WO2017090468A1 - 学習模型 - Google Patents

学習模型 Download PDFInfo

- Publication number

- WO2017090468A1 WO2017090468A1 PCT/JP2016/083624 JP2016083624W WO2017090468A1 WO 2017090468 A1 WO2017090468 A1 WO 2017090468A1 JP 2016083624 W JP2016083624 W JP 2016083624W WO 2017090468 A1 WO2017090468 A1 WO 2017090468A1

- Authority

- WO

- WIPO (PCT)

- Prior art keywords

- account

- columns

- amount

- column

- balance

- Prior art date

- Legal status (The legal status is an assumption and is not a legal conclusion. Google has not performed a legal analysis and makes no representation as to the accuracy of the status listed.)

- Ceased

Links

Images

Classifications

-

- G—PHYSICS

- G09—EDUCATION; CRYPTOGRAPHY; DISPLAY; ADVERTISING; SEALS

- G09B—EDUCATIONAL OR DEMONSTRATION APPLIANCES; APPLIANCES FOR TEACHING, OR COMMUNICATING WITH, THE BLIND, DEAF OR MUTE; MODELS; PLANETARIA; GLOBES; MAPS; DIAGRAMS

- G09B19/00—Teaching not covered by other main groups of this subclass

- G09B19/18—Book-keeping or economics

Definitions

- the present invention relates to a teaching material for double-entry bookkeeping learning.

- Double-entry bookkeeping is a bookkeeping method in which the relationship of average balance is always established when transactions in a business activity are recorded on two sides simultaneously with the cause and result of the same amount, and the accounts are summarized, and is consistently on the left side. Is called debit and the right side is called credit.

- journal In double-entry bookkeeping, the recording method is called journal, and the two sides are debited and credited, and the account item and the amount are described so that the average of the balance is established.

- the amount of the account item described in the debit is the account amount.

- the amount of the account item described in the credit to the debit of the item is a rule of recording in the credit of the account item, and this work is called posting.

- Double-entry bookkeeping has special features such as addition calculation and a mechanism that keeps the average loan balance.

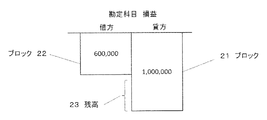

- the learner understands that the blocks 21 and 22 have a height proportional to the amount of the account item. It takes time and effort to draw a chart like the above, write account titles and amounts, or repeat calculation.

- the present invention creates a model of account items, amounts and forms that constitute double-entry bookkeeping, so that the learner does not have to write the figures of the charts such as blocks, the characters of the account items, and the numbers of the amounts in advance, instead of the blocks.

- the amount is written, using a bill with a height proportional to the amount of the amount of the account item, and further writing the account item and amount on the front and back, making the background or text color different, and

- the identification of the tag is simplified, including making the background or character color different for each element to which the listed account item belongs.

- the board that mimics the entire account is an asset and expense account vertically on the left side so that you can visually grasp the mechanism that keeps the balance average always by looking at the movement of the account by journal entry and posting Two columns, debit and credit, and two columns, debt, net asset, and revenue, debit and credit on the right side, and above or below the four columns, an account amount increase column, and an account

- a frame for only two columns of debits and credits of account items not included in the above five elements above or below the four columns is solved by the inventions of claims 1 and 2 and accommodated in one layout.

- the board can be laid out in advance with letters and frames with vertical scales at regular intervals, and if necessary, the amount of money can be measured by length to facilitate placement and simple calculations. it can.

- the learner can carefully check the movement of the double-entry bookkeeping because the bill is moved and placed on the board while checking manually.

- the learner can learn the double-entry bookkeeping mechanism without having to write all the figures of the charts and account items such as blocks, and the numbers of the monetary amounts.

- one combination of debiting the correct journal between the accounts and increasing / decreasing each account amount in the credit is placed in the column placed on the board.

- the column corresponding to the increase in the account item amount among 4 columns is marked with an increase including “+”, and the column corresponding to the decrease in the amount is marked with a decrease including “ ⁇ ”.

- the table of 4 rows and 4 columns can be used to add a mark indicating that the amount of increase or decrease of the account amount.

- the balance average is calculated for the entire account by journalizing and posting. It is possible to learn while confirming how the amount of the account item increases and decreases while being maintained.

- the placement of the elements on the board is fixed if you look at the tags placed on the board by posting, so it will be posted correctly You can check if it was done.

- the board that mimics the entire account, the assets, expenses, liabilities, net assets, and revenue account items are stored in two columns on each side, a total of four columns, and for accounts that do not belong to any of the elements, Both the debit and credit lines are stored in one layout, and the entire account item and the average loan balance can be expressed.

- the scales are written evenly in the vertical direction.

- Reference numeral 1 denotes a layout board simulating a journal, which has two columns of debits and credits.

- the left column is the asset column on the left, the debit and credit columns of the expense account column, the vertical column is the debt, net asset, and revenue account column on the right. There are two columns of debit and credit.

- a mark 8 is placed above each column, and “+” corresponds to a column corresponding to an increase in the amount of the corresponding account item, corresponding to the pattern of journal entries between one account item, and corresponds to a decrease. "-" Is added to the column.

- the left two columns and right two columns are divided for each account item. If the left column is the upper left side, the right column is the upper right side. Is marked.

- 15 is an account area for internal use.

- the two columns of debit and credit of account withdrawals that do not belong to assets, expenses, liabilities, net assets, and profits are out of the four columns. And the remaining two inner rows are marked with a mark indicating that the cards cannot be placed.

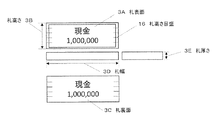

- FIG. 2 is an explanatory diagram of the shape of the bill.

- the name of the account item and the amount of money are written in black on both the front and back surfaces, so that it can be easily selected from the bill set 17.

- the dimensions of the bills are the same for all the widths of the bills, and the thicknesses are the same, and the height is proportional to the written amount. When a plurality of bills are stacked vertically, the height represents the total amount.

- the front side is color-coded for each element to which the account item written on the tag belongs, the asset is cream, the debt is blue, the net asset is green, the income is pink, the expense is yellow, and the back is white .

- 16 is a scale, which is marked on the front and back near the side to visually indicate the height of the bill, and if placed and referenced, the amount corresponding to the balance is easy to understand. .

- Reference numeral 4 denotes a bill, which is written as “capital” as an account item belonging to net assets and “1,000,000” as a monetary amount in black letters on a green background.

- Reference numeral 5 denotes a bill, which is written as “cash” as an account item belonging to the asset and “1,000,000” as a monetary amount, in black letters on the cream area.

- Reference numeral 9 denotes a bill, which is written as “cash” as an account item belonging to the asset and “1,200,000” as a monetary amount in black on the cream.

- Reference numeral 11 denotes a layout board simulating a balance trial calculation table, and has two columns of debits and credits.

- journal 1 As a result of the journal accompanying the transaction assumed in the learning, one journal is arranged in the journal 1 by imitating one journal with a pair of bills.

- the bill 4 is placed on the credit of the journal 1 and the bill 5 is placed on the debit of the journal 1.

- journal contents of the journal 1 are moved and arranged by imitating the transfer to the account item.

- the bill 4 in the credit is moved and arranged manually 6 to the credit position of the corresponding account item in the general ledger 2 according to the written account item.

- the bill 5 in the debit is moved and arranged manually 7 to the debit position of the corresponding account item in the general ledger 2 according to the written account item.

- a bill of all account items with an amount corresponding to the balance of all account items is manually selected from the bill set 17 as shown in FIG. 3.

- the bill 9 is moved manually 10 and placed in the debit of the cash account item in the balance trial calculation table 11.

Landscapes

- Business, Economics & Management (AREA)

- Entrepreneurship & Innovation (AREA)

- Engineering & Computer Science (AREA)

- Physics & Mathematics (AREA)

- Economics (AREA)

- General Business, Economics & Management (AREA)

- Development Economics (AREA)

- Accounting & Taxation (AREA)

- Educational Administration (AREA)

- Educational Technology (AREA)

- General Physics & Mathematics (AREA)

- Theoretical Computer Science (AREA)

- Financial Or Insurance-Related Operations Such As Payment And Settlement (AREA)

Applications Claiming Priority (2)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| JP2015-006292U | 2015-11-26 | ||

| JP2015006292U JP3202685U (ja) | 2015-11-26 | 2015-11-26 | 学習模型 |

Publications (1)

| Publication Number | Publication Date |

|---|---|

| WO2017090468A1 true WO2017090468A1 (ja) | 2017-06-01 |

Family

ID=55346288

Family Applications (1)

| Application Number | Title | Priority Date | Filing Date |

|---|---|---|---|

| PCT/JP2016/083624 Ceased WO2017090468A1 (ja) | 2015-11-26 | 2016-11-07 | 学習模型 |

Country Status (2)

| Country | Link |

|---|---|

| JP (1) | JP3202685U (enExample) |

| WO (1) | WO2017090468A1 (enExample) |

Cited By (1)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| WO2018135669A1 (ja) * | 2018-01-22 | 2018-07-26 | 誠吾 川嶋 | 学習模型 |

Citations (5)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| GB824971A (en) * | 1957-01-18 | 1959-12-09 | Joseph Rispoli | Visual aid to the teaching of bookkeeping |

| JPH06102818A (ja) * | 1992-09-24 | 1994-04-15 | Masanori Masumoto | 簿記練習具 |

| JP2001051588A (ja) * | 1999-08-10 | 2001-02-23 | Hiromichi Kato | 学習装置及び学習方法 |

| US20020164561A1 (en) * | 1999-11-05 | 2002-11-07 | Neville Joffe | Method of teaching financial management |

| JP3176596U (ja) * | 2012-03-29 | 2012-06-28 | 孝一 蒲池 | トレーニング用仕訳カード |

-

2015

- 2015-11-26 JP JP2015006292U patent/JP3202685U/ja not_active Expired - Lifetime

-

2016

- 2016-11-07 WO PCT/JP2016/083624 patent/WO2017090468A1/ja not_active Ceased

Patent Citations (5)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| GB824971A (en) * | 1957-01-18 | 1959-12-09 | Joseph Rispoli | Visual aid to the teaching of bookkeeping |

| JPH06102818A (ja) * | 1992-09-24 | 1994-04-15 | Masanori Masumoto | 簿記練習具 |

| JP2001051588A (ja) * | 1999-08-10 | 2001-02-23 | Hiromichi Kato | 学習装置及び学習方法 |

| US20020164561A1 (en) * | 1999-11-05 | 2002-11-07 | Neville Joffe | Method of teaching financial management |

| JP3176596U (ja) * | 2012-03-29 | 2012-06-28 | 孝一 蒲池 | トレーニング用仕訳カード |

Cited By (1)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| WO2018135669A1 (ja) * | 2018-01-22 | 2018-07-26 | 誠吾 川嶋 | 学習模型 |

Also Published As

| Publication number | Publication date |

|---|---|

| JP3202685U (ja) | 2016-02-18 |

Similar Documents

| Publication | Publication Date | Title |

|---|---|---|

| US6767210B2 (en) | Method of teaching financial management | |

| JP3202685U7 (enExample) | ||

| JP3202685U6 (enExample) | ||

| Cole | The fundamentals of accounting | |

| JP3202685U (ja) | 学習模型 | |

| JP3176596U (ja) | トレーニング用仕訳カード | |

| CN102177536A (zh) | 会计教具 | |

| JP3219827U (ja) | 学習模型 | |

| JP6255378B2 (ja) | 会計学習教材及び会計学習教材の使用方法 | |

| Kohler et al. | Principles of accounting | |

| WO2018135669A1 (ja) | 学習模型 | |

| US20060172265A1 (en) | Method of and means for teaching accounting concepts and procedures | |

| Lee | A Scottish Contribution to Accounting History | |

| JP6898632B2 (ja) | ボードゲーム具 | |

| Kalra et al. | Connections Maths: Stage 5.3/5.2/5.1 | |

| McKinsey | Bookkeeping and accounting | |

| TWM656558U (zh) | 會計教學用具 | |

| Mari et al. | The Spread of the Double-Entry Bookkeeping Method in the Sixteenth Century: The Quaderno doppio col suo giornale novamente composto et dilegentissimamente ordinato secondo il costume di Venetia of Dominico Manzoni (Venice, 1540) | |

| Sheaffer | Metropolitan system of bookkeeping | |

| CA2289153C (en) | A method of teaching financial management | |

| Nitkin et al. | Leveraging spreadsheets to learn the mechanics of accounting | |

| Titus | Unit organization of two topics for a class in bookkeeping | |

| Sheaffer | Metropolitan system of bookkeeping: embracing theory and practice of bookkeeping and accounting for high schools, parochial schools, academies and all other schools teaching the subject | |

| Byrd et al. | Teaching the Statement of Changes in Financial Position—A Worksheet Approach | |

| Hindman | Development of a terminal course of accounting for the Mangum Junior College |

Legal Events

| Date | Code | Title | Description |

|---|---|---|---|

| 121 | Ep: the epo has been informed by wipo that ep was designated in this application |

Ref document number: 16868416 Country of ref document: EP Kind code of ref document: A1 |

|

| NENP | Non-entry into the national phase |

Ref country code: DE |

|

| 122 | Ep: pct application non-entry in european phase |

Ref document number: 16868416 Country of ref document: EP Kind code of ref document: A1 |