JP5592683B2 - Life design support program - Google Patents

Life design support program Download PDFInfo

- Publication number

- JP5592683B2 JP5592683B2 JP2010075551A JP2010075551A JP5592683B2 JP 5592683 B2 JP5592683 B2 JP 5592683B2 JP 2010075551 A JP2010075551 A JP 2010075551A JP 2010075551 A JP2010075551 A JP 2010075551A JP 5592683 B2 JP5592683 B2 JP 5592683B2

- Authority

- JP

- Japan

- Prior art keywords

- repayment

- mortgage

- amount

- transition

- program

- Prior art date

- Legal status (The legal status is an assumption and is not a legal conclusion. Google has not performed a legal analysis and makes no representation as to the accuracy of the status listed.)

- Active

Links

Images

Description

本発明は、生活設計支援プログラム及び生活設計支援システムに関する。 The present invention relates to a life design support program and a life design support system.

家族を有する世帯主にとって住宅購入費は、生涯を通じて一般的に最も高い支出構成比を占めている。このため、住宅の購入時期、住宅ローンの借入額、返済期間及び返済プラン等は、世帯が望む生活設計において最も重要な選択事項となっている。 For householders with families, housing purchases generally account for the highest proportion of spending throughout life. For this reason, the purchase time of a house, the borrowing amount of a mortgage, the repayment period, the repayment plan, etc. are the most important selection items in the lifestyle design desired by the household.

従来、利用者が安心して住宅ローンの設定、返済ができるようにするための各種解析ツール・ソフトが知られている。例えば特許文献1には、入力された単位年毎の住宅ローン借入額情報、住宅ローン返済期間情報及び住宅ローン金利率情報から単位年毎の住宅ローン返済額情報を算出し、入力された単位年毎の生涯予想収入額情報、生涯予想支出額情報、及び算出された前記住宅ローン返済額情報から単位年毎の生涯予想金融資産情報を算出し、前記住宅ローン返済額情報及び前記生涯予想金融資産情報を単位年毎に一同に表示する生涯金融資産試算システムが開示されている。

Conventionally, various analysis tool software for enabling a user to set and repay a mortgage with confidence is known. For example, in

しかし、従来の各種解析ツール・ソフトは、住宅ローン金利の上昇や担保地価の下落等の社会的な経済環境の変動によるリスクを勘案したものではなかった。また、近年、ライフスタイルが多様化しているにも関わらず、利用者の個別の事情、例えば家族構成、将来の子供の誕生やそれに伴う教育費等の変動を詳細に反映したものでもなかった。こうした個人的な経済状況の変動要因を加味しながら、世帯主にとって最適かつ合理的な生活設計をするには、ファイナンシャルプランナーやライフプランナー等の専門的な知識や経験を有する者によるコンサルティングを必要としていた。 However, various analysis tools and software in the past did not take into account risks due to changes in the social economic environment such as rising mortgage interest rates and falling collateral land prices. Moreover, despite the diversification of lifestyles in recent years, it has not been a detailed reflection of changes in individual circumstances of users, such as family composition, future birth of children and associated educational expenses. In order to design an optimal and rational life plan for the householder while taking into account these factors of fluctuations in personal economic conditions, consulting by persons with specialized knowledge and experience such as financial planners and life planners is required. It was.

従って、本発明の目的は、利用者の個人的な経済状況及び社会的な経済環境の変動要因を即応的に加味し、世帯主が望む将来の生活設計に基づく住宅ローンの借り換え、借り入れやローン返済の方法等の選択についての合理的な判断材料を利用者に提供し得る生活設計支援プログラム及び生活設計支援システムを提供することにある。 Therefore, the object of the present invention is to take into account the fluctuation factors of the user's personal economic situation and social economic environment promptly and refinance the mortgage based on the future life design desired by the householder. It is an object of the present invention to provide a life design support program and a life design support system that can provide a user with rational judgment materials for selecting a repayment method.

本発明の一態様は、上記目的を達成するため、コンピュータを、

記憶手段に記憶されている利用者に関する情報のうち時期とともに入力された世帯収入に関する情報に基づいて当該利用者の収入の推移を試算する収入推移試算手段と、

前記記憶手段に記憶されている経済指標に基づく予測情報のうち住宅ローン金利の予測情報、及び利用者が選択する住宅ローンの借り換え時期と借り換え後のローン種別を含む住宅ローンの返済条件に基づいて当該利用者の住宅ローン返済額を試算する住宅ローン返済額試算手段と、

前記記憶手段に記憶されている前記利用者に関する情報のうち時期とともに入力された世帯支出に関する情報、前記予測情報及び前記住宅ローン返済額試算手段が試算する前記住宅ローン返済額に基づいて当該利用者の支出の推移を試算する支出推移試算手段と、

前記収入推移試算手段が試算する収入推移、前記支出推移試算手段が試算する支出推移及び前記住宅ローン返済額試算手段が試算する返済額の推移を年次毎に日本人の平均寿命まで一同に表示部に表示する生涯収支推移表示手段として機能させるための生活設計支援プログラムであって、

前記住宅ローン返済額試算手段は、変動金利、所定年の固定金等のローン種別を含む前記住宅ローンの返済条件の入力を受け付ける住宅ローン設定条件入力表画面を前記表示部に表示し、入力された前記住宅ローンの返済条件に基づいて試算した住宅ローンの返済総額を前記住宅ローン設定条件入力表画面に表示し、入力された前記住宅ローンの返済条件に基づいて試算した年次毎の毎月の住宅ローン返済額の返済グラフによる推移を前記表示部に表示し、

前記コンピュータを、

前記収入推移試算手段が試算する収入推移、前記支出推移試算手段が試算する支出推移及び前記住宅ローン返済額試算手段が試算する返済額の推移に基づいて、住宅ローンの借り換え、借り入れ、又は繰上げ返済による貯蓄残高が減少する時期と自由使途資金を算出し、自由使途資金に対応した必要保障額を算出する必要保障額算出手段と、

保険設計時または保険募集の提案時に、前記貯蓄残高が減少する期間と前記必要保障額を提示するリスク提示手段としてさらに機能させるための生活設計支援プログラムを提供する。

According to one embodiment of the present invention, in order to achieve the above object, a computer is provided.

Revenue transition estimation means for calculating transition of the income of the user based on information on household income input with the time out of the information on the user stored in the storage means;

Based on the prediction information of the mortgage interest rate among the prediction information based on the economic index stored in the storage means, and the mortgage repayment condition including the mortgage refinancing time selected by the user and the loan type after refinancing A mortgage repayment amount calculation means for calculating the mortgage repayment amount of the user;

Of the information on the user stored in the storage means, information on household expenditure input with time, the prediction information, and the mortgage repayment amount calculated by the mortgage repayment amount calculation means, the user Expenditure trend calculation means to estimate the trend of expenditure,

The revenue transition estimated by the income transition estimation means, the expenditure transition estimated by the expenditure transition estimation means, and the repayment amount estimated by the mortgage repayment amount estimation means are displayed all together until the average life span of the Japanese for each year. A life design support program for functioning as a lifetime balance display means to be displayed in the department,

The mortgage repayment amount calculation means displays a mortgage setting condition input table screen for accepting input of the mortgage repayment conditions including a variable interest rate, a loan type such as a fixed amount for a predetermined year on the display unit, and is input said the repayment total amount of housing loans was estimated on the basis of the repayment terms of the mortgage and displayed on the mortgage setting condition input table screen, the annual each of which has been estimated on the basis of the repayment terms of the input the mortgage Display the transition of the monthly mortgage repayment amount by the repayment graph on the display section ,

The computer,

Refinancing, borrowing, or prepayment of a mortgage based on the revenue transition estimated by the revenue transition estimation means, the expenditure transition estimated by the expenditure transition estimation means, and the repayment amount estimated by the mortgage repayment amount estimation means A required security amount calculation means for calculating a period when the savings balance due to and a free-use funds are calculated, and calculating a required security amount corresponding to the free-use funds,

Provided is a life design support program for further functioning as a risk presenting means for presenting the period during which the savings balance decreases and the required security amount at the time of insurance design or insurance solicitation .

本発明によれば、利用者の個人的な経済状況及び社会的な経済環境の変動要因を即応的に加味し、世帯主が望む将来の生活設計に基づく住宅ローンの借り換え、借り入れやローン返済の方法等の選択についての合理的な判断材料を利用者に提供することができる。 According to the present invention, the user's personal economic situation and social economic environment fluctuation factors are promptly taken into account, and mortgage refinancing, borrowing and loan repayment based on the future life design desired by the householder It is possible to provide a user with a rational judgment material regarding selection of a method or the like.

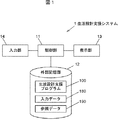

[生活設計支援システムの構成]

図1は、本発明の実施の形態に係る生活設計支援システムのハードウエアの構成例を示すブロック図である。この生活設計支援システム1は、制御部11と、外部記憶部12と、表示部13と、入力部14とを備えている。

[Configuration of life design support system]

FIG. 1 is a block diagram illustrating a hardware configuration example of a lifestyle design support system according to an embodiment of the present invention. The life

制御部11は、CPUと、内部メモリと、外部記憶部12等との制御信号及びデータ信号の入出力制御を行う周辺デバイスインタフェースと、ビデオ制御ボード等とを備え、これらが内部バスで接続されている。

The

外部記憶部12は、磁気ハードディスクや不揮発メモリ等のデータの読み書き可能なストレージ媒体から構成される。外部記憶部12には、制御部11が演算処理に必要な後述する各種プログラム(生活設計支援プログラム100等)やデータ(入力データ180、参照データ190等)が記憶される。

The

ここで、入力データ180としては、例えば住宅購入費、住宅ローンの借入額、ローン返済期間(本明細書では「借入期間」又は「住宅ローン利用年数」ともいう。)、返済プラン(本明細書では「ローン種別」ともいい、固定金利、変動金利等が含まれる。)、世帯情報(家族構成、年齢又は生年月日、住所等)、年収、生活費、年金、保険、資産等の個人的な情報が相当する。また、参照データ190としては、例えば、住宅ローン金利、物価指数、地域ごとの地価等の社会的な経済指標情報が相当し、当該情報は専門的視点から将来の上昇又は下落を見通した予測値も含めて最新の値が随時更新可能に外部記憶部12に記憶される。

Here, as the

なお、入力データ180及び参照データ190として挙げたこれらの情報は、本実施の形態による解析において勘案する情報の一例であり、これら全ての情報が本発明における解析に必須の情報というわけではない。また、これらの情報のみに限定されることを意図するものでもない。

Note that the information listed as the

表示部13は、例えばCRTや液晶ディスプレイ等の画像表示装置であり、図示しないタッチパネル等の入力手段を付帯するものでもよい。また、表示部13は、制御部11が演算処理して生成した画面を表示する。

The

入力部14は、例えばキーボード、マウス等の入力装置から構成される。利用者が入力部14を介して入力された情報は、入力データ180として制御部11の外部記憶部12に記憶される。また、タッチパネル(不図示)を備える表示部13と連携して、利用者が選択することで情報を入力してもよい。

The

(生活設計支援プログラム100)

本実施の形態の生活設計支援プログラム100は、図1に示した生活設計支援システム1の外部記憶部12に予め記憶される。なお、この生活設計支援プログラム100は、図示しない情報記憶媒体に記憶され、外部記憶部12にインストールされるもの、又はインターネット等の双方向電気通信回線を介して管理サーバからダウンロードされるものでもよい。

(Life design support program 100)

The life

また、生活設計支援プログラム100は、ASP(アプリケーション・サービス・プロバイダ)のサーバ上で動作するものでもよい。この場合には、当該ASPサーバのローカルの記憶部に最新の住宅ローン金利(変動率等の予測値を含む)等の参照データ190が随時、更新可能に記憶される。この構成によれば、利用者は、自己の所有するパーソナルコンピュータ又はプロバイダの窓口に設置される端末装置等からASPのホームページにインターネット又は専用回線を介してアクセス(ログイン)することにより、次に説明する世帯収支、住宅ローン及び保険の見直し等に関する最新の予測値に基づく高精度の各種シミュレーション及び解析サービスを簡便に受けることができる。

The life

図2は、生活設計支援システム1のソフトウエア構成を階層的に示す図である。生活設計支援プログラム100は、システム制御プログラムとしてメイン制御プログラム101と、表示制御プログラム102と、入力制御プログラム103とを備え、各種解析用のプログラムとして、生涯資金収支解析プログラム110と、住宅費用解析プログラム120とを備えている。

FIG. 2 is a diagram hierarchically showing the software configuration of the lifestyle

(メイン制御プログラム101)

メイン制御プログラム101は、次に説明する表示制御プログラム102、入力制御プログラム103及び生涯資金収支解析プログラム110等の各プログラムを制御部11にロードすることにより、CPUがこれらのプログラムによる演算処理を実行できる状態に制御する。このとき、各プログラムに対応する複数のタスクが生成される。また、メイン制御プログラム101は、利用者による情報の入力や解析結果等に応じて、適宜、CPUが演算処理すべきタスクをタイムシェアリング方式(時間分割方式)により切り換えて実行するように構成されている。

(Main control program 101)

The

(表示制御プログラム102)

表示制御プログラム102は、メイン制御プログラム101の制御下で、各種選択メニュー画面、解析結果を示す表及びグラフ等の画面を生成し、表示部13にこれらの画面を表示する制御を行うように構成されている。

(Display control program 102)

The

(入力制御プログラム103)

入力制御プログラム103は、利用者が入力部14を介して入力した情報をメイン制御プログラム101の制御下で外部記憶部12に入力データ180として記憶、更新するように構成されている。

(Input control program 103)

The

生活設計支援プログラム100は、起動すると、初期のメイン選択メニュー画面が表示部13に表示され、利用者が生涯資金収支解析又は住宅費用解析のいずれかを選択できるように構成されている。

When the life

メイン制御プログラム101は、利用者がメイン選択メニュー画面において、生涯資金収支解析のアイコンを入力部14を介してクリックすると、生涯資金収支解析プログラム110が起動されるように構成されている。

The

(生涯資金収支解析プログラム110)

生涯資金収支解析プログラム110は、サブプログラムとして利用者情報設定プログラム111と、世帯収入推移試算プログラム112と、世帯支出推移試算プログラム113と、生涯収支推移表示プログラム118とを備えている。

(Lifetime funds balance analysis program 110)

The lifetime fund

(利用者情報設定プログラム111)

図3は、利用者世帯に関する情報入力表の画面の一例を示す図である。生涯資金収支解析プログラム110が起動すると、初めに利用者情報設定プログラム111が起動され、図3(a)に示されるような家族情報に関する情報入力表の画面が表示部13に表示される。

(User information setting program 111)

FIG. 3 is a diagram illustrating an example of an information input table screen regarding a user household. When the lifetime fund

例えば、利用者の世帯構成情報として、世帯主、配偶者、子供のそれぞれの氏名、生年月日、現年齢、性別を所定の欄内に入力部14を介して入力することで、各情報が入力データ180として外部記憶部12に記憶される。また、現時点では家族の構成員ではないが将来構成員となる子供が誕生する予定がある場合に対応して、その予定される年をゼロ歳とした場合の現時点での仮想の年齢であるマイナス年齢を入力することで、誕生前の子供についての情報を入力できる。

For example, as the household composition information of the user, each name is entered by inputting the name, date of birth, current age, and sex of each householder, spouse, and child in a predetermined column via the

また、次のステップでは、図3(b)に示されるような世帯収入に関する情報入力表の画面が表示部13に表示される。

In the next step, an information input table screen related to household income as shown in FIG. 3B is displayed on the

例えば、現在の年収金額、ステージアップ(昇格)の予定年齢と昇給額、定年退職金額等が所定の欄内に入力できるように構成されている。また、給与所得以外にもその他の収入として、例えば不動産、株式配当及び資産贈与等の個人資産についても世帯会計(家計)に組み入れる場合には、その金額と取得時期とともに入力できる。 For example, the current annual income, stage up (promotion) scheduled age and salary increase, retirement retirement amount, etc. can be entered in a predetermined field. In addition to salary income, personal assets such as real estate, stock dividends, and asset gifts can be entered together with the amount and acquisition date when they are included in household accounting (household).

また、次のステップでは、図3(c)示されるような現在有している積立等の金融資産残高に関する情報入力表の画面が表示部13に表示される。例えば、住宅準備資金、シニアライフ積立、学資準備積立等の金額が所定の欄内に入力できる。

Further, in the next step, an information input table screen related to the financial asset balance such as funding as shown in FIG. 3C is displayed on the

また、次のステップでは、図3(d)示されるような世帯支出に関する情報入力表の画面が表示部13に表示される。例えば、現在の年間の生活費、住宅関連費(賃貸の場合は家賃、管理費等、戸建の場合は修繕費等)、固定資産税、所得税、住民税、養育費・教育費、金融資産積立費、保険料(社会保険、生命保険、火災保険、自動車保険等)、レジャー費(趣味、旅行等)、自家用車維持費(自動車ローン、燃料費、車検費等)等の金額が所定の欄内に入力できる。 In the next step, a screen of an information input table relating to household expenditure as shown in FIG. For example, current annual living expenses, housing-related expenses (rent, management expenses, etc. for rent, repair expenses, etc. for detached houses), fixed asset tax, income tax, resident tax, childcare / education expenses, financial asset accumulation Costs, insurance premiums (social insurance, life insurance, fire insurance, car insurance, etc.), leisure expenses (hobbies, travel, etc.), private car maintenance costs (car loans, fuel costs, car inspection expenses, etc.) Can be entered in.

これらの利用者情報の入力事項は、利用者が任意に選択できるが、現時点でわかっている事項をより多く正確に入力することで、より精度の高い生涯資金収支(ライフキャッシュフロー)を試算することができる。 These user information items can be selected arbitrarily by the user, but more accurate life balance (life cash flow) is estimated by inputting more information known at the present time. be able to.

(世帯収入推移試算プログラム112)

生涯資金収支解析プログラム110は、利用者による情報の入力の完了が操作指示されると、世帯収入推移試算プログラム112を起動するように構成されている。世帯収入推移試算プログラム112は、上述の世帯収入に関する入力情報に基づいて、年次ごとの世帯収入の推移を試算して生涯収入推移データを作成するように構成されている。

(Household income transition estimation program 112)

The lifetime fund

世帯収入の試算にあたっては、参照データ190として外部記憶部12に予め記憶されている定期昇給額の統計上の平均値が勘案される。すなわち、世帯収入推移試算プログラム112は、外部記憶部12から読み取った定期昇給額の平均値を世帯主が定年退職を迎える年までの毎年次の年収金額に加算するように構成されている。

In the trial calculation of the household income, the statistical average value of the periodic salary increase stored in advance in the

(世帯支出推移試算プログラム113)

世帯収入推移試算プログラム112による処理が終了すると、世帯支出推移試算プログラム113が起動される。世帯支出推移試算プログラム113は、そのサブプログラムとして基本生活費シミュレーションプログラム114と、教育費シミュレーションプログラム115と、年金保険料シミュレーションプログラム116と、税金シミュレーションプログラム117とを備えている。

(Household Expenditure Trend Estimation Program 113)

When the processing by the household income

世帯支出推移試算プログラム113は、初めに基本生活費シミュレーションプログラム114を起動して、入力データ180として記憶された現時点の生活費及び世帯構成情報、並びに参照データ190として予め記憶されている現時点の物価指数、将来の物価予測指数、年齢ごとの平均的な個人消費額等を勘案して、世帯の基本生活費(食料、衣料及び生活消耗品等にかかる費用の総額)の推移を年次ごとにシミュレーションするように構成されている。

The household expenditure transition

図4は、世帯支出に関するシミュレーション条件に関し、予め参照データ190として外部記憶部12に記憶されている情報の一例を示す図である。

FIG. 4 is a diagram illustrating an example of information stored in advance in the

(基本生活費シミュレーションプログラム114)

基本生活費シミュレーションプログラム114は、各世帯構成員ごとに基本生活費の推移を日本人の統計上の平均余命年齢まで試算してその合計を世帯の基本生活費として算出するように構成されている。そして、その各世帯構成員における生活費の試算にあたっては、当該年次に対応する当該世帯構成員の年齢及び性別における統計上の平均的な生活費の額に、当該年次における物価予測指数を重み付けした額を当該年次における当該世帯構成員の基本生活費として算出するように構成されている。

(Basic cost of living simulation program 114)

The basic living

(教育費シミュレーションプログラム115)

世帯支出推移試算プログラム113は、次のステップにおいて教育費シミュレーションプログラム115を起動して、これから教育を受ける世帯構成員ごとに最終学歴の卒業年まで年次ごとに教育費の推移をシミュレーションするように構成されている。

(Education fee simulation program 115)

The household expenditure

具体的に教育費シミュレーションプログラム115による教育費の試算にあたっては、表示部13の選択メニュー画面を介して選択された各教育機関の種別(例えば公立・私立中学、公立・私立高校、国立・私立大学又は高等専門学校か等の別)や分野別(例えば理工系、医学系、文科系、芸術系又は体育系か等の別)ごとに、参照データ190として予め記憶されている当該年次に対応する当該年齢における平均的な教育費の額を当該年次における教育費として算出する。

Specifically, in estimating the educational expenses by the educational

(年金保険料シミュレーションプログラム116)

世帯支出推移試算プログラム113は、次のステップにおいて年金保険料シミュレーションプログラム116を起動して、年次ごとに支払うべき保険料の推移をシミュレーションするように構成されている。年金保険料シミュレーションプログラム116は、表示部13に表示された情報入力表の画面を介して利用者が入力した現時点で加入契約している保険の種別(生命保険、火災保険、自動車保険等)及び社会保険(健康保険、厚生年金保険、雇用保険)の保険料に所定の変動率を年次ごとにべき乗算した額を当該年次の保険料金額として算出するように構成されている。更に年金保険料シミュレーションプログラム116は、利用者が積み立てている個人年金積立基金(例えばシニアライフ積立、学資準備積立等)について所定の変動率を年次ごとべき乗算して金額を前記算出した保険料金額に加算するように構成されている。

(Pension premium simulation program 116)

The household expenditure transition

各種保険や年金の変動率の予測情報は、参照データ190として外部記憶部12に予め記憶されており、年金保険料シミュレーションプログラム116による処理において適宜読み取られる。また社会保険料の試算にあたっては、年金保険料シミュレーションプログラム116は、前述の世帯収入推移試算プログラム112と連携して、算出された被保険者の年次ごとの年収金額に応じた法定の保険税率を乗算して求めた金額を当該年次の社会保険料として算出する。

Prediction information of the fluctuation rates of various insurances and pensions is stored in advance in the

(税金シミュレーションプログラム117)

世帯支出推移試算プログラム113は、次のステップにおいて税金シミュレーションプログラム117を起動して、年次ごとに支払う税金の推移をシミュレーションするように構成されている。税金シミュレーションプログラム117は、税の種別(所得税、住民税、固定資産税、相続・贈与税等)ごとに納付額を試算するよう構成されている。

(Tax simulation program 117)

The household expenditure

例えば所得税額の試算にあたっては、税金シミュレーションプログラム117は、前述の世帯収入推移試算プログラム112と連携して得られる被課税者の年収金額から法定の給与所得控除を減算することで所得金額を算出し、外部記憶部12に入力データ180として記憶されている世帯構成員の情報に基づいて社会保険控除、生命保険控除、配偶者控除及び扶養者控除等を必要に応じて所得金額から控除して求めた課税所得に、参照データ190に記憶されている法定の税率を乗算することで、当該年次の所得税納付額が試算する。

For example, when calculating the income tax amount, the

また、住民税額の試算にあたっては、税金シミュレーションプログラム117は、同様に算出された当該年次の課税所得に法定の税率を乗算した所得税割と一定の均等割を加算した金額を当該年次の納付額として試算する。

In addition, when calculating the resident tax amount, the

また、所有する土地の固定資産税額の試算にあたっては、税金シミュレーションプログラム117は、その土地の地目(例えば宅地、農地又は山林等)に応じてその地域の公示地価と所有地の面積から土地資産評価額が算出される。そして、算出された土地資産評価額と予め参照データ190に記憶されているその地域の地価の予測値に基づいて年次ごとの土地に係る固定資産税額を算出する。

In addition, when calculating the property tax amount of land owned, the

また、所有する建物の固定資産税額の試算にあたっては、税金シミュレーションプログラム117は、その建物の購入価格からその建物の構造(例えば木造、軽量鉄骨、鉄筋コンクリート等)に応じて年次ごとに一定の比率で減価償却した建物資産評価額に基づいて年次ごとの建物に係る固定資産税額を算出する。

Moreover, in the trial calculation of the property tax amount of the owned property, the

世帯支出推移試算プログラム113は、各シミュレーションプログラムで試算した前述の生活費、教育費、年金保険料及び税金の推移とともに、後述するローン返済額シミュレーションプログラム122と連携して得られる年次ごとのローン返済額を生涯支出推移データに加えるように構成されている。また、利用者世帯の事情に対応して、例えば新車購入費、海外旅行費等のローンや積立、医療介護費、冠婚葬祭等の交際費など、臨時的、単発的な出費についても情報入力表の画面を通じて個別に入力可能とされており、生涯支出推移の試算に組み込むことができるように構成されている。

The Household Expenditure Trend

生涯資金収支解析プログラム110は、前述の世帯収入推移試算プログラム112及び世帯支出推移試算プログラム113による試算処理が終了すると、生涯収支推移表示プログラム118を起動するように構成されている。

The lifetime fund

(生涯収支推移表示プログラム118)

生涯収支推移表示プログラム118は、世帯収入推移試算プログラム112により作成された生涯収入推移データを年次(又は世帯主の年齢)を横軸とする折れ線グラフの画面データに変換するように構成されている。また、生涯収支推移表示プログラム118は、世帯収支出推移試算プログラム113により作成された生涯支出推移データを年次(又は世帯主の年齢)を横軸として、各細目(基本生活費、教育費、各種税金等)ごとに比率を色分けした棒グラフの画面データに変換するように構成されている。

(Lifetime balance transition display program 118)

The lifetime balance transition display program 118 is configured to convert the lifetime income transition data created by the household income

また、生涯収支推移表示プログラム118は、生涯収入推移データから生涯支出推移のデータを差し引いた余剰資金(自由使途資金)推移を、例えば年次ごとの損益グラフで、又は年次ごとに積算したグラフで可視化表示するように構成されている。更に、生涯収支推移表示プログラム118は、生涯収入推移データ及び生涯支出推移のデータから、生涯収支のバランスシートの画面データを生成し可視化表示するように構成されている。 In addition, the lifetime balance change display program 118 is a graph in which the surplus funds (free-use funds) change obtained by subtracting the data on the change in lifetime expenditure from the lifetime income change data, for example, in the profit / loss graph for each year or accumulated for each year. It is configured to display with visualization. Further, the lifetime balance transition display program 118 is configured to generate and display the screen data of the balance sheet of the lifetime balance from the lifetime income transition data and the lifetime expenditure transition data.

図5(a)は、生涯収支推移表示プログラム118により表示部13に表示される生涯支出推移の一例を示す図である。生涯収支推移表示プログラム118は、同図に示すように、生成したこれらグラフの画面を一同に表示部13に表示することができるように構成されている。

FIG. 5A is a diagram illustrating an example of a lifetime expenditure transition displayed on the

また、図5(b)は、教育費の推移の一例を示す図である。生涯収支推移表示プログラム118は、図5(b)に示されるように、例えば教育費のみの推移を個別に取り出して子供ごとに比率を色分けした棒グラフの画面に変換して表示部13に表示できるように構成されている。なお、図示はしないが、基本生活費用や税金のみの推移を個別に表示できるようにも構成されている。

FIG. 5B is a diagram illustrating an example of the transition of educational expenses. As shown in FIG. 5 (b), the lifetime balance transition display program 118 can convert a transition of only educational expenses into a bar graph screen in which the ratio is color-coded for each child and can be displayed on the

図6は、生涯収入推移、生涯支出推移及び余剰資金(自由使途資金)推移を一同に表示した例を示す図である。このように、利用者は、生涯にわたる収入と収支の推移を比較しながら世帯の資金収支(キャッシュフロー)の全体像を容易に把握することができる。 FIG. 6 is a diagram illustrating an example in which a change in lifetime income, a change in lifetime expenditure, and a change in surplus funds (free-use funds) are displayed together. In this way, the user can easily grasp the overall picture of the household's cash balance (cash flow) while comparing changes in income and balance over the lifetime.

更に、生涯収支推移表示プログラム118は、次に詳細に説明する住宅費用解析プログラム122と連携し、住宅ローン設定条件入力表の画面を介して利用者が選択したローン種別(返済プラン)により試算される毎年の返済額や、借り換え返済、又は繰り上げ返済をした場合の返済額を瞬時に前記生涯支出推移及び余剰資金推移の表示に反映させるように構成されている。これにより、利用者は、自己の家計の事情や生活プランに適合する最も合理的又は低リスクの返済方法は何かを表示部13の画面を見ながら容易に比較検討することができることとなる。

Further, the lifetime balance transition display program 118 is calculated according to the loan type (repayment plan) selected by the user through the screen of the mortgage setting condition input table in cooperation with the housing

(住宅費用解析プログラム120)

次に、住宅費用解析プログラム120について説明する。生活設計支援プログラム100のメイン選択メニュー画面において住宅費用解析が選択されると、住宅費用解析プログラム120が起動されるように構成されている。

(Housing Cost Analysis Program 120)

Next, the housing

住宅費用解析プログラム120は、図2に示すように、サブプログラムとして住宅関連情報設定プログラム121と、ローン返済額シミュレーションプログラム122と、借換返済シミュレーションプログラム123と、繰上返済シミュレーションプログラム124とを備えている。

As shown in FIG. 2, the housing

(住宅関連情報設定プログラム121)

図7は、表示部13に表示される住宅関連費用入力表の画面の一例を示す図である。住宅費用解析プログラム120が起動すると、初めに住宅関連情報設定プログラム121が起動され、最初のステップとして図7(a)に示されるような住宅関連費用入力表の画面が表示部13に表示されるように構成されている。

(Housing Related Information Setting Program 121)

FIG. 7 is a diagram illustrating an example of a screen of a house related cost input table displayed on the

図7(a)において、「試算開始年」の欄には、現在の西暦年が自動的に表示されるように構成されている。また、数年後にローンを組みたい利用者であれば、入力部14を操作して当該欄に任意の西暦年を入力することにより試算開始年を指定できるようにも構成されている。

In FIG. 7A, the “year of trial calculation” column is configured to automatically display the current year. In addition, it is configured so that a user who wants to make a loan several years later can specify a trial calculation start year by operating the

「住宅ローン借入額」、「融資実行年」及び「住宅ローン利用年数」の各欄には、利用者が既にローン契約した、又は契約予定の値が入力部14を介して入力できるように構成されている。

In each column of “Mortgage Borrowing Amount”, “Loan Execution Year”, and “Home Loan Usage Year”, the user has already entered a loan contract or a contract planned value can be input via the

また、その他の試算条件である「物件価格」、「諸費用価格(頭金)」、「管理費」、「修繕積立費」等の各欄には、前述の生涯資金収支解析において利用者が既に入力した情報が入力データ180から読み出されて当該欄に自動的に表示されるように構成されている。なお、空欄には利用者による追加入力が可能とされている。

In addition, other columns such as “Property price”, “Expense price (down payment)”, “Administrative expenses”, “Repair reserve expenses”, etc. The input information is read from the

住宅関連情報設定プログラム121は、次のステップで図7(b)に示されるような住宅ローン設定条件入力表の画面を表示部13に表示するように構成されている。

The house related

同図に示される「住宅ローン利用年数」には、既に入力された年数が自動的に表示され、また「第1順位ローン金額」には、既に入力された住宅ローン借入額が自動的に表示されるように構成されている。 The number of years already entered is automatically displayed in the “Year of Mortgage Usage” shown in the figure, and the amount of borrowing already entered is automatically displayed in “First Loan Amount”. It is configured to be.

また、「ローン種別」の欄では、当該欄にカーソルを合わせることにより表示されるポップアップリストの一覧のなかから「変動金利」、「3年固定金利」、「5年固定金利」、「10年固定金利」、「フラット35(35年間金利が固定される実質的に固定金利の返済プラン)」又は「ステップ金利(第一次返済期間と第二次返済期間で金利設定条件が異なる、いわゆる「ゆとり返済」)」のいずれかの返済プランが選択されるように構成されている。 In the “Loan Type” column, “Floating Interest Rate”, “3-Year Fixed Interest Rate”, “5-Year Fixed Interest Rate”, “10-Year” from the pop-up list displayed by placing the cursor in the relevant column. "Fixed interest rate", "Flat 35 (substantially fixed interest rate repayment plan with fixed interest rate for 35 years)" or "Step interest rate (the interest rate setting conditions differ between the primary and secondary repayment periods, so-called" One of the repayment plans of "clearance repayment")) "is selected.

なお、固定金利期間が終了後、更に固定金利特約(3年、5年、10年)の再設定も可能に構成されている。 In addition, after the fixed interest rate period ends, it is possible to reset the fixed interest rate special contract (3 years, 5 years, 10 years).

「第2順位ローン金額」の欄に金額が入力されると、既に入力された住宅ローン借入額(総額)を合計で満たす金額が「第1順位ローン金額」の欄に自動的に表示されるように構成されている。すなわち、第1順位ローン金額と第2順位ローン金額それぞれの借入額について2種類の返済プランを同時に組み合わせた、ペアローン(ミックスローン)の場合におけるシミュレーション解析ができるように構成されている。 When an amount is entered in the “second-order loan amount” field, the amount that satisfies the total mortgage borrowing amount (total) already entered is automatically displayed in the “first-order loan amount” field. It is configured as follows. That is, it is configured to be able to perform a simulation analysis in the case of a pair loan (mixed loan) in which two types of repayment plans are simultaneously combined for the borrowing amounts of the first rank loan amount and the second rank loan amount.

「ローン種別」の欄で「ステップ金利」が選択された場合には、「優遇金利幅(第一次返済期間の金利)」、「優遇金利適用期間(第一次返済期間年数)」及び「当初優遇期間終了後金利(第二次返済期間の金利)」の各欄に当該値がデフォルトで表示される。利用者は、例えば「優遇金利幅」や「優遇金利適用期間」の欄で所望の金利や期間を指定することができ、その入力に応じて「当初優遇期間終了後金利」の値が自動的に計算されて当該欄に表示されるように構成されている。これにより、利用者は、優遇金利適用期間経過後の金利を瞬時に知ることができる。 When “Step interest rate” is selected in the “Loan type” column, “Preferential interest rate range (interest rate for primary repayment period)”, “Preferential interest rate application period (number of years for primary repayment period)” and “ The value is displayed by default in each column of “Interest rate after initial preferential period (interest rate for second repayment period)”. For example, the user can specify the desired interest rate and period in the “Preferential interest rate range” and “Preferential interest rate application period” fields, and the value of “Interest rate after initial preferential period” is automatically set according to the input. Is calculated and displayed in the corresponding field. As a result, the user can instantly know the interest rate after the preferential interest rate application period has elapsed.

図8は、表示部13に表示される金利設定条件入力表の画面の一例を示す図である。住宅関連情報設定プログラム121は、利用者の任意選択的な入力事項として、図8に示される金利設定条件入力表の画面を介して、金利条件を任意に設定できるように構成されている。すなわち、各ローン種別の横の欄に、融資実行年当初の金利が入力されるとともに、利用者がその後の金利変化の予測を上昇率又は下降率で入力可能とされている。これにより、専門家の予測だけでなく、利用者の主観による楽観的又は悲観的な金利予測に基づく返済額のシミュレーションを可能としている。

FIG. 8 is a diagram illustrating an example of a screen of the interest rate setting condition input table displayed on the

なお、この住宅関連費用入力表に入力された各情報は、入力データ180として一旦、外部記憶部12に記憶される。また、利用者は、入力表に入力した情報を任意の値に変更するだけで、それぞれ異なる条件下でのシミュレーション結果を容易に比較検討することも可能とされている。

Note that each piece of information input to the housing-related cost input table is temporarily stored in the

(ローン返済額シミュレーションプログラム122)

住宅費用解析プログラム120は、少なくとも「住宅ローン借入額」、「融資実行年」、「住宅ローン利用年数」及び「ローン種別」の情報が入力されたと判断すると、ローン返済額シミュレーションプログラム122を起動するよう構成されている。ローン返済額シミュレーションプログラム122は、これらの情報に基づいて利息を年次複利で計算した場合の返済額を算出し、図7(b)に示した住宅ローン設定条件入力表の画面の返済総額の欄にその金額を表示するよう構成されている。

(Loan Repayment Amount Simulation Program 122)

The housing

外部記憶部12の参照データ190には、長期金利や国債金利等の経済指標の専門家の見通しに基づいて予測される最新の住宅ローン金利が記憶されている。返済総額の試算にあたって「変動金利」が選択された場合には、参照データ190から読み出されるこの最新の住宅ローン金利の予測値が用いられる。また、利用者の主観的な予測に基づく金利が入力データ180に入力されている場合には、この入力データ180から読み出される住宅ローン金利が返済総額の試算に用いられる。

The

また、ローン返済額シミュレーションプログラム122は、ローン種別として「3年固定金利」、「5年固定金利」又は「10年固定金利」のいずれかが選択された場合には、選択された固定金利期間において所定の固定金利の条件で試算される返済額と、残余のローン返済期間において選択された固定金利期間経過後に予測される金利条件で試算される返済額とを加算した額を返済総額として算出し表示するように構成されている。そして、試算した各返済額に基づいて、年次ごと毎月のローン返済額の推移を返済グラフにより可視化するように構成されている。

The loan repayment

また、ローン返済額シミュレーションプログラム122は、ローン種別として「ステップ金利」が選択された場合には、優遇金利適用期間において選択された優遇金利の条件で試算される返済額と、残余のローン返済期間において当初優遇期間終了後金利の条件で試算される返済額とを加算した額を返済総額として算出し表示するように構成されている。そして、試算した各返済額に基づいて、年次ごと毎月のローン返済額の推移を返済グラフにより可視化するように構成されている。

Further, the loan repayment

(借換返済シミュレーションプログラム123)

図9は、住宅ローンの借り換えを解析する際の住宅ローン設定条件入力表の画面の一例を示す図である。ローン返済額シミュレーションプログラム122は、住宅ローン設定条件入力表の画面において、同図の破線による円内に示す「借換 年次指定」、「借換 種別指定」、「借換 優遇金利」に情報が入力されたと判断すると、借換返済シミュレーションプログラム123を起動するように構成されている。

(Refinancing simulation program 123)

FIG. 9 is a diagram illustrating an example of a screen of a mortgage setting condition input table when analyzing mortgage refinancing. The loan repayment

借換返済シミュレーションプログラム123は、指定された借換年次までの期間において当初の条件で試算される返済額と、借換年次からローン返済期間満了(完済)年までの期間において借り換えにより変更された条件で試算される返済額とを加算した額を返済総額として算出し表示するように構成されている。そして、試算した各返済額に基づいて、年次ごと毎月のローン返済額の推移を返済グラフにより可視化するように構成されている。

The

例えば利用者が変動金利で住宅ローンを契約している場合において、当初予想していたよりも金利が上昇した場合に、どの時期にどのような返済プランに借り換えたらより少ない返済額で済むかを判断することは難しい。本実施の形態によれば、将来における様々な変動金利のパターンを想定して、借り換え時期と返済プランごとに試算される返済総額を相互に比較できるので、社会的な経済環境の変化に対応し、また支出のピーク時期を回避するような最適な借り換え条件を事前に利用者に提示することができる。 For example, when a user has a mortgage contract with a variable interest rate, if the interest rate rises higher than originally expected, the repayment plan will be reconciled with a lower repayment amount when refinancing. Difficult to do. According to this embodiment, assuming various variable interest rate patterns in the future, the amount of repayment and the total repayment estimated for each repayment plan can be compared with each other. In addition, optimal refinancing conditions that avoid the peak time of expenditure can be presented to the user in advance.

(繰上返済シミュレーションプログラム124)

図10は、住宅ローンの繰り上げ返済を解析する際の住宅ローン設定条件入力表の画面の一例を示す図である。ローン返済額シミュレーションプログラム122は、住宅ローン設定条件入力表の画面において、同図の破線による円内に示されるように利用者が繰り上げ返済をしようとする年次を指定し、繰り上げ返済額を入力したのを受けて、繰上返済シミュレーションプログラム124を起動するように構成されている。

(Progress repayment simulation program 124)

FIG. 10 is a diagram illustrating an example of a screen of a mortgage setting condition input table when analyzing prepayment of a mortgage. The loan repayment

繰上返済シミュレーションプログラム124は、指定された繰上返済年次までの期間において当初の契約で定めた返済条件で試算される返済額と、入力された繰り上げ返済額と、繰り上げ返済をした年次以降、減額した借入額に基づいてローン返済期間満了(完済)年までの期間において契約で定めた返済条件で試算される返済額とを加算した額を返済総額として算出し、住宅ローン設定条件入力表の画面に表示するように構成されている。

The advance

図11(a)は、繰り上げ返済前の返済グラフの画面の例であり、図11(b)は、繰り上げ返済後の返済グラフの画面の例である。このように繰上返済シミュレーションプログラム124は、試算した各返済額に基づいて、年次ごと毎月のローン返済額の推移を返済グラフにより可視化するように構成されている。これにより、利用者は、繰り上げ返済による効果を瞬時にかつ容易に知ることができる。

FIG. 11A is an example of a repayment graph screen before the advance repayment, and FIG. 11B is an example of a repayment graph screen after the advance repayment. In this way, the advance

また、ローン返済額シミュレーションプログラム122は、前述の生涯収支推移表示プログラム118と連携し、ローン返済額の推移の試算結果を生涯支出推移及び余剰資金(自由使途資金)推移の結果に反映させるとともに、返済グラフを生涯支出推移グラフ、バランスシート及び余剰資金推移等と一同に又は重ね合わせて表示できるように構成されている。

In addition, the loan repayment

これにより、利用者は、基本支出、教育費及び保険料等を総合した支出のピークを回避するような無理のない住宅ローンの借り換え方法、又は例えば給与収入のある生産年齢内に住宅ローンを完済させるような繰り上げ返済方法等について、金利や物価の上昇等の将来の社会的な経済環境の変動要因を考慮した上での最も低リスクで、かつ合理的な判断をすることができるようになる。 As a result, users can repay mortgage loans within the production age with salary income, for example, by using a reasonable mortgage refinancing method that avoids the peak of spending including basic spending, education expenses and insurance premiums. It is possible to make a reasonable judgment on the advanced repayment method, etc., with the lowest risk, taking into consideration the fluctuation factors of the future social economic environment such as the rise in interest rates and prices. .

また、住宅ローンの借り換えや繰り上げ返済による利息軽減効果と、他の金融資産配分による利増分を最新の経済指標に基づき比較できるので、双方の投資習性を鑑みた老後資金計画も簡便に検討することもできる。 In addition, since the interest reduction effect by refinancing and prepayment of mortgages can be compared with the increase in interest from other financial asset allocation based on the latest economic indicators, retirement funding plans that take into account the investment habits of both parties should be considered easily. You can also.

(本実施の形態の効果)

したがって、本実施の形態の生活設計支援システム1によれば、将来予測される世帯のキャッシュフローを可視化することにより、主として住宅ローンの借り換え、借り入れ又は返済の方法等の選択について、将来における利用者の個人的な経済状況及び社会的な経済環境の変動要因を勘案しながら、世帯主の経済事情や求めるライフプランに応じた最も合理的な判断材料を提供することができる。また、生活設計に基づく必要保障額の算出により、最適な保険設計が容易にでき、保険募集上、保険見直しのニーズに応えられる。

(Effect of this embodiment)

Therefore, according to the lifestyle

本発明は、上記実施の形態に限定されず、本発明の要旨を変更しない範囲内で種々変形実施が可能である。例えば、各手段を制御部11のCPUとプログラム100〜124によって実現したが、ASIC(Application Specific IC)等のハードウエアによって実現してもよい。

The present invention is not limited to the above-described embodiment, and various modifications can be made without departing from the scope of the present invention. For example, each means is realized by the CPU of the

また、プログラム100〜124は、CD−ROM等の記録媒体から外部記憶部12内に取り込んでもよく、サーバ装置等からネットワークを介して外部記憶部12内に取り込んでもよい。

The

また、試算された収入推移、支出推移及び返済額の推移に基づいて、住宅ローンの借り換え、借り入れ、又は繰上げ返済による貯蓄残高が減少する期間と自由使途資金を算出し、自由使途資金に対応した必要保障額(遺族生活資金)を算出し、保険設計時または保険募集の提案時に、貯蓄残高が減少する期間と必要保障額を提示してもよい。これにより、必要保障額の見直しや、今後発生し得る疾病リスクの見直しの際の有効な判断材料が得られる。 In addition, based on the estimated income trend, expenditure trend, and repayment trend, the amount of savings due to mortgage refinancing, borrowing, or advanced repayment and the amount of free-use funds were calculated to deal with free-use funds. You may calculate the required amount of security (survivor's living fund) and present the period during which the savings balance will decrease and the required amount of security at the time of insurance design or insurance offer proposal. As a result, it is possible to obtain an effective judgment material when reviewing the required security amount and reviewing the disease risk that may occur in the future.

1…生活設計支援システム、11…制御部、12…外部記憶部、13…表示部、14…入力部、100…生活設計支援プログラム、101…メイン制御プログラム、102…表示制御プログラム、103…入力制御プログラム、110…生涯資金収支解析プログラム、111…利用者情報設定プログラム、112…世帯収入推移試算プログラム、113…世帯支出推移試算プログラム、114…基本生活費シミュレーションプログラム、115…教育費シミュレーションプログラム、116…年金保険料シミュレーションプログラム、117…税金シミュレーションプログラム、118…生涯収支推移表示プログラム、

120…住宅費用解析プログラム、121…住宅関連情報設定プログラム、122…ローン返済額シミュレーションプログラム、123…借換返済シミュレーションプログラム、124…繰上返済シミュレーションプログラム、180…入力データ、190…参照データ、

DESCRIPTION OF

120 ... Housing cost analysis program, 121 ... Housing related information setting program, 122 ... Loan repayment amount simulation program, 123 ... Refinancing repayment simulation program, 124 ... Advance repayment simulation program, 180 ... Input data, 190 ... Reference data,

Claims (1)

記憶手段に記憶されている利用者に関する情報のうち時期とともに入力された世帯収入に関する情報に基づいて当該利用者の収入の推移を試算する収入推移試算手段と、

前記記憶手段に記憶されている経済指標に基づく予測情報のうち住宅ローン金利の予測情報、及び利用者が選択する住宅ローンの借り換え時期と借り換え後のローン種別を含む住宅ローンの返済条件に基づいて当該利用者の住宅ローン返済額を試算する住宅ローン返済額試算手段と、

前記記憶手段に記憶されている前記利用者に関する情報のうち時期とともに入力された世帯支出に関する情報、前記予測情報及び前記住宅ローン返済額試算手段が試算する前記住宅ローン返済額に基づいて当該利用者の支出の推移を試算する支出推移試算手段と、

前記収入推移試算手段が試算する収入推移、前記支出推移試算手段が試算する支出推移及び前記住宅ローン返済額試算手段が試算する返済額の推移を年次毎に日本人の平均寿命まで一同に表示部に表示する生涯収支推移表示手段として機能させるための生活設計支援プログラムであって、

前記住宅ローン返済額試算手段は、変動金利、所定年の固定金等のローン種別を含む前記住宅ローンの返済条件の入力を受け付ける住宅ローン設定条件入力表画面を前記表示部に表示し、入力された前記住宅ローンの返済条件に基づいて試算した住宅ローンの返済総額を前記住宅ローン設定条件入力表画面に表示し、入力された前記住宅ローンの返済条件に基づいて試算した年次毎の毎月の住宅ローン返済額の返済グラフによる推移を前記表示部に表示し、

前記コンピュータを、

前記収入推移試算手段が試算する収入推移、前記支出推移試算手段が試算する支出推移及び前記住宅ローン返済額試算手段が試算する返済額の推移に基づいて、住宅ローンの借り換え、借り入れ、又は繰上げ返済による貯蓄残高が減少する時期と自由使途資金を算出し、自由使途資金に対応した必要保障額を算出する必要保障額算出手段と、

保険設計時または保険募集の提案時に、前記貯蓄残高が減少する期間と前記必要保障額を提示するリスク提示手段としてさらに機能させるための生活設計支援プログラム。 Computer

Revenue transition estimation means for calculating transition of the income of the user based on information on household income input with the time out of the information on the user stored in the storage means;

Based on the prediction information of the mortgage interest rate among the prediction information based on the economic index stored in the storage means, and the mortgage repayment condition including the mortgage refinancing time selected by the user and the loan type after refinancing A mortgage repayment amount calculation means for calculating the mortgage repayment amount of the user;

Of the information on the user stored in the storage means, information on household expenditure input with time, the prediction information, and the mortgage repayment amount calculated by the mortgage repayment amount calculation means, the user Expenditure trend calculation means to estimate the trend of expenditure,

The revenue transition estimated by the income transition estimation means, the expenditure transition estimated by the expenditure transition estimation means, and the repayment amount estimated by the mortgage repayment amount estimation means are displayed all together until the average life span of the Japanese for each year. A life design support program for functioning as a lifetime balance display means to be displayed in the department,

The mortgage repayment amount calculation means displays a mortgage setting condition input table screen for accepting input of the mortgage repayment conditions including a variable interest rate, a loan type such as a fixed amount for a predetermined year on the display unit, and is input said the repayment total amount of housing loans was estimated on the basis of the repayment terms of the mortgage and displayed on the mortgage setting condition input table screen, the annual each of which has been estimated on the basis of the repayment terms of the input the mortgage Display the transition of the monthly mortgage repayment amount by the repayment graph on the display section ,

The computer,

Refinancing, borrowing, or prepayment of a mortgage based on the revenue transition estimated by the revenue transition estimation means, the expenditure transition estimated by the expenditure transition estimation means, and the repayment amount estimated by the mortgage repayment amount estimation means A required security amount calculation means for calculating a period when the savings balance due to and a free-use funds are calculated, and calculating a required security amount corresponding to the free-use funds,

At the time of proposal of insurance design time or insurance recruitment, living design support program for further function as a risk presenting means for presenting the required guarantee amount and the period in which the savings balance is reduced.

Priority Applications (1)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| JP2010075551A JP5592683B2 (en) | 2010-03-29 | 2010-03-29 | Life design support program |

Applications Claiming Priority (1)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| JP2010075551A JP5592683B2 (en) | 2010-03-29 | 2010-03-29 | Life design support program |

Publications (3)

| Publication Number | Publication Date |

|---|---|

| JP2011209890A JP2011209890A (en) | 2011-10-20 |

| JP2011209890A5 JP2011209890A5 (en) | 2013-05-23 |

| JP5592683B2 true JP5592683B2 (en) | 2014-09-17 |

Family

ID=44940902

Family Applications (1)

| Application Number | Title | Priority Date | Filing Date |

|---|---|---|---|

| JP2010075551A Active JP5592683B2 (en) | 2010-03-29 | 2010-03-29 | Life design support program |

Country Status (1)

| Country | Link |

|---|---|

| JP (1) | JP5592683B2 (en) |

Families Citing this family (5)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| JP6204077B2 (en) * | 2013-06-12 | 2017-09-27 | 小澤 隆 | Simulation system and server |

| JP6300866B2 (en) * | 2016-08-19 | 2018-03-28 | ヤフー株式会社 | Information presentation apparatus, presentation method, and presentation program |

| JP2018169898A (en) * | 2017-03-30 | 2018-11-01 | Hrソリューションズ株式会社 | Information providing device, information providing method, program, and information providing system |

| JP7146966B2 (en) * | 2021-01-25 | 2022-10-04 | プルデンシャル生命保険株式会社 | Information processing device, program, and information processing method |

| JP7458121B1 (en) | 2023-11-06 | 2024-03-29 | Jolly Factory株式会社 | Loan refinancing support system |

Family Cites Families (7)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| JPH08314892A (en) * | 1995-05-18 | 1996-11-29 | Hitachi Ltd | Rate of interest predicting system applying neural net to econometric model |

| JPH1125155A (en) * | 1997-06-27 | 1999-01-29 | Jiyasutei:Kk | Life planning system and storage medium |

| JP2001222585A (en) * | 2000-02-08 | 2001-08-17 | Sony Corp | Server device, method and system for consulting service for financial product and terminal device for the system |

| JP2002230033A (en) * | 2001-01-31 | 2002-08-16 | Daikoro Kk | Commemorative bulletin |

| JP2003288486A (en) * | 2002-03-28 | 2003-10-10 | Casio Comput Co Ltd | Graph display device |

| JP4901153B2 (en) * | 2005-08-02 | 2012-03-21 | 旭化成ホームズ株式会社 | Lifetime financial asset estimation device |

| JP5223088B2 (en) * | 2007-06-29 | 2013-06-26 | 株式会社日立ソリューションズ | Stock price analysis system and program |

-

2010

- 2010-03-29 JP JP2010075551A patent/JP5592683B2/en active Active

Also Published As

| Publication number | Publication date |

|---|---|

| JP2011209890A (en) | 2011-10-20 |

Similar Documents

| Publication | Publication Date | Title |

|---|---|---|

| JP6348545B2 (en) | Computer-implemented method and apparatus for building and executing dynamic equity financial products | |

| Mun | Real options analysis course: business cases and software applications | |

| JP6354059B2 (en) | Financial information analysis system and program | |

| US20130339219A1 (en) | Interactive Finance And Asset Management System | |

| US20190213766A1 (en) | Method and system for computer assisted valuation modeling | |

| US20110218934A1 (en) | System and methods for comparing real properties for purchase and for generating heat maps to aid in identifying price anomalies of such real properties | |

| US8473392B1 (en) | System and method for evaluation and comparison of variable annuity products | |

| Gan et al. | Efficient greek calculation of variable annuity portfolios for dynamic hedging: A two-level metamodeling approach | |

| Strickland | The financialisation of urban development: Tax Increment Financing in Newcastle upon Tyne | |

| Sauer | Educational financing and lifetime earnings | |

| JP5592683B2 (en) | Life design support program | |

| JP2007011990A (en) | Business portfolio simulation system | |

| Pfnür et al. | Modelling uncertain operational cash flows of real estate investments using simulations of stochastic processes | |

| Espinoza et al. | DNPV: a valuation methodology for infrastructure and Capital investments consistent with prospect theory | |

| Ghent | Infrequent housing adjustment, limited participation, and monetary policy | |

| JP2014093041A (en) | Inheritance management program and inheritance management system | |

| Leonardo et al. | Formalization of a new stock trend prediction methodology based on the sector price book value for the Colombian market | |

| Lee et al. | Valuation of reverse mortgages with surrender: A utility approach | |

| JP2001350893A (en) | Method and system for management accounting under consideration of time value and program recording medium | |

| JP2004295492A (en) | Life planning device and method, computer program, program storage medium | |

| KR20120070136A (en) | System, method, and media on providing financial planning simumation information | |

| Lindner et al. | Borrowing constraints, own labour and homeownership | |

| JP2021502653A (en) | Systems and methods for automated preparation of visible representations regarding the achievability of goals | |

| JP2019074979A (en) | Information processor, program and information processing method | |

| Moro-Visconti et al. | E-Health and Telemedicine Startup Valuation |

Legal Events

| Date | Code | Title | Description |

|---|---|---|---|

| A521 | Request for written amendment filed |

Free format text: JAPANESE INTERMEDIATE CODE: A523 Effective date: 20130322 |

|

| A621 | Written request for application examination |

Free format text: JAPANESE INTERMEDIATE CODE: A621 Effective date: 20130322 |

|

| A711 | Notification of change in applicant |

Free format text: JAPANESE INTERMEDIATE CODE: A711 Effective date: 20130322 |

|

| A521 | Request for written amendment filed |

Free format text: JAPANESE INTERMEDIATE CODE: A821 Effective date: 20130325 |

|

| A131 | Notification of reasons for refusal |

Free format text: JAPANESE INTERMEDIATE CODE: A131 Effective date: 20131217 |

|

| A521 | Request for written amendment filed |

Free format text: JAPANESE INTERMEDIATE CODE: A523 Effective date: 20140217 |

|

| A02 | Decision of refusal |

Free format text: JAPANESE INTERMEDIATE CODE: A02 Effective date: 20140311 |

|

| A521 | Request for written amendment filed |

Free format text: JAPANESE INTERMEDIATE CODE: A523 Effective date: 20140610 |

|

| A911 | Transfer to examiner for re-examination before appeal (zenchi) |

Free format text: JAPANESE INTERMEDIATE CODE: A911 Effective date: 20140618 |

|

| TRDD | Decision of grant or rejection written | ||

| A01 | Written decision to grant a patent or to grant a registration (utility model) |

Free format text: JAPANESE INTERMEDIATE CODE: A01 Effective date: 20140708 |

|

| A61 | First payment of annual fees (during grant procedure) |

Free format text: JAPANESE INTERMEDIATE CODE: A61 Effective date: 20140801 |

|

| R150 | Certificate of patent or registration of utility model |

Ref document number: 5592683 Country of ref document: JP Free format text: JAPANESE INTERMEDIATE CODE: R150 |

|

| R250 | Receipt of annual fees |

Free format text: JAPANESE INTERMEDIATE CODE: R250 |