WO2017141398A1 - 情報処理装置、情報処理方法およびコンピュータプログラム - Google Patents

情報処理装置、情報処理方法およびコンピュータプログラム Download PDFInfo

- Publication number

- WO2017141398A1 WO2017141398A1 PCT/JP2016/054702 JP2016054702W WO2017141398A1 WO 2017141398 A1 WO2017141398 A1 WO 2017141398A1 JP 2016054702 W JP2016054702 W JP 2016054702W WO 2017141398 A1 WO2017141398 A1 WO 2017141398A1

- Authority

- WO

- WIPO (PCT)

- Prior art keywords

- information

- financial institution

- score

- subject

- analysis

- Prior art date

Links

Images

Classifications

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q40/00—Finance; Insurance; Tax strategies; Processing of corporate or income taxes

- G06Q40/03—Credit; Loans; Processing thereof

-

- H—ELECTRICITY

- H04—ELECTRIC COMMUNICATION TECHNIQUE

- H04L—TRANSMISSION OF DIGITAL INFORMATION, e.g. TELEGRAPHIC COMMUNICATION

- H04L63/00—Network architectures or network communication protocols for network security

- H04L63/04—Network architectures or network communication protocols for network security for providing a confidential data exchange among entities communicating through data packet networks

- H04L63/0407—Network architectures or network communication protocols for network security for providing a confidential data exchange among entities communicating through data packet networks wherein the identity of one or more communicating identities is hidden

- H04L63/0414—Network architectures or network communication protocols for network security for providing a confidential data exchange among entities communicating through data packet networks wherein the identity of one or more communicating identities is hidden during transmission, i.e. party's identity is protected against eavesdropping, e.g. by using temporary identifiers, but is known to the other party or parties involved in the communication

-

- H—ELECTRICITY

- H04—ELECTRIC COMMUNICATION TECHNIQUE

- H04L—TRANSMISSION OF DIGITAL INFORMATION, e.g. TELEGRAPHIC COMMUNICATION

- H04L63/00—Network architectures or network communication protocols for network security

- H04L63/08—Network architectures or network communication protocols for network security for authentication of entities

- H04L63/0815—Network architectures or network communication protocols for network security for authentication of entities providing single-sign-on or federations

Definitions

- This invention relates to data processing technology, and more particularly to information processing technology that supports the operations of financial institutions.

- a technology for efficiently realizing asset liability management (Asset Liability Management (ALM)) for the purpose of normal bank management has been proposed (for example, see Patent Document 1). Further, a technique for improving the accuracy of debtor asset assessment and reducing credit risk of financial institutions has been proposed (see, for example, Patent Document 2).

- the present invention has been made in view of the above problems, and a main purpose thereof is to provide a technology that supports financial institutions so as to be able to provide a business more suited to the state of each customer.

- an information processing apparatus is an apparatus that supports a business of a financial institution, and acquires asset information indicating an asset held by an analysis subject outside the financial institution.

- the score determination unit for determining the score of the analysis subject for determining the business content of the financial institution with respect to the analysis subject based on the asset information acquired by the acquisition unit, and the score determination unit

- a support information generation unit that generates information for supporting the business of the financial institution for the analysis subject based on the score of the analysis subject.

- This device is a device that supports the operations of a plurality of financial institutions, and obtains asset information indicating assets held by the first entity, which is an analysis subject in the first financial institution, outside the first financial institution.

- a first financial institution for determining the business contents of the first financial institution for the first main body based on the asset information of the first main body acquired by the department, the asset information of the first main body acquired by the acquisition unit, and the parameters predetermined by the first financial institution.

- a score determination unit that determines the score of the main body, and a support information generation unit that generates information for supporting the business of the first financial institution for the first main body based on the score of the first main body determined by the score determination unit And comprising.

- the acquisition unit further acquires asset information indicating an asset held by the second entity, which is an analysis subject in the second financial institution, outside the second financial institution, and the score determination unit receives the second information acquired by the acquisition unit.

- the score of the second entity for determining the business content of the second financial institution for the second entity is further determined, and support information is generated

- the unit further generates information for supporting the business of the second financial institution for the second entity based on the score of the second entity determined by the score determination unit.

- Still another aspect of the present invention is an information processing method.

- a device that supports the business of a financial institution acquires asset information indicating assets held by the analysis target entity outside the financial institution, and the analysis target entity based on the acquired asset information.

- the step of determining the score of the analysis subject for determining the business content of the financial institution, and information for supporting the business of the financial institution for the analysis subject based on the determined score of the analysis subject And generating.

- FIG. 1 It is a figure which shows the structure of the information system of embodiment. It is a block diagram which shows the function structure of the work assistance apparatus of FIG. It is a figure which shows the example of the loan with respect to a certain individual. It is a figure which shows the example of the loan with respect to a certain individual. It is a figure which shows the structure of the information system of a 4th modification.

- a business support device (a business support device 14 to be described later) that supports a loan business for individuals (for example, a housing loan) in a financial institution is proposed.

- This business support device dynamically calculates both credit amount and lending interest rate for each customer according to various attribute information of individual customers (including individuals who are potential customers and individuals who are sales targets) To do.

- the credit amount can be said to be a loanable amount, and it can also be said to be the maximum loan amount.

- a personal number (My Number (registered trademark)) is assigned to each citizen from a public institution (government, etc.).

- the personal number is an ID unique to the individual that is not changed throughout the lifetime. From 2016, personal numbers will be required for administrative procedures such as social security, taxes and disaster countermeasures.

- the business support apparatus uses this personal number to collect various attribute information of an individual who receives a loan from an external apparatus.

- FIG. 1 shows a configuration of an information system 10 according to the embodiment.

- the information system 10 includes a PC 12 a and a PC 12 b collectively referred to as a PC 12, a business support device 14, and a personal attribute information source 16. 1 are connected via a communication network 18 including a LAN, a WAN, the Internet, and a dedicated line.

- a communication network 18 including a LAN, a WAN, the Internet, and a dedicated line.

- encryption and authentication processing for maintaining security may be performed as appropriate during communication.

- PC 12a is a PC installed in bank A and operated by a bank A loan officer.

- the PC 12b is a PC installed in the bank B and operated by a bank B loan officer.

- the PC 12 may be another type of information terminal such as a tablet terminal or a smartphone.

- the personal attribute information source 16 is a general term for a plurality of database devices (hereinafter referred to as “DB”) that store various attribute information related to individuals who are debtors.

- the personal attribute information source 16 includes a collateral information DB 20, a route price information DB 22, a property information DB 24, an annuity information DB 26, a possessed securities information DB 28, an insurance information DB 30, a debt information DB 32, an income information DB 34, a work information DB 36, and a company information DB 38. .

- each DB included in the personal attribute information source 16 is installed.

- each DB is installed outside the bank A and in a company or institution outside the bank B, but as a modification, it is installed in at least one of the bank A and the bank B. Good.

- One DB may be distributed and installed in a plurality of companies and institutions.

- the retained securities information DB 28 may be realized by a plurality of securities company DBs

- the liability information DB may be realized by a plurality of banks or credit card company DBs.

- the personal attribute information held in the personal attribute information source 16 includes information indicating personal assets, liabilities, and income.

- An asset in the embodiment means an economic value that is attributed to an individual and expected to generate profit for the individual, and can be said to be a property.

- a liability means a payment obligation attributed to an individual and owed to an external third party, and includes, for example, a borrowing.

- the collateral information DB 20 the route price information DB 22, the property information DB 24, the pension information DB 26, the securities information DB 28, and the insurance information DB 30 hold information related to personal assets.

- the liability information DB 32 holds information related to individual debt

- the income information DB 34 and the work information DB 36 hold information related to personal income. Specific examples are shown below.

- the collateral information DB 20 holds the appraisal value of land and buildings that are collateral (for example, assets subject to mortgage setting) in financing.

- the collateral information DB 20 may be installed in, for example, a research company or a real estate company.

- the route price information DB 22 holds information on route prices throughout Japan.

- the route price information DB 22 may be installed in, for example, a public organization (such as a tax organization).

- the property information DB 24 holds information such as price information and sales time of properties (land, buildings, etc.) that an individual intends to purchase.

- the property information DB 24 may be installed in a real estate company or a home sales company.

- the pension information DB 26 holds personal pension information.

- the pension information includes the annual amount that the individual will receive in the future, for example, the defined contribution pension amount.

- the pension information DB 26 may be installed in a private or public pension mechanism or pension information service company.

- the held securities information DB 28 holds information such as stocks and bonds held by individuals.

- the owned securities information DB 28 may be installed in a plurality of securities companies.

- the insurance information DB 30 holds information on life insurance that an individual joins, for example, saving life insurance.

- Insurance information DB30 may be installed in a plurality of insurance companies.

- the liability information DB 32 holds information on liabilities (for example, car loans) for which individuals are obligated to pay.

- the debt information DB 32 may be installed in a bank other than the banks A and B, a credit card company, or a credit information agency.

- the income information DB 34 holds information (annual income amount, income amount, etc.) indicating individual income.

- the income information DB 34 may be installed in a public organization such as a tax organization.

- the work information DB 36 holds information such as the name of the company where the individual works, the treatment at the place of work (position, etc.), and the length of service.

- the work information DB 36 may be installed in a company where a person works or a credit information agency.

- the company information DB 38 holds information indicating the management status and financial status of various companies.

- the company information DB 38 may be installed in a credit information agency, an ICT service company, or the like.

- Each DB included in the personal attribute information source 16 stores attribute information related to each individual in association with a personal number assigned to each individual.

- each DB receives an acquisition request for personal attribute information from a predetermined external device via the communication network 18, each DB provides attribute information associated with the personal number designated as a key in the request to the request source device.

- the business support device 14 is an information processing device such as a server managed by an ICT service company.

- the ICT service company is, for example, a system integrator or an ASP (Application Service Provider) provider.

- the business support device 14 provides the PC 12a and the PC 12b with web pages including information (hereinafter also referred to as “business support information”) that supports the business of a plurality of financial institutions (in the embodiment, the bank A and the bank B). Since the function of the web server is publicly known, description thereof is omitted.

- the business support apparatus 14 uses the personal number of the individual to be analyzed (hereinafter also referred to as “analysis target individual”) as the loan destination candidate of the A bank or the B bank, and uses the personal number of the analysis target individual. Collect multiple types of attribute information related to debt, income, etc. from the personal attribute information source 16. Then, based on the collected plural types of attribute information, business support information for supporting the execution of the loan business in accordance with the state of each individual to be analyzed is provided to the PC 12 of the A bank or the B bank. Further, the business support apparatus 14 provides such business support information providing service as an ASP type service to a plurality of financial institutions (in the embodiment, bank A and bank B).

- FIG. 2 is a block diagram showing a functional configuration of the business support apparatus 14 of FIG.

- the business support apparatus 14 includes a control unit 40, a storage unit 42, and a communication unit 44.

- the control unit 40 executes various types of data processing such as collection processing of attribute information related to the individual to be analyzed and generation processing of business support information for the banks A and B.

- the storage unit 42 is a storage area that stores data that is referred to or updated by the control unit 40.

- the communication unit 44 communicates with an external device according to a known communication protocol.

- the control unit 40 transmits / receives data to / from each DB included in the PC 12a, PC 12b, and personal attribute information source 16 via the communication unit 44.

- Each block shown in the block diagram of the present specification can be realized in terms of hardware by an element such as a CPU and a memory of a computer or a mechanical device, and in terms of software, it can be realized by a computer program or the like. , Depicts functional blocks realized by their cooperation. Therefore, those skilled in the art will understand that these functional blocks can be realized in various forms by a combination of hardware and software.

- a business support application including a module corresponding to each block of the control unit 40 may be installed in the storage of the business support device 14.

- the CPU of the business support apparatus 14 may exhibit the functions of these blocks by reading out the modules corresponding to the respective blocks of the control unit 40 to the main memory and executing them.

- Each functional block of the storage unit 42 may be realized by storing data in a storage device such as a storage or a memory of the business support device 14.

- the storage unit 42 includes a bank A parameter holding unit 46 and a bank B parameter holding unit 48.

- the bank A parameter holding unit 46 stores parameters predetermined by the bank A.

- the bank B parameter holding unit 48 is a parameter determined independently of the parameters stored in the bank A parameter holding unit 46, and stores a parameter predetermined by the bank B.

- the parameters stored in the bank A parameter holding unit 46 and the bank B parameter holding unit 48 are data for deriving the score of the individual to be analyzed according to the contents of the asset information, debt information, and income information of the individual to be analyzed. is there.

- This parameter is information indicating the degree to which each of the plurality of attribute information of the individual to be analyzed affects the work support information (in the embodiment, the credit amount and the lending interest rate), and can be said to be data for weighting.

- This parameter is not limited to a numerical value, and may be a program indicating an algorithm for realizing the degree of influence or weighting according to the attribute value.

- a parameter for reflecting the content indicated by the attribute information in the credit amount is referred to as a credit amount parameter

- a parameter for reflecting the content indicated by the attribute information in the interest rate is referred to as an interest rate parameter.

- the credit of each attribute information classified as asset information so that the amount of assets indicated by the asset information (for example, the market capitalization of the stock held) is positively correlated with the credit amount, while being inversely correlated with the interest rate.

- An amount parameter and an interest rate parameter may be defined.

- the credit amount parameter and interest rate parameter of each attribute information classified as liability information so that the amount of debt indicated by the liability information (for example, the existing loan balance) is inversely correlated with the credit amount while being directly correlated with the interest rate.

- the credit amount parameter and interest rate of each attribute information classified as income information so that the amount of income indicated by the income information (including the height of the position) is positively correlated with the credit amount and inversely correlated with the interest rate.

- a parameter may be defined.

- Each bank may set the parameters of each information item so that the correlation coefficient of the information item to be emphasized with respect to the interest rate or the like is larger than the correlation coefficient of other information items.

- different weights may be set for each type according to the judgment of each bank. The same applies to debt information and income information. This example will be described below.

- bank A places more importance on the market capitalization of stocks than the defined contribution pension amount.

- Bank A uses the credit parameter for the defined contribution pension amount and the amount of the defined contribution pension amount to be more positively correlated with the credit amount than the degree to which the defined contribution pension amount is directly correlated with the credit amount.

- a credit amount parameter for the market capitalization of stocks may be set.

- bank A has an interest rate parameter for the defined contribution pension amount, so that the degree of the inverse correlation to the interest rate of the market capitalization of the stock is stronger than the degree of the inverse correlation to the interest rate of the defined contribution pension amount, You may set the interest rate parameter for the market capitalization of stocks.

- Bank B places more importance on the defined contribution pension amount than the market capitalization of shares.

- Bank B has a credit parameter for the defined contribution pension amount and the amount of the defined contribution pension amount that is more positively correlated with the credit amount than the degree that the market capitalization of the shares held is positively correlated with the credit amount.

- a credit amount parameter for the market capitalization of stocks may be set.

- Bank B has an interest rate parameter for the defined contribution pension amount, so that the degree of the inverse correlation with respect to the interest rate of the defined contribution pension amount is stronger than the degree of inverse correlation with respect to the interest rate of the market capitalization of shares. You may set the interest rate parameter for the market capitalization of stocks.

- each of the plurality of financial institutions that use the business support apparatus 14 sets arbitrary values as the credit amount parameter and the interest rate parameter.

- the control unit 40 includes a personal attribute acquisition unit 50, a personal score determination unit 52, a support information generation unit 54, a support information provision unit 60, and a parameter setting unit 62.

- the personal attribute acquisition unit 50 transmits an attribute acquisition request designating the personal number of the individual to be analyzed as a search key to a plurality of DBs included in the personal attribute information source 16.

- the personal attribute acquisition unit 50 is attribute information associated with the personal number of the search key from each DB included in the personal attribute information source 16, for example, at least one of asset information, liability information, and income information related to the individual to be analyzed. Get one.

- the personal attribute acquisition unit 50 acquires the defined contribution pension amount of the individual to be analyzed from the pension information DB 26 installed in the public institution.

- the personal attribute acquisition unit 50 acquires stock brands and quantities held by the individual to be analyzed from the securities information DB 28 installed in the securities company.

- the personal attribute acquisition unit 50 acquires the liabilities (for example, the balance of the car loan, the repayment status, etc.) held by the individual to be analyzed from the debt information DB 32 installed in a bank other than Bank A and Bank B or a credit information agency.

- the personal score determination unit 52 is a plurality of attribute information regarding the individual to be analyzed acquired by the personal attribute acquisition unit 50. Specifically, the personal score determination unit 52 includes a plurality of attribute information classified as asset information, liability information, or income information. First, the score of the individual to be analyzed for determining the business contents of the financial institution for the individual to be analyzed is determined. Specifically, the personal score determination unit 52 determines a score according to a plurality of attribute information related to the individual to be analyzed and parameters predetermined by the bank A or the bank B for each attribute information.

- the score of the individual to be analyzed is data for adjusting the value of the reference credit amount and the value of the reference interest rate specified by the bank A or bank B as the analysis request source.

- a score for adjusting the reference credit amount is called a credit amount adjustment score

- a score for adjusting the reference interest rate is called an interest rate adjustment score.

- the credit amount adjustment score can be said to be adjustment data that reflects the actual attribute information of the individual to be analyzed on the credit amount by the weighting indicated by the credit amount parameter.

- the interest rate adjustment score can be said to be adjustment data that reflects the actual attribute information of the individual to be analyzed to the interest rate by the weighting indicated by the interest rate parameter.

- the standard credit amount and the standard interest rate are standard credit amount and interest rate determined in advance in each of the bank A and the bank B.

- the reference interest rate may be a conventional loan interest rate (a floating interest rate, a 10-year fixed interest rate, etc.) determined based on a short-term prime rate.

- a reference credit amount and a reference interest rate are designated by a person in charge at each bank when an analysis request is made to the business support apparatus 14.

- the business support apparatus 14 may acquire the reference credit amount and the reference interest rate from each bank apparatus in advance and store them in the storage unit 42 in advance.

- the personal score determination unit 52 of the embodiment includes a collateral information rate, a pension rate, a holding stock rate, a participation insurance rate, a service company rank rate, a service years rate, a job title rate, a debt rate, and an income rate as credit adjustment scores. decide.

- the personal score determination unit 52 determines a collateral information rate, an annuity rate, a holding stock rate, an enrollment insurance rate, a working company rank rate, a service years rate, a job title rate, a debt rate, and an income rate as interest rate adjustment scores.

- the personal score determination unit 52 stores the collateral information (land and building), building age, road price, property information acquired from the personal attribute information source 16, the bank A parameter holding unit 46 or the bank B parameter holding unit 48.

- the collateral information rate as the credit amount adjustment score is calculated according to the credit amount parameter associated with each attribute information.

- the personal score determination unit 52 uses the collateral information (land and building), age, road price, property information acquired from the personal attribute information source 16 and the bank A parameter holding unit 46 or the bank B parameter holding unit 48.

- a collateral information rate as an interest rate adjustment score is calculated according to the interest rate parameter associated with each attribute information.

- the credit amount parameter stored in the bank A parameter holding unit 46 and the bank B parameter holding unit 48 of the embodiment increases the credit amount as the asset amount of the individual to be analyzed (for example, the market price or valuation amount of the stock held) increases.

- the value is determined as follows. Increasing the credit amount can be said to increase the increment from a predetermined standard reference credit amount.

- the value of the interest rate parameter is determined such that the interest rate decreases as the asset amount of the individual to be analyzed increases. Reducing the interest rate can be said to increase the discount from a predetermined standard reference interest rate.

- the individual score determination unit 52 determines the collateral information rate, the pension rate, the stock holding rate, and the enrollment insurance rate as the credit amount adjustment score so that the credit amount increases as the asset amount of the individual to be analyzed increases.

- the personal score determination unit 52 determines a collateral information rate, an annuity rate, a stock holding rate, and an enrollment insurance rate as an interest rate adjustment score so that the interest rate decreases as the asset amount of the individual to be analyzed increases.

- the relationship between the amount of income and the income rate is the same. As described above, when the credit risk (in other words, credit loss risk) of a specific individual to be analyzed is relatively low, the credit amount to the individual is relatively increased and the interest rate is relatively decreased. To adjust.

- the credit amount parameter stored in the bank A parameter holding unit 46 and the bank B parameter holding unit 48 of the embodiment is such that the credit amount decreases as the debt amount (for example, borrowing balance) of the individual to be analyzed increases. Is determined.

- the value of the interest rate parameter is determined such that the interest rate increases as the amount of debt of the individual to be analyzed increases.

- the individual score determination unit 52 determines the collateral information rate, the pension rate, the stock holding rate, and the enrollment insurance rate as the credit amount adjustment score so that the credit amount decreases as the amount of debt held by the individual to be analyzed increases.

- the personal score determination unit 52 determines the collateral information rate, pension rate, stock holding rate, and insurance coverage rate as the interest rate adjustment score so that the interest rate increases as the debt amount of the individual to be analyzed increases.

- the support information generation unit 54 generates information for supporting the business of the financial institution for the analysis target individual based on the score of the analysis target individual determined by the personal score determination unit 52. Specifically, the support information generation unit 54 determines a value obtained by adjusting the reference credit amount based on the credit amount adjustment score of the analysis target individual as the credit amount for the analysis target individual. Further, the support information generation unit 54 determines a value obtained by adjusting the reference interest rate based on the interest rate adjustment score of the analysis target individual as the interest rate for the analysis target individual. Then, the support information generation unit 54 generates business support information indicating the credit amount and interest rate for the individual to be analyzed.

- the support information generation unit 54 includes a credit amount determination unit 56 and an interest rate determination unit 58.

- the credit amount determination unit 56 determines the credit amount for the individual to be analyzed by adjusting the reference credit amount based on the credit amount adjustment score of the individual to be analyzed.

- the credit amount determination unit 56 adds a reference credit amount, a collateral information rate as a credit amount adjustment score, a pension rate, a stock holding rate, a working company rank rate, and a service years rate to a predetermined credit amount calculation formula (function).

- the position rate, debt rate, and income rate may be input, and the credit amount for the individual to be analyzed may be acquired as the calculation result.

- Credit amount for individuals to be analyzed standard credit amount x collateral information rate x pension rate x holding stock rate x working company rank rate x years of service rate x position rate x liability rate x income rate

- the individual score determination unit 52 is “0 ⁇ rate ⁇ 1” when the credit amount for the individual to be analyzed is smaller than the reference credit amount, and “1 ⁇ rate” when the credit amount for the individual to be analyzed is equal to or greater than the reference credit amount.

- the score of each attribute information is determined so that it becomes. In addition, you may determine so that the multiplication result of multiple types of credit amount adjustment scores may be in the said range.

- the interest rate determination unit 58 determines the lending interest rate for the individual to be analyzed by adjusting the reference interest rate based on the interest rate adjustment score of the individual to be analyzed.

- the interest rate determination unit 58 calculates the reference interest rate, the collateral information rate as the interest rate adjustment score, the pension rate, the stock holding rate, the working company rank rate, the years of service rate, the job rate,

- the debt rate and the income rate may be input, and the interest rate for the individual to be analyzed may be acquired as the calculation result.

- Interest rate for individuals to be analyzed standard credit amount x collateral information rate x pension rate x holding stock rate x working company rank rate x years of service rate x position rate x debt rate x income rate

- the personal score determination unit 52 Each attribute is set so that “0 ⁇ rate ⁇ 1” when the interest rate for the individual subject to analysis is discounted from the base rate, and “1 ⁇ rate” when the interest rate for the individual subject to analysis is greater than or equal to the base rate. Determine the information score. In addition, you may determine so that the multiplication result of several types of interest rate adjustment scores may become the said range.

- the support information providing unit 60 transmits the business support information including the credit amount and interest rate for the individual to be analyzed generated by the support information generating unit 54 to the analysis request source PC 12a or PC 12b. Specifically, the web page data indicating the business support information is transmitted to the PC 12a or PC 12b.

- the parameter setting unit 62 transmits and displays a web page for changing at least one of the credit amount parameter and the interest rate parameter to the PC 12a and the PC 12b.

- the parameter setting unit 62 receives the initial value and the updated value of the credit amount parameter and the interest rate parameter input to the web page from the PC 12a and the PC 12b.

- the parameter setting unit 62 reflects the received parameter value in the score determination processing of the individual to be analyzed by the personal score determination unit 52.

- the parameter setting unit 62 stores the credit amount parameter and the interest rate parameter value received from the PC 12 a in the bank A parameter holding unit 46. In other words, the previous parameter value stored in the bank A parameter holding unit 46 is updated to the latest value received from the PC 12a.

- the parameter setting unit 62 stores the value of the credit amount parameter and the interest rate parameter received from the PC 12 b in the bank B parameter holding unit 48. In other words, the previous parameter value stored in the bank B parameter holding unit 48 is updated to the latest value received from the PC 12b.

- the updated values of the credit amount parameter and the interest rate parameter are reflected in the score of the individual to be analyzed, and are reflected in the credit amount and the interest rate for the individual to be analyzed.

- the loan officer of bank A activates the web browser of the PC 12a, logs in to the business support site provided by the business support device 14, and selects the loan business support menu.

- the business support device 14 transmits a web page (referred to as “analysis target designation page”) for inputting information related to the individual to be analyzed to the PC 12a for display.

- the loan officer of Bank A sets the individual credit number and interest rate on the analysis target designation page in addition to the individual number of the individual to be analyzed as the individual to be analyzed as the individual who is the mortgage loan candidate. Enter the operation.

- the web browser of the PC 12a transmits an analysis request, which is an HTTP request including the individual number of the individual to be analyzed, the reference credit amount, and the reference interest rate, to the business support apparatus 14.

- the personal attribute acquisition unit 50 of the business support device 14 uses the personal number specified in the request as a key to analyze from a plurality of DBs included in the personal attribute information source 16 Get multiple types of attribute information about an individual.

- the personal score determination unit 52 of the business support device 14 is a parameter stored in the bank A parameter holding unit 46, and responds to a plurality of types of attribute information according to a credit amount parameter predetermined by the analysis request source A bank.

- the credit amount adjustment score (shareholding rate, debt rate, etc.) is determined.

- the personal score determination unit 52 determines an interest rate adjustment score according to a plurality of types of attribute information according to interest rate parameters predetermined by the bank A as the analysis request source.

- the support information generation unit 54 of the business support device 14 determines the credit amount for the individual to be analyzed based on the reference credit amount specified in the analysis request and the credit amount adjustment score determined by the personal score determination unit 52. Further, the support information generation unit 54 determines the interest rate of the loan for the individual to be analyzed based on the reference interest rate specified in the analysis request and the interest rate adjustment score determined by the personal score determination unit 52. Then, the support information generation unit 54 generates web page data of business support information indicating the credit amount and interest rate of the loan to the individual to be analyzed, and the support information providing unit 60 transmits the web page data to the PC 12a for display. .

- the person in charge of bank A formulates a loan plan according to the credit amount and interest provided from the business support apparatus 14 and presents it to the individual to be analyzed.

- the credit amount and interest rate appropriate for each individual according to the asset holding status, debt holding status, and income status of each individual as a debtor are presented to the financial institution, Can support risk management and risk control of financial institutions.

- the stock is treated as a collateral element of debt and reflected in the credit amount and interest rate.

- the actual performance for example, company rank, length of service, title, treatment, etc.

- the collateral market value can be calculated by calculating the collateral value linked with the property price information.

- the business support device 14 performs the same process according to the analysis request transmitted from the PC 12b. Execute. However, when the individual score determination unit 52 determines the score of the individual to be analyzed, the parameters are stored in the bank B parameter holding unit 48, and the credit amount parameter and the interest rate parameter predetermined by the analysis request source B bank It differs in that it refers to.

- the loan officer of bank A determines the updated values of the credit amount parameter and the interest rate parameter.

- the loan officer of bank A activates the web browser of the PC 12a, logs in to the loan business support site provided by the business support device 14, and selects the parameter setting menu.

- the business support apparatus 14 transmits a web page (referred to as a “parameter setting page”) for inputting the credit amount parameter and the updated value of the interest rate parameter to the PC 12a for display.

- the loan officer inputs the updated value of the credit amount parameter and the interest rate parameter to the parameter setting page, and inputs an operation for reflecting the setting value.

- the web browser of the PC 12a transmits a parameter setting request, which is an HTTP request including the updated value of the credit amount parameter and the interest rate parameter, to the business support apparatus 14.

- a parameter setting request which is an HTTP request including the updated value of the credit amount parameter and the interest rate parameter

- the parameter setting unit 62 of the business support apparatus 14 stores the credit amount parameter and the updated value of the interest rate parameter included in the request in the bank A parameter holding unit 46.

- the setting operation of the credit amount parameter and the interest rate parameter of the bank B is the same, but the storage destination of the parameter value is the bank B parameter holding unit 48.

- the business support apparatus 14 collectively provides business support services for a plurality of financial institutions as an ASP service.

- each financial institution can enjoy the business support service at a lower cost than the construction of the business support device 14 on its own.

- the credit amount parameter and the interest rate parameter for determining the score of the individual to be analyzed can be set to values uniquely determined by each financial institution and can be changed as needed.

- each financial institution can cause the business support device 14 to determine the risk management policy and the credit amount and interest rate in accordance with the business strategy.

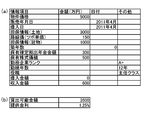

- FIG. 3 shows an example of financing for a certain individual.

- FIG. 3A shows individual attribute information at the time of the initial loan.

- FIG. 3B shows the credit amount (upper stage) and the interest rate (lower stage) determined by the business support apparatus 14 based on the attribute information shown in FIG.

- FIG. 4 shows an example of financing for the same individual as FIG.

- FIG. 4A shows individual attribute information five years after FIG. 3A.

- FIG. 4B shows the credit amount (upper stage) and the interest rate (lower stage) determined by the business support apparatus 14 based on the attribute information shown in FIG.

- FIG. 3 (a) Comparing the attribute information in FIG. 3 (a) with the attribute information in FIG. 4 (a), FIG. 3 (a) has a smaller liability amount, so FIG. 3 (a) has a lower credit risk based on the liability. It can be said. However, Figure 4 (a) has larger assets (collateral, share price, defined contribution pension amount, etc.) and income (working company rank, years of service, title, income amount). It can be said that the credit risk based on assets and income is smaller.

- the credit amount and interest rate calculated by the business support apparatus 14 comprehensively reflect the assets held, liabilities held, and income of the individual to be analyzed. In this example, the credit amount larger than FIG. 3B is calculated in FIG. 4B, and the interest rate smaller than FIG. 3B is calculated in FIG. 4B.

- a person in charge of a financial institution can propose an additional loan to a low interest rate to a customer by looking at the result of FIG.

- a credit amount smaller than that in FIG. 3B is calculated in FIG. In b), it is possible to calculate a higher interest rate than in FIG.

- each DB in the personal attribute information source 16 electronically stores attribute information related to the individual to be analyzed, and the business support apparatus 14 acquires the attribute information of the individual to be analyzed from each DB. did.

- at least a part of attribute information related to the individual to be analyzed may be reported verbally or on paper from the individual to be analyzed to bank A or bank B, and the attribute information thus reported is sent from the PC 12 to the business support apparatus 14. It may be entered.

- attribute information for example, in addition to the individual number, standard credit amount, and standard interest rate of the individual subject to analysis, one or more attribute information (stock stocks and quantity held, title and years of service at the workplace, etc.) declared by the individual subject to analysis

- the analysis request may be input from the PC 12 to the business support apparatus 14. It is suitable for acquiring attribute information for which electronic acquisition from an external DB is prohibited or restricted by law or attribute information that requires high confidentiality.

- the business support apparatus 14 of the above embodiment derives the credit amount adjustment score and the interest rate adjustment score of the analysis target individual according to the plurality of types of attribute information of the analysis target individual. Based on those scores, information (information indicating the credit amount and interest rate for the individual to be analyzed) that supports the financing operation from the financial institution to the individual to be analyzed was generated and provided to the PC 12.

- the business support device 14 is a score for determining the business content of the financial institution for the individual to be analyzed, and may determine a score other than the credit amount adjustment score and the interest rate adjustment score.

- a score indicating the importance of the individual to be analyzed for the financial institution may be determined, or a score indicating the accuracy of loan establishment, purchase of securities, contract of insurance, etc. may be determined.

- the support information generation unit 54 of the business support device 14 generates business support information indicating the score of the individual to be analyzed determined by the personal score determination unit 52, and the support information provision unit 60 displays the business support information. You may provide to PC12.

- the business support device 14 collects attribute information related to a plurality of individuals specified by the PC 12a or the PC 12b and stores business support information for supporting the business of the financial institution for the plurality of individuals.

- the generation may be executed collectively. In other words, the generation of business support information regarding a plurality of individuals may be executed as a batch process.

- the business support device 14 selects a score (for example, a score indicating the number of shares held) from a plurality of individuals. May extract individuals who satisfy the extraction conditions predetermined by the financial institution. Then, business support information including the extracted personal score and various attribute information may be generated and provided to the financial institution.

- the business support apparatus 14 collects attribute information about an analysis target person from a plurality of DBs included in the personal attribute information source 16 using a personal number assigned to the analysis target person from a public institution. .

- the first temporary number for identifying the analysis target person in the financial institution, and the analysis target individual in an entity different from the financial institution A second temporary number for identification may be determined in advance, and the first temporary number and the second temporary number may be associated with each other by a predetermined device.

- FIG. 5 shows the configuration of the information system of the fourth modified example.

- the information system 10 of the fourth modification includes a personal number management device 70 in addition to the configuration of FIG.

- the business support apparatus 14 accesses the personal number management apparatus 70 via the communication network 18.

- the personal number management apparatus 70 corresponds to the personal number management apparatus proposed by the present applicant in “Japanese Patent Application No. 2013-216936 (Japanese Patent Laid-Open No. 2015-79406)”.

- the personal number management device 70 receives a personal number report from an individual (not shown) (that is, an individual who can be analyzed), and based on the personal number, a financial institution (here, bank A). A first temporary number for identifying the individual is determined in step (b). The personal number management device 70 may directly transmit the determined first temporary number together with personal identification information (name, address, etc.) to the device of the bank A designated by the individual as the destination of the first temporary number. . Alternatively, the personal number management device 70 may provide the determined first temporary number to the personal device, and the individual may declare the first temporary number to the bank A.

- the personal number management device 70 receives a personal number declaration from the same individual, and determines a second temporary number for identifying the individual at each company or organization of the personal attribute information source 16 based on the personal number. To do.

- the second temporary number may be transmitted to the personal attribute information source 16 in the same manner as the first temporary number.

- the second temporary number is determined to be different for each company / institution managing the DB of the personal attribute information source 16, but here, as a second temporary number, for simplicity of explanation, explain.

- Each DB of the personal attribute information source 16 stores attribute information related to the individual to be analyzed in association with the second temporary number of the individual. Actually, DBs of companies and institutions different from each other may store attribute information related to the analysis target person in association with different second temporary numbers.

- an individual's personal number, first temporary number, and second temporary number are IDs having different systems, lengths, contents, and the like. Moreover, it is desirable that both the first temporary number and the second temporary number are determined to be IDs that are difficult to guess the original personal number.

- the first temporary number of the individual to be analyzed may be handled in the same manner as the personal number of the individual to be analyzed in the bank A, and the second temporary number of the individual to be analyzed is stored in the company or institution of the personal attribute information source 16 It may be handled in the same way as a personal number. However, since the first temporary number is different from the personal number, the number management cost in the bank A can be reduced, and the influence when the first temporary number is leaked is limited. The same can be said for the second temporary number.

- the personal number management device 70 stores the personal personal number, the first temporary number, and the second temporary number in association with each other (see, for example, FIG. 3 of JP-A-2015-79406).

- the personal number management device 70 receives a search request designating the first temporary number, the personal number management device 70 transmits information indicating the second temporary number associated with the first temporary number to the requesting device.

- the PC 12a of the fourth modified example transmits an analysis request including the first temporary number, the reference credit amount, and the reference interest rate of the individual to be analyzed to the business support apparatus 14.

- the personal attribute acquisition unit 50 of the business support apparatus 14 transmits a search request specifying the first temporary number specified in the analysis request to the personal number management apparatus 70, and the first temporary number The second temporary number managed in association with is acquired from the personal number management device 70.

- the personal attribute acquisition unit 50 transmits an attribute acquisition request designating the second temporary number as a key to a plurality of DBs included in the personal attribute information source 16, and manages the attribute information associated with the second temporary number. Is acquired from each DB.

- the personal attribute acquisition unit 50 may acquire a plurality of types of second temporary numbers from the personal number management device 70 together with information of the DB provided with each second temporary number. And you may transmit the search request which designated the different 2nd temporary number with respect to different DB.

- the personal number management device 70 centrally manages personal numbers that require high security and confidentiality. Since the financial institution and the personal attribute information source 16 perform information management using the first temporary number or the second temporary number different from the personal number as a key, the risk of leakage of the personal number can be reduced. In addition, the burden of personal number management at each company or institution can be reduced.

- the business support apparatus 14 collectively provides business support services for a plurality of financial institutions as an ASP service.

- the business support device 14 may be constructed as a device that generates business support information for one financial institution or a small number of financial institutions in the same company group.

- the business support apparatus 14 that includes the bank A parameter holding unit 46 but does not include the bank B parameter holding unit 48 may be built in the bank A.

- the business support apparatus 14 that includes the bank B parameter holding unit 48 but does not include the bank A parameter holding unit 46 may be built in the bank B.

- the analysis target by the business support apparatus 14 is an individual, but the subject to be analyzed is not limited to an individual.

- the subject to be analyzed by the business support apparatus 14 may be a corporation (company, organization, etc.).

- the loan destination of the financial institution supported by the business support device 14 is not limited to an individual, and may be a corporation.

- each DB of the personal attribute information source 16 may store the attribute information of the analysis target corporation in association with the corporation number that is a unique number of the corporation assigned to the corporation by a public institution.

- the PC 12 may transmit an analysis request specifying the corporate number of the analysis target corporation to the business support apparatus 14.

- the business support apparatus 14 may collect attribute information of the analysis target corporation from each DB of the personal attribute information source 16 using the corporation number as a key. Then, information that supports the business of the financial institution with respect to the corporation (for example, information on the credit amount or interest rate of the loan to the corporation) may be generated and provided to the PC 12.

- This invention can be applied to a device that supports the business of a financial institution.

Abstract

金融機関の業務を支援する業務支援装置14は、当該金融機関の外部に分析対象主体が保有する資産を示す資産情報を個人属性情報ソース16から取得する。業務支援装置14は、個人属性情報ソース16から取得した資産情報にもとづいて、分析対象主体に対する当該金融機関の業務内容を決定するための分析対象主体のスコアを決定する。業務支援装置14は、決定したスコアにもとづいて、分析対象主体に対する当該金融機関の業務を支援するための情報を生成する。

Description

この発明はデータ処理技術に関し、特に金融機関の業務を支援する情報処理技術に関する。

正常な銀行経営を目的とした資産負債管理(Asset Liability Management(ALM))を効率的に実現するための技術が提案されている(例えば特許文献1参照)。また、債務者の資産査定の精度を向上し、金融機関の信用リスクを低減するための技術が提案されている(例えば特許文献2参照)。

これまで、金融機関から顧客(個人および法人を含む)に対して実施される融資の金利は金融機関側の要因(短期プライムレート等)で決定されてきた。本発明者は、ローンの多様化や、証券資産の拡大等が見込まれる今後、顧客各々が保有する資産の状態に応じて柔軟に金利を調整することが金融機関にとって重要になると考えた。

本発明は上記課題を鑑みてなされたものであり、主たる目的は、個々の顧客の状態に一層即した業務を提供できるよう金融機関を支援する技術を提供することである。

上記課題を解決するために、本発明のある態様の情報処理装置は、金融機関の業務を支援する装置であって、当該金融機関の外部に分析対象主体が保有する資産を示す資産情報を取得する取得部と、取得部により取得された資産情報にもとづいて、分析対象主体に対する当該金融機関の業務内容を決定するための分析対象主体のスコアを決定するスコア決定部と、スコア決定部により決定された分析対象主体のスコアにもとづいて、分析対象主体に対する当該金融機関の業務を支援するための情報を生成する支援情報生成部と、を備える。

本発明の別の態様もまた、情報処理装置である。この装置は、複数の金融機関の業務を支援する装置であって、第1金融機関における分析対象主体である第1主体が第1金融機関の外部に保有する資産を示す資産情報を取得する取得部と、取得部により取得された第1主体の資産情報と、第1金融機関により予め定められたパラメータとにもとづいて、第1主体に対する第1金融機関の業務内容を決定するための第1主体のスコアを決定するスコア決定部と、スコア決定部により決定された第1主体のスコアにもとづいて、第1主体に対する第1金融機関の業務を支援するための情報を生成する支援情報生成部と、を備える。取得部は、第2金融機関における分析対象主体である第2主体が第2金融機関の外部に保有する資産を示す資産情報をさらに取得し、スコア決定部は、取得部により取得された第2主体の資産情報と、第2金融機関により予め定められたパラメータとにもとづいて、第2主体に対する第2金融機関の業務内容を決定するための第2主体のスコアをさらに決定し、支援情報生成部は、スコア決定部により決定された第2主体のスコアにもとづいて、第2主体に対する第2金融機関の業務を支援するための情報をさらに生成する。

本発明のさらに別の態様は、情報処理方法である。この方法は、金融機関の業務を支援する装置が、当該金融機関の外部に分析対象主体が保有する資産を示す資産情報を取得するステップと、取得された資産情報にもとづいて、分析対象主体に対する当該金融機関の業務内容を決定するための分析対象主体のスコアを決定するステップと、決定された分析対象主体のスコアにもとづいて、分析対象主体に対する当該金融機関の業務を支援するための情報を生成するステップと、を実行する。

なお、以上の構成要素の任意の組合せ、本発明の表現を、システム、コンピュータプログラム、コンピュータプログラムを格納した記録媒体などの間で変換したものもまた、本発明の態様として有効である。

本発明によれば、個々の顧客の状態に一層即した業務を提供できるよう金融機関を支援することができる。

実施の形態では、金融機関における個人向けの融資業務(例えば住宅ローン等)を支援する業務支援装置(後述の業務支援装置14)を提案する。この業務支援装置は、個々の顧客(潜在的な顧客である個人、営業ターゲットとなる個人を含む)の種々の属性情報に応じて、顧客毎の与信額と貸出金利の両方を動的に算出する。与信額は、貸出可能金額と言え、融資上限額とも言える。

また現在日本では、公的機関(政府等)から国民1人1人へ個人番号(マイナンバー(登録商標))が付与されている。個人番号は、原則として、一生変更されない個人固有のIDとなる。2016年からは、社会保障、税、災害対策等の行政手続において個人番号が必要となる予定である。実施の形態の業務支援装置は、この個人番号を利用して、融資を受ける対象となる個人の種々の属性情報を外部装置から収集する。

図1は、実施の形態の情報システム10の構成を示す。情報システム10は、PC12で総称されるPC12aおよびPC12b、業務支援装置14、個人属性情報ソース16を備える。図1の各装置は、LAN・WAN・インターネット・専用線を含む通信網18を介して接続される。以下説明しないが、通信に際して、セキュリティを維持するための暗号化や認証処理が適宜実行されてもよい。

PC12aは銀行Aに設置され、銀行Aの融資担当者により操作されるPCである。PC12bは銀行Bに設置され、銀行Bの融資担当者により操作されるPCである。PC12は、タブレット端末またはスマートフォン等、他の種類の情報端末であってもよい。

個人属性情報ソース16は、債務者となる個人に関する様々な属性情報を記憶する複数のデータベースの装置(以下「DB」と呼ぶ。)の総称である。個人属性情報ソース16は、担保情報DB20、路線価情報DB22、物件情報DB24、年金情報DB26、保有証券情報DB28、保険情報DB30、負債情報DB32、収入情報DB34、勤務情報DB36、企業情報DB38を含む。

個人属性情報ソース16に含まれる各DBが設置される場所に制限はない。実施の形態では、いずれのDBも銀行Aの外部で、かつ銀行Bの外部の企業や機関に設置されることとするが、変形例として、銀行Aと銀行Bの少なくとも一方にも設置されてよい。また、1つのDBは、複数の企業や機関に分散して設置されてもよい。例えば、保有証券情報DB28は複数の証券会社のDBにより実現されてもよく、負債情報DBは複数の銀行やクレジットカード会社のDBにより実現されてもよい。

個人属性情報ソース16に保持される個人の属性情報は、個人の資産、負債、収入を示す情報を含む。実施の形態の資産は、個人に帰属し、個人に収益をもたらすことが期待される経済的価値を意味し、財産とも言える。一方、負債は、個人に帰属し、個人が外部の第三者に対して負う支払い義務を意味し、例えば借入金を含む。個人属性情報ソース16に含まれるDBのうち、担保情報DB20、路線価情報DB22、物件情報DB24、年金情報DB26、保有証券情報DB28、保険情報DB30は、個人の資産に関する情報を保持する。また、負債情報DB32は個人の負債に関する情報を保持し、収入情報DB34、勤務情報DB36は個人の収入に関する情報を保持する。以下、具体例を示す。

担保情報DB20は、融資における担保(例えば抵当権設定の対象資産)となる土地や建物の査定額を保持する。担保情報DB20は、例えば調査会社や不動産会社に設置されてもよい。路線価情報DB22は、日本全国の路線価の情報を保持する。路線価情報DB22は、例えば公的機関(税務機関等)に設置されてもよい。物件情報DB24は、個人が購入しようとする物件(土地や建物等)の価格情報や販売時期等の情報を保持する。物件情報DB24は、不動産会社や住宅販売会社に設置されてもよい。

年金情報DB26は個人の年金情報を保持する。年金情報は、個人が将来受取予定の年金額を含み、例えば確定拠出年金金額を含む。年金情報DB26は、民間または公共の年金機構や年金情報サービス会社に設置されてもよい。保有証券情報DB28は、個人が保有する株式・債権等の情報を保持する。保有証券情報DB28は、複数の証券会社に設置されてもよい。保険情報DB30は、個人が加入する生命保険、例えば貯蓄型の生命保険の情報を保持する。保険情報DB30は、複数の保険会社に設置されてもよい。負債情報DB32は、個人が支払義務を負う負債(例えば自動車ローン等)の情報を保持する。負債情報DB32は、銀行Aと銀行B以外の銀行や、クレジットカード会社、信用情報機関に設置されてもよい。

収入情報DB34は、個人の収入を示す情報(年間収入額や所得額等)を保持する。収入情報DB34は、税務機関等の公的機関に設置されてもよい。勤務情報DB36は、個人が勤務する会社名、勤務先での処遇(役職等)、勤続年数等の情報を保持する。勤務情報DB36は、個人が勤務する会社や信用情報機関等に設置されてもよい。企業情報DB38は、様々な会社の経営状況や財務状況を示す情報を保持する。企業情報DB38は、信用情報機関やICTサービス企業等に設置されてもよい。

個人属性情報ソース16に含まれる各DBは、各個人に関する属性情報を各個人に付与された個人番号と対応づけて記憶する。各DBは、通信網18を介して所定の外部装置から個人属性情報の取得要求を受け付けると、その要求でキーとして指定された個人番号に対応づけられた属性情報を要求元装置へ提供する。

業務支援装置14は、ICTサービス企業が管理するサーバ等の情報処理装置である。ICTサービス企業は、例えばシステムインテグレータやASP(Application Service Provider)事業者である。業務支援装置14は、複数の金融機関(実施の形態では銀行Aおよび銀行B)の業務を支援する情報(以下「業務支援情報」とも呼ぶ。)を含むウェブページをPC12aおよびPC12bへ提供する。ウェブサーバの機能は公知のため説明を省略する。

具体的には、業務支援装置14は、A銀行またはB銀行の融資先候補として分析対象となる個人(以下「分析対象個人」とも呼ぶ。)の個人番号を使用して、分析対象個人の資産・負債・収入等に関する複数種類の属性情報を個人属性情報ソース16から収集する。そして、収集した複数種類の属性情報にもとづいて、分析対象個人それぞれの状態に即した融資業務の遂行を支援する業務支援情報をA銀行またはB銀行のPC12へ提供する。また業務支援装置14は、このような業務支援情報の提供サービスをASP型のサービスとして複数の金融機関(実施の形態では銀行Aおよび銀行B)へ提供する。

図2は、図1の業務支援装置14の機能構成を示すブロック図である。業務支援装置14は、制御部40、記憶部42、通信部44を備える。制御部40は、分析対象個人に関する属性情報の収集処理と、銀行Aおよび銀行Bに対する業務支援情報の生成処理等、各種のデータ処理を実行する。記憶部42は、制御部40により参照または更新されるデータを記憶する記憶領域である。通信部44は、公知の通信プロトコルにしたがって外部装置と通信する。制御部40は、通信部44を介して、PC12a、PC12b、個人属性情報ソース16に含まれる各DBとデータを送受する。

本明細書のブロック図で示す各ブロックは、ハードウェア的には、コンピュータのCPUやメモリをはじめとする素子や機械装置で実現でき、ソフトウェア的にはコンピュータプログラム等によって実現されるが、ここでは、それらの連携によって実現される機能ブロックを描いている。したがって、これらの機能ブロックはハードウェア、ソフトウェアの組合せによっていろいろなかたちで実現できることは、当業者には理解されるところである。

例えば、制御部40の各ブロックに対応するモジュールを備える業務支援アプリケーションが業務支援装置14のストレージへインストールされてもよい。業務支援装置14のCPUは、制御部40の各ブロックに対応するモジュールをメインメモリに読み出して実行することにより、それらのブロックの機能を発揮してもよい。また、記憶部42の各機能ブロックは、業務支援装置14のストレージやメモリ等の記憶装置がデータを記憶することにより実現されてもよい。

記憶部42は、銀行Aパラメータ保持部46と銀行Bパラメータ保持部48を含む。銀行Aパラメータ保持部46には、銀行Aにより予め定められたパラメータが格納される。銀行Bパラメータ保持部48には、銀行Aパラメータ保持部46に格納されるパラメータとは独立して定められたパラメータであり、銀行Bにより予め定められたパラメータが格納される。銀行Aパラメータ保持部46と銀行Bパラメータ保持部48に格納されるパラメータは、分析対象個人の資産情報、負債情報、収入情報それぞれの内容に応じた分析対象個人のスコアを導出するためのデータである。

このパラメータは、分析対象個人の複数の属性情報のそれぞれが業務支援情報(実施の形態では与信額と貸出金利)に影響する度合を示す情報であり、重み付けのためのデータとも言える。このパラメータは、数値に限らず、属性値に応じた影響度合または重み付けを実現するためのアルゴリズムを示すプログラム等であってもよい。以下、属性情報が示す内容を与信額に反映させるためのパラメータを与信額パラメータと呼び、属性情報が示す内容を金利に反映させるためのパラメータを金利パラメータと呼ぶ。

パラメータの設定例として、資産情報が示す資産の量(例えば保有株式の時価総額)が与信金額に正相関し、一方で金利に逆相関するように、資産情報に分類される各属性情報の与信額パラメータと金利パラメータが定められてよい。また、負債情報が示す負債の量(例えば既存のローン残高)が与信金額に逆相関し、一方で金利に正相関するように、負債情報に分類される各属性情報の与信額パラメータと金利パラメータが定められてよい。また、収入情報が示す収入の量(役職の高さを含む)が与信金額に正相関し、一方で金利に逆相関するように、収入情報に分類される各属性情報の与信額パラメータと金利パラメータが定められてよい。

資産情報、負債情報、収入情報のうち、どの情報項目を重視するかは銀行Aと銀行Bのそれぞれの判断で決定される。各銀行は、重視する情報項目の金利等に対する相関係数が他の情報項目の相関係数よりも大きくなるように、各情報項目のパラメータを設定してもよい。また、同じ資産情報に分類される複数種類の属性情報について、各銀行の判断にて種類毎に異なる重み付けが設定されてもよい。負債情報と収入情報についても同様である。以下この例を説明する。

例えば、銀行Aが、確定拠出年金金額よりも保有株式時価総額を重視するケースを想定する。このケースでは、銀行Aは、確定拠出年金金額が与信額に正相関する度合よりも、保有株式時価総額が与信額に正相関する度合が強くなるように、確定拠出年金金額に対する与信額パラメータと、保有株式時価総額に対する与信額パラメータを設定してもよい。また、このケースでは、銀行Aは、確定拠出年金金額の金利に対する逆相関の度合よりも、保有株式時価総額の金利に対する逆相関の度合が強くなるように、確定拠出年金金額に対する金利パラメータと、保有株式時価総額に対する金利パラメータを設定してもよい。

別の例として、銀行Bが、保有株式時価総額よりも確定拠出年金金額を重視するケースを想定する。このケースでは、銀行Bは、保有株式時価総額が与信額に正相関する度合よりも、確定拠出年金金額が与信額に正相関する度合が強くなるように、確定拠出年金金額に対する与信額パラメータと、保有株式時価総額に対する与信額パラメータを設定してもよい。また、このケースでは、銀行Bは、保有株式時価総額の金利に対する逆相関の度合よりも、確定拠出年金金額の金利に対する逆相関の度合が強くなるように、確定拠出年金金額に対する金利パラメータと、保有株式時価総額に対する金利パラメータを設定してもよい。このように、業務支援装置14を利用する複数の金融機関のそれぞれは、与信額パラメータおよび金利パラメータとして任意の値を設定する。

制御部40は、個人属性取得部50、個人スコア決定部52、支援情報生成部54、支援情報提供部60、パラメータ設定部62を含む。個人属性取得部50は、分析対象個人の個人番号を検索キーとして指定した属性取得要求を、個人属性情報ソース16に含まれる複数のDBへ送信する。個人属性取得部50は、個人属性情報ソース16に含まれる各DBから、検索キーの個人番号に対応づけられた属性情報であり、例えば分析対象個人に関する資産情報、負債情報、収入情報の少なくとも1つを取得する。

例えば、個人属性取得部50は、公的機関に設置された年金情報DB26から分析対象個人の確定拠出年金金額を取得する。また個人属性取得部50は、証券会社に設置された保有証券情報DB28から、分析対象個人が保有する株式の銘柄と数量を取得する。また個人属性取得部50は、銀行Aと銀行B以外の銀行や信用情報機関に設置された負債情報DB32から、分析対象個人が抱える負債(例えば自動車ローンの残額や返済状況等)を取得する。

個人スコア決定部52は、個人属性取得部50により取得された分析対象個人に関する複数の属性情報であり、具体的には、資産情報、負債情報、または収入情報に分類される複数の属性情報にもとづいて、分析対象個人に対する金融機関の業務内容を決定するための、分析対象個人のスコアを決定する。具体的には、個人スコア決定部52は、分析対象個人に関する複数の属性情報と、各属性情報に対して予め銀行Aまたは銀行Bが定めたパラメータにしたがってスコアを決定する。

実施の形態における分析対象個人のスコアは、分析要求元の銀行Aまたは銀行Bにより指定された基準与信額の値と基準金利の値を調整するデータである。基準与信額を調整するスコアを与信額調整スコアと呼び、基準金利を調整するスコアを金利調整スコアと呼ぶ。与信額調整スコアは、分析対象個人の実際の属性情報を与信額パラメータが示す重み付けの分、与信額へ反映させる調整データと言える。同様に、金利調整スコアは、分析対象個人の実際の属性情報を金利パラメータが示す重み付けの分、金利へ反映させる調整データと言える。

ここで基準与信額と基準金利は、銀行Aと銀行Bそれぞれの内部で予め定められた標準的な与信額と金利である。例えば基準金利は、短期プライムレートにもとづいて決定された従来のローン金利(変動金利や10年固定金利等)でもよい。実施の形態では、業務支援装置14に対する分析要求時に各銀行の担当者により基準与信額と基準金利が指定されることとする。変形例として、業務支援装置14は、各銀行の装置から基準与信額と基準金利を予め取得し、予め記憶部42に記憶してもよい。

実施の形態の個人スコア決定部52は、与信額調整スコアとしての担保情報レート、年金レート、保有株式レート、加入保険レート、勤務企業ランクレート、勤続年数レート、役職レート、負債レート、収入レートを決定する。また個人スコア決定部52は、金利調整スコアとしての担保情報レート、年金レート、保有株式レート、加入保険レート、勤務企業ランクレート、勤続年数レート、役職レート、負債レート、収入レートを決定する。

例えば、個人スコア決定部52は、個人属性情報ソース16から取得された担保情報(土地および建物)、築年数、路線価、物件情報と、銀行Aパラメータ保持部46または銀行Bパラメータ保持部48にて各属性情報と対応づけられた与信額パラメータにしたがって、与信額調整スコアとしての担保情報レートを算出する。また個人スコア決定部52は、個人属性情報ソース16から取得された担保情報(土地および建物)、築年数、路線価、物件情報と、銀行Aパラメータ保持部46または銀行Bパラメータ保持部48にて各属性情報と対応づけられた金利パラメータにしたがって、金利調整スコアとしての担保情報レートを算出する。

実施の形態の銀行Aパラメータ保持部46と銀行Bパラメータ保持部48に記憶される与信額パラメータは、分析対象個人の資産額(例えば保有株式の時価や評価額等)が大きいほど与信額を大きくするように値が定められる。与信額を大きくするとは、予め定められた標準的な基準与信額からの増分を大きくするともいえる。その一方、金利パラメータは、分析対象個人の資産額が大きいほど金利を小さくするように値が定められる。金利を小さくするとは、予め定められた標準的な基準金利からの割引を大きくするとも言える。

したがって個人スコア決定部52は、分析対象個人の資産額が大きいほど与信額が大きくなるように与信額調整スコアとしての担保情報レート、年金レート、保有株式レート、加入保険レートを決定する。また個人スコア決定部52は、分析対象個人の資産額が大きいほど金利が小さくなるように金利調整スコアとしての担保情報レート、年金レート、保有株式レート、加入保険レートを決定する。収入額と収入レートの関係も同様である。このように、特定の分析対象個人の信用リスク(言い換えれば貸倒リスク)が相対的に低い場合は、その個人への与信額を相対的に大きくし、金利を相対的に小さくするように動的に調整する。

また実施の形態の銀行Aパラメータ保持部46と銀行Bパラメータ保持部48に記憶される与信額パラメータは、分析対象個人の負債額(例えば借入金残高等)が大きいほど与信額を小さくするように値が定められる。その一方、金利パラメータは、分析対象個人の負債額が大きいほど金利を大きくするように値が定められる。

したがって個人スコア決定部52は、分析対象個人が抱える負債額が大きいほど与信額が小さくなるように与信額調整スコアとしての担保情報レート、年金レート、保有株式レート、加入保険レートを決定する。また個人スコア決定部52は、分析対象個人の負債額が大きいほど金利が大きくなるように金利調整スコアとしての担保情報レート、年金レート、保有株式レート、加入保険レートを決定する。このように、特定の分析対象個人の信用リスクが相対的に高い場合は、その個人への与信額を相対的に小さくし、金利を相対的に大きくするように動的に調整する。

支援情報生成部54は、個人スコア決定部52により決定された分析対象個人のスコアにもとづいて、分析対象個人に対する金融機関の業務を支援するための情報を生成する。具体的には、支援情報生成部54は、分析対象個人の与信額調整スコアにもとづいて基準与信額を調整した値を、分析対象個人向けの与信額として決定する。また支援情報生成部54は、分析対象個人の金利調整スコアにもとづいて基準金利を調整した値を、分析対象個人向けの金利として決定する。そして支援情報生成部54は、分析対象個人向けの与信額と金利を示す業務支援情報を生成する。

支援情報生成部54は、与信額決定部56と金利決定部58を含む。与信額決定部56は、分析対象個人の与信額調整スコアにもとづいて基準与信額を調整することにより、分析対象個人向けの与信額を決定する。与信額決定部56は、予め定められた与信額計算式(関数)に、基準与信額と、与信額調整スコアとしての担保情報レート、年金レート、保有株式レート、勤務企業ランクレート、勤続年数レート、役職レート、負債レート、収入レートを入力し、その計算結果として分析対象個人向けの与信額を取得してもよい。

例えば、以下のような計算式でもよい。

分析対象個人向けの与信額 = 基準与信額×担保情報レート×年金レート×保有株式レート×勤務企業ランクレート×勤続年数レート×役職レート×負債レート×収入レート

この計算式の場合、個人スコア決定部52は、分析対象個人向けの与信額を基準与信額より小さくする場合に「0<レート<1」とし、分析対象個人向けの与信額を基準与信額以上とする場合に「1≦レート」となるように各属性情報のスコアを決定する。なお、複数種類の与信額調整スコアの乗算結果が上記範囲になるよう決定してもよい。

分析対象個人向けの与信額 = 基準与信額×担保情報レート×年金レート×保有株式レート×勤務企業ランクレート×勤続年数レート×役職レート×負債レート×収入レート

この計算式の場合、個人スコア決定部52は、分析対象個人向けの与信額を基準与信額より小さくする場合に「0<レート<1」とし、分析対象個人向けの与信額を基準与信額以上とする場合に「1≦レート」となるように各属性情報のスコアを決定する。なお、複数種類の与信額調整スコアの乗算結果が上記範囲になるよう決定してもよい。

金利決定部58は、分析対象個人の金利調整スコアにもとづいて基準金利を調整することにより、分析対象個人向けの貸出金利を決定する。金利決定部58は、予め定められた金利計算式(関数)に、基準金利と、金利調整スコアとしての担保情報レート、年金レート、保有株式レート、勤務企業ランクレート、勤続年数レート、役職レート、負債レート、収入レートを入力し、その計算結果として分析対象個人向けの金利を取得してもよい。

例えば、以下のような計算式でもよい。

分析対象個人向けの金利 = 基準与信額×担保情報レート×年金レート×保有株式レート×勤務企業ランクレート×勤続年数レート×役職レート×負債レート×収入レート

この計算式の場合、個人スコア決定部52は、分析対象個人向けの金利を基準金利より割引く場合に「0<レート<1」とし、分析対象個人向けの金利を基準金利以上とする場合に「1≦レート」となるように各属性情報のスコアを決定する。なお、複数種類の金利調整スコアの乗算結果が上記範囲になるよう決定してもよい。

分析対象個人向けの金利 = 基準与信額×担保情報レート×年金レート×保有株式レート×勤務企業ランクレート×勤続年数レート×役職レート×負債レート×収入レート

この計算式の場合、個人スコア決定部52は、分析対象個人向けの金利を基準金利より割引く場合に「0<レート<1」とし、分析対象個人向けの金利を基準金利以上とする場合に「1≦レート」となるように各属性情報のスコアを決定する。なお、複数種類の金利調整スコアの乗算結果が上記範囲になるよう決定してもよい。

支援情報提供部60は、支援情報生成部54により生成された分析対象個人向けの与信額および金利を含む業務支援情報を、分析要求元のPC12aまたはPC12bへ送信する。具体的には、業務支援情報を示すウェブページのデータをPC12aまたはPC12bへ送信する。

パラメータ設定部62は、与信額パラメータと金利パラメータの少なくとも一方を変更するためのウェブページをPC12aおよびPC12bへ送信して表示させる。パラメータ設定部62は、そのウェブページに入力された与信額パラメータと金利パラメータの初期値や更新値をPC12aおよびPC12bから受け付ける。パラメータ設定部62は、受け付けたパラメータの値を個人スコア決定部52による分析対象個人のスコア決定処理に反映させる。

具体的には、パラメータ設定部62は、PC12aから受け付けた与信額パラメータと金利パラメータの値を銀行Aパラメータ保持部46へ格納する。言い換えれば、銀行Aパラメータ保持部46に格納済のそれまでのパラメータ値を、PC12aから受け付けた最新の値へ更新する。同様にパラメータ設定部62は、PC12bから受け付けた与信額パラメータと金利パラメータの値を銀行Bパラメータ保持部48へ格納する。言い換えれば、銀行Bパラメータ保持部48に格納済のそれまでのパラメータ値を、PC12bから受け付けた最新の値へ更新する。与信額パラメータおよび金利パラメータの更新値は、分析対象個人のスコアへ反映され、分析対象個人向けの与信額および金利へ反映される。

以上の構成による動作を説明する。銀行Aの融資担当者は、PC12aのウェブブラウザを起動して、業務支援装置14が提供する業務支援サイトへログインし、融資業務支援メニューを選択する。融資業務支援メニューが選択されると、業務支援装置14は、分析対象個人に関する情報を入力させるためのウェブページ(「分析対象指定ページ」と呼ぶ。)をPC12aへ送信して表示させる。銀行Aの融資担当者は、住宅ローンの融資先候補である個人を分析対象個人として、分析対象個人の個人番号に加えて、基準与信額と基準金利を分析対象指定ページへ入力し、分析開始の操作を入力する。PC12aのウェブブラウザは、分析対象個人の個人番号、基準与信額、基準金利を含むHTTP要求である分析要求を業務支援装置14へ送信する。

PC12aから送信された分析要求を受信すると、業務支援装置14の個人属性取得部50は、当該要求で指定された個人番号をキーとして、個人属性情報ソース16に含まれる複数のDBから、分析対象個人に関する複数種類の属性情報を取得する。業務支援装置14の個人スコア決定部52は、銀行Aパラメータ保持部46に格納されたパラメータであり、分析要求元のA銀行により予め定められた与信額パラメータにしたがって、複数種類の属性情報に応じた与信額調整スコア(保有株式レート、負債レート等)を決定する。同様に個人スコア決定部52は、分析要求元のA銀行により予め定められた金利パラメータにしたがって、複数種類の属性情報に応じた金利調整スコアを決定する。

業務支援装置14の支援情報生成部54は、分析要求で指定された基準与信額と、個人スコア決定部52により決定された与信額調整スコアにもとづいて、分析対象個人に対する与信額を決定する。また支援情報生成部54は、分析要求で指定された基準金利と、個人スコア決定部52により決定された金利調整スコアにもとづいて、分析対象個人に対する融資の金利を決定する。そして支援情報生成部54は、分析対象個人に対する融資の与信額と金利を示す業務支援情報のウェブページデータを生成し、支援情報提供部60は、当該ウェブページデータをPC12aへ送信して表示させる。銀行Aの担当者は、業務支援装置14から提供された与信額および金利にしたがって融資計画を策定し、分析対象個人へ提示する。

このように、業務支援装置14によると、債務者としての個人毎の資産保有状態、負債保有状態、収入状況に応じた、個人毎の適切な与信額および金利を金融機関へ提示し、債権者としての金融機関のリスクマネジメントやリスクコントロールを支援できる。例えば、個人が保有する株式を解約させることなく、その株式を債務の担保的な要素として取り扱い、与信額や金利に反映させる。また、ローン契約する個人の社会人としての実績(例えば会社のランクや勤続年数、役職、処遇等)を与信額や金利に反映させる。さらにまた、不動産の路線価情報と連動した担保価値計算によって担保の時価計算を実現できる。

債務者としての個人は、多くの株式を保有する場合や、貯蓄型保険の貯蓄額が大きい場合、確定拠出年金金額が大きい場合等、基準与信額より大きい借り入れが可能になり、また基準金利より低金利で融資を受けやすくなるというメリットを享受できる。また債権者としての金融機関は、個々の顧客の状態に一層即した融資計画を策定しやすくなり、リスクをコントロールしつつ競争力を高めることができるというメリットを享受できる。

銀行Bの融資担当者が、PC12bのウェブブラウザを起動して、業務支援装置14の融資業務支援サイトへアクセスする場合も、業務支援装置14は、PC12bから送信された分析要求にしたがって同様の処理を実行する。ただし、個人スコア決定部52が分析対象個人のスコアを決定する際に、銀行Bパラメータ保持部48に格納されたパラメータであり、分析要求元のB銀行により予め定められた与信額パラメータと金利パラメータを参照する点で異なる。

銀行Aの融資担当者(パラメータの決定権限を持つ管理者等)は、与信額パラメータおよび金利パラメータの更新値を決定する。銀行Aの融資担当者は、PC12aのウェブブラウザを起動して、業務支援装置14が提供する融資業務支援サイトへログインし、パラメータ設定メニューを選択する。パラメータ設定メニューが選択されると、業務支援装置14は、与信額パラメータおよび金利パラメータの更新値を入力させるためのウェブページ(「パラメータ設定ページ」と呼ぶ。)をPC12aへ送信して表示させる。融資担当者は、与信額パラメータおよび金利パラメータの更新値をパラメータ設定ページへ入力し、設定値反映の操作を入力する。

PC12aのウェブブラウザは、与信額パラメータおよび金利パラメータの更新値を含むHTTP要求であるパラメータ設定要求を業務支援装置14へ送信する。PC12aから送信されたパラメータ設定要求を受信すると、業務支援装置14のパラメータ設定部62は、その要求が含む与信額パラメータおよび金利パラメータの更新値を銀行Aパラメータ保持部46へ格納する。銀行Bの与信額パラメータおよび金利パラメータの設定動作も同様になるが、パラメータ値の格納先は銀行Bパラメータ保持部48になる。

このように、実施の形態の業務支援装置14は、ASPサービスとして、複数の金融機関に対する業務支援サービスを一括して提供する。これにより、各金融機関は、自前で業務支援装置14を構築するよりも安価に業務支援サービスを享受できる。また、分析対象個人のスコアを決定するための与信額パラメータおよび金利パラメータには、各金融機関が独自に決定した値を設定でき、また随時変更することができる。これにより、各金融機関は、自機関におけるリスクマネジメントのポリシーや、ビジネス戦略に即した与信額および金利を業務支援装置14にて決定させることができる。

図3は、或る個人に対する融資の例を示す。図3(a)は、初期融資時の個人の属性情報を示している。図3(b)は、図3(a)に示す属性情報にもとづいて業務支援装置14が決定した与信額(上段)と金利(下段)を示している。図4は、図3と同一の個人に対する融資の例を示す。図4(a)は、図3(a)から5年後の個人の属性情報を示している。図4(b)は、図4(a)に示す属性情報にもとづいて業務支援装置14が決定した与信額(上段)と金利(下段)を示している。

図3(a)の属性情報と図4(a)の属性情報を比較すると、図3(a)の方が負債金額が小さいため、図3(a)の方が負債に基づく信用リスクが小さいと言える。しかし、図4(a)の方が、保有資産(担保や保有株式価額、確定拠出年金金額等)および収入(勤務企業ランク、勤続年数、役職、収入金額)が大きく、図4(a)の方が資産・収入に基づく信用リスクが小さいと言える。業務支援装置14により算出される与信額と金利には、分析対象個人の保有資産、保有負債、収入が総合的に反映される。この例では、図4(b)では図3(b)より大きい与信額を算出し、図4(b)では図3(b)より小さい金利を算出している。

例えば、金融機関の担当者は、図4(b)の結果を見て、低金利への追加融資を顧客へ提案することができる。また、変動金利での融資を行っている場合に、顧客の現在の状態に即して、図3(b)に示す金利から図4(b)に示す金利へ見直すことを顧客へ提案することができる。なお、業務支援装置14を利用する金融機関が、負債金額の少なさを重視してパラメータを設定する場合、図4(b)では図3(b)より小さい与信額を算出し、図4(b)では図3(b)より高い金利を算出することもあり得る。

以上、本発明を実施の形態をもとに説明した。実施の形態は例示であり、各構成要素や各処理プロセスの組合せにいろいろな変形例が可能なこと、またそうした変形例も本発明の範囲にあることは当業者に理解されるところである。以下変形例を示す。

第1変形例を説明する。上記実施の形態では、個人属性情報ソース16内の各DBは、分析対象個人に関する属性情報を電子的に記憶し、業務支援装置14は、各DBから分析対象個人の属性情報を取得することとした。変形例として、分析対象個人に関する少なくとも一部の属性情報が、分析対象個人から銀行Aまたは銀行Bへ口頭や紙にて申告されてもよく、申告された属性情報がPC12から業務支援装置14へ入力されてもよい。例えば、分析対象個人の個人番号、基準与信額、基準金利に加えて、分析対象個人から申告された1つ以上の属性情報(保有株式銘柄や数量、勤務先での役職や勤続年数等)を含む分析要求が、PC12から業務支援装置14へ入力されてもよい。外部DBからの電子的な取得が法律で禁止または制限されている属性情報や、高い秘匿性が求められる属性情報の取得に好適である。

第2変形例を説明する。上記実施の形態の業務支援装置14は、分析対象個人の複数種類の属性情報にしたがって、分析対象個人の与信額調整スコアと金利調整スコアを導出した。そして、それらのスコアにもとづいて、金融機関から分析対象個人への融資業務を支援する情報(分析対象個人向けの与信額と金利を示す情報)を生成し、PC12へ提供した。変形例として、業務支援装置14は、分析対象個人に対する金融機関の業務内容を決定するためのスコアであり、与信額調整スコアと金利調整スコア以外のスコアを決定してもよい。例えば、金融機関にとって分析対象個人の重要度を示すスコアを決定してもよく、融資の成立や、証券の購入、保険の成約等の確度を示すスコアを決定してもよい。また、業務支援装置14の支援情報生成部54は、個人スコア決定部52により決定された分析対象個人のスコアそのものを示す業務支援情報を生成し、支援情報提供部60は、その業務支援情報をPC12へ提供してもよい。

第3変形例を説明する。上記実施の形態では言及していないが、業務支援装置14は、PC12aまたはPC12bにより指定された複数の個人に関する属性情報の収集と、それら複数の個人に対する金融機関の業務を支援する業務支援情報の生成を一括して実行してもよい。言い換えれば、複数の個人に関する業務支援情報の生成をバッチ処理として実行してもよい。また、第2変形例で説明したように個人のスコアそのものを示す業務支援情報を生成する場合、業務支援装置14は、複数の個人の中から、スコア(例えば保有株式数の多寡を示すスコア)が金融機関により予め定められた抽出条件を充足する個人を抽出してもよい。そして、抽出した個人に関するスコアや各種属性情報を含む業務支援情報を生成し、金融機関へ提供してもよい。

第4変形例を説明する。上記実施の形態の業務支援装置14は、公的機関から分析対象個人へ付与された個人番号を使用して、個人属性情報ソース16に含まれる複数のDBから分析対象個人に関する属性情報を収集した。変形例として、公的機関から分析対象個人へ付与された個人番号にもとづいて、金融機関において分析対象個人を識別するための第1仮番号と、当該金融機関とは異なる主体において分析対象個人を識別するための第2仮番号が予め決定され、第1仮番号と第2仮番号は所定の装置で対応づけられてもよい。

図5は、第4変形例の情報システムの構成を示す。第4変形例の情報システム10は、図1の構成に加えて個人番号管理装置70を備える。業務支援装置14は、通信網18を介して個人番号管理装置70へアクセスする。個人番号管理装置70は、本出願人が「特願2013-216936(特開2015-79406号公報)」で提案した個人番号管理装置に対応する。

具体的には、個人番号管理装置70は、不図示の個人(すなわち分析対象個人となりうる個人)から個人番号の申告を受け付け、その個人番号にもとづいて、金融機関(ここでは銀行Aとする)において当該個人を識別するための第1仮番号を決定する。個人番号管理装置70は、決定した第1仮番号を個人の識別情報(氏名や住所等)とともに、第1仮番号の提供先として個人により指定された銀行Aの装置へ直接送信してもよい。または、個人番号管理装置70は、決定した第1仮番号を個人の装置へ提供し、個人が第1仮番号を銀行Aへ申告してもよい。

また個人番号管理装置70は、同じ個人から個人番号の申告を受け付け、その個人番号にもとづいて、個人属性情報ソース16の各企業や各機関において当該個人を識別するための第2仮番号を決定する。第1仮番号と同様の方法にて、第2仮番号は個人属性情報ソース16へ伝達されてよい。なお実際には、第2仮番号は、個人属性情報ソース16のDBを管理する企業毎・機関毎に異なる番号が決定されるが、ここでは説明の簡明化のため1つの第2仮番号として説明する。個人属性情報ソース16の各DBは、分析対象個人に関する属性情報を、当該個人の第2仮番号に対応づけて記憶する。実際には、互いに異なる企業や機関のDBは、分析対象個人に関する属性情報を、互いに異なる第2仮番号に対応づけて記憶してもよい。

ここで、ある個人の個人番号、第1仮番号、第2仮番号は、体系・長さ・内容等が互いに異なるIDである。また、第1仮番号と第2仮番号はいずれも、オリジナルの個人番号を推測困難なIDが決定されることが望ましい。分析対象個人の第1仮番号は、銀行Aにおいて分析対象個人の個人番号と同等に取り扱われてよく、分析対象個人の第2仮番号は個人属性情報ソース16の企業や機関において分析対象個人の個人番号と同等に取り扱われてよい。ただし、第1仮番号は個人番号とは異なるため、銀行Aにおける番号管理コストを低減でき、第1仮番号が万が一漏洩した場合の影響も限定的になる。第2仮番号も同じことが言える。

個人番号管理装置70は、個人の個人番号、第1仮番号、第2仮番号を対応づけて記憶する(例えば特開2015-79406号公報の図3等を参照)。個人番号管理装置70は、第1仮番号を指定した検索要求を受け付けると、その第1仮番号に対応づけられた第2仮番号を示す情報を要求元の装置へ送信する。

第4変形例のPC12aは、分析対象個人の第1仮番号、基準与信額、基準金利を含む分析要求を業務支援装置14へ送信する。業務支援装置14の個人属性取得部50は、この分析要求を受け付けると、この分析要求で指定された第1仮番号を指定した検索要求を個人番号管理装置70へ送信し、その第1仮番号に対応づけて管理された第2仮番号を個人番号管理装置70から取得する。個人属性取得部50は、第2仮番号をキーとして指定した属性取得要求を、個人属性情報ソース16に含まれる複数のDBへ送信し、その第2仮番号に対応づけて管理された属性情報を各DBから取得する。実際には、個人属性取得部50は、個人番号管理装置70から、複数種類の第2仮番号を、各第2仮番号が提供されたDBの情報とともに取得してもよい。そして、異なるDBに対して異なる第2仮番号を指定した検索要求を送信してもよい。

第4変形例の態様によると、高度なセキュリティと秘匿性が求められる個人番号を個人番号管理装置70が集中的に一括管理する。金融機関や個人属性情報ソース16では、個人番号とは異なる第1仮番号または第2仮番号をキーとして情報管理を行うため、個人番号の漏洩リスクを低減できる。また、各企業や機関における個人番号管理の負担を低減できる。

第5変形例を説明する。上記実施の形態では、業務支援装置14は、複数の金融機関に対する業務支援サービスをASPサービスとして一括して提供した。変形例として、業務支援装置14は、1つの金融機関、または同一企業グループ内の少数の金融機関向けの業務支援情報を生成する装置として構築されてもよい。例えば、銀行Aパラメータ保持部46を備える一方、銀行Bパラメータ保持部48を備えない業務支援装置14が銀行Aに構築されてよい。またそれとは別個に、銀行Bパラメータ保持部48を備える一方、銀行Aパラメータ保持部46を備えない業務支援装置14が銀行Bに構築されてもよい。

第6変形例を説明する。上記実施の形態では、業務支援装置14による分析対象を個人としたが、分析対象となる主体は個人に限られない。例えば、業務支援装置14による分析対象主体は法人(企業や団体等)であってもよい。言い換えれば、業務支援装置14により支援される金融機関の融資先は個人に限られず、法人であってもよい。この場合、個人属性情報ソース16の各DBは、分析対象法人の属性情報を、公的機関が当該法人に対して付与した当該法人の固有番号である法人番号と対応づけて記憶してもよい。PC12は、分析対象法人の法人番号を指定した分析要求を業務支援装置14へ送信してもよい。業務支援装置14は、その法人番号をキーとして、個人属性情報ソース16の各DBから分析対象法人の属性情報を収集してもよい。そして、当該法人に対する金融機関の業務を支援する情報(例えば当該法人への融資の与信額や金利の情報)を生成し、PC12へ提供してもよい。

上述した実施の形態および変形例の任意の組み合わせもまた本発明の実施の形態として有用である。組み合わせによって生じる新たな実施の形態は、組み合わされる実施の形態および変形例それぞれの効果をあわせもつ。また、請求項に記載の各構成要件が果たすべき機能は、実施の形態および変形例において示された各構成要素の単体もしくはそれらの連携によって実現されることも当業者には理解されるところである。

10 情報システム、 14 業務支援装置、 16 個人属性情報ソース、 50 個人属性取得部、 52 個人スコア決定部、 54 支援情報生成部、 56 与信額決定部、 58 金利決定部、 60 支援情報提供部、 62 パラメータ設定部、 70 個人番号管理装置。

この発明は金融機関の業務を支援する装置に適用できる。

Claims (10)

- 金融機関の業務を支援する装置であって、

当該金融機関の外部に分析対象主体が保有する資産を示す資産情報を取得する取得部と、

前記取得部により取得された資産情報にもとづいて、分析対象主体に対する当該金融機関の業務内容を決定するための分析対象主体のスコアを決定するスコア決定部と、

前記スコア決定部により決定された分析対象主体のスコアにもとづいて、分析対象主体に対する当該金融機関の業務を支援するための情報を生成する支援情報生成部と、

を備えることを特徴とする情報処理装置。 - 前記支援情報生成部は、当該金融機関から分析対象主体への融資の金利であって、前記スコア決定部により決定された分析対象主体のスコアにもとづき調整された金利を示す情報を生成することを特徴とする請求項1に記載の情報処理装置。

- 前記スコア決定部は、当該金融機関の外部に分析対象主体が保有する資産が大きいほど金利が小さくなるように分析対象主体のスコアを決定することを特徴とする請求項2に記載の情報処理装置。

- 分析対象主体の資産情報は、当該金融機関とは異なる主体の装置において、公的機関から分析対象主体へ付与された固有番号に対応づけて管理されるものであり、

前記取得部は、通信網を介して前記異なる主体の装置へアクセスし、分析対象主体の固有番号をキーとして分析対象主体の資産情報を取得することを特徴とする請求項1から3のいずれかに記載の情報処理装置。 - 公的機関から分析対象主体へ付与された固有番号にもとづいて、当該金融機関において分析対象主体を識別するための第1仮番号と、当該金融機関とは異なる主体において分析対象主体を識別するための第2仮番号が予め決定され、第1仮番号と第2仮番号は所定の装置で対応づけられており、

分析対象主体の資産情報は、当該金融機関とは異なる主体の装置において、第2仮番号に対応づけて管理されるものであり、

前記取得部は、通信網を介して前記異なる主体の装置へアクセスし、分析対象主体の第1仮番号に対応づけられた第2仮番号をキーとして分析対象主体の資産情報を取得することを特徴とする請求項1から3のいずれかに記載の情報処理装置。 - 前記取得部は、当該金融機関の外部に分析対象主体が保有する負債を示す負債情報をさらに取得し、

前記スコア決定部は、前記取得部により取得された資産情報と負債情報のそれぞれにもとづいて、分析対象主体のスコアを決定することを特徴とする請求項1から5のいずれかに記載の情報処理装置。 - 資産情報が示す資産の内容に応じたスコアを導出するためのパラメータを金融機関の装置から受け付け、受け付けたパラメータを前記スコア決定部によるスコア決定処理に反映させるパラメータ設定部をさらに備えることを特徴とする請求項1から6のいずれかに記載の情報処理装置。

- 複数の金融機関の業務を支援する装置であって、

第1金融機関における分析対象主体である第1主体が第1金融機関の外部に保有する資産を示す資産情報を取得する取得部と、

前記取得部により取得された第1主体の資産情報と、第1金融機関により予め定められたパラメータとにもとづいて、第1主体に対する第1金融機関の業務内容を決定するための第1主体のスコアを決定するスコア決定部と、

前記スコア決定部により決定された第1主体のスコアにもとづいて、第1主体に対する第1金融機関の業務を支援するための情報を生成する支援情報生成部と、

を備え、

前記取得部は、第2金融機関における分析対象主体である第2主体が第2金融機関の外部に保有する資産を示す資産情報をさらに取得し、

前記スコア決定部は、前記取得部により取得された第2主体の資産情報と、第2金融機関により予め定められたパラメータとにもとづいて、第2主体に対する第2金融機関の業務内容を決定するための第2主体のスコアをさらに決定し、

前記支援情報生成部は、前記スコア決定部により決定された第2主体のスコアにもとづいて、第2主体に対する第2金融機関の業務を支援するための情報をさらに生成することを特徴とする情報処理装置。 - 金融機関の業務を支援する装置が、

当該金融機関の外部に分析対象主体が保有する資産を示す資産情報を取得するステップと、

取得された資産情報にもとづいて、分析対象主体に対する当該金融機関の業務内容を決定するための分析対象主体のスコアを決定するステップと、

決定された分析対象主体のスコアにもとづいて、分析対象主体に対する当該金融機関の業務を支援するための情報を生成するステップと、

を実行することを特徴とする情報処理方法。 - 金融機関の業務を支援する装置に、

当該金融機関の外部に分析対象主体が保有する資産を示す資産情報を取得する機能と、

取得された資産情報にもとづいて、分析対象主体に対する当該金融機関の業務内容を決定するための分析対象主体のスコアを決定する機能と、

決定された分析対象主体のスコアにもとづいて、分析対象主体に対する当該金融機関の業務を支援するための情報を生成する機能と、

を実現させるためのコンピュータプログラム。

Priority Applications (17)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|