JP4583708B2 - Motivation and commission distribution system for non-cash transactions - Google Patents

Motivation and commission distribution system for non-cash transactions Download PDFInfo

- Publication number

- JP4583708B2 JP4583708B2 JP2002514622A JP2002514622A JP4583708B2 JP 4583708 B2 JP4583708 B2 JP 4583708B2 JP 2002514622 A JP2002514622 A JP 2002514622A JP 2002514622 A JP2002514622 A JP 2002514622A JP 4583708 B2 JP4583708 B2 JP 4583708B2

- Authority

- JP

- Japan

- Prior art keywords

- commission

- purchase

- computer

- amount

- card

- Prior art date

- Legal status (The legal status is an assumption and is not a legal conclusion. Google has not performed a legal analysis and makes no representation as to the accuracy of the status listed.)

- Expired - Lifetime

Links

Images

Classifications

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q30/00—Commerce

Description

【0001】

【発明の属する技術分野】

本発明は、購入取引の管理及び非現金式拠点販売取引システムの販売者と利用者の間で購入コミッションの分配を行う非現金式拠点販売取引システムに関するものである。

【0002】

【従来の技術】

デビットカードやクレジットカードのような非現金式支払装置は、商品やサービスの購入者に多大な便宜を与える。しかし、そのような支払装置は、電子取引管理・会計システムを要し、そのような装置で購入された商品やサービスのコストに加えて運営費が発生する。伝統的に、非現金式支払装置の発行者は販売契約を結び、非現金式支払装置を利用できる便宜を消費者に提供できることと引き換えに参加している販売者がカード発行者にコミッションを支払うようになっている。最近では、カード発行者間の競争が販売者が支払うコミッションのレートを下げている。結果として、カード発行者は消費者に対して多種多様な動機付けを与えそのような動機付けを積極的にコマーシャルをかけて宣伝することによって、取引量を増やすことを試みてきた。

【0003】

McCarthyの米国特許第4、941、090号に開示されているような公知の動機付けプログラムでは、顧客に非現金式支払装置による個人の購入額に基づいてパーソナルボーナスが支払われるようになっている。また、そのような動機付けプログラムは個々の顧客にとって魅力的であるが、広告をしたり見込み客を引き付けるために有効的に宣伝されなければならない。さらに、これらの動機付けプログラムは参加している販売者に対してはなんら利益も与えず、しかし販売者はそれでもなお他の非現金式支払システムと競争的なコミッションに基づいて登録されていなければならない。従って、消費者に他の非現金式支払装置よりも優先して利用する動機付けを提供し、また販売者に入会奨励を付与し、カード保持者を引き付けて維持することに関する宣伝コストの削減を可能にする非現金式支払いシステムを開発させることが望ましい。

この出願の発明に関連する先行技術文献情報としては、以下のものがある(国際出願日以降国際段階で引用された文献及び他国に国内移行した際に引用された文献を含む)。

【特許文献1】

米国特許第号4,594,663明細書

【特許文献2】

米国特許第号4,750,119明細書

【特許文献3】

米国特許第号4,491,090明細書

【特許文献4】

米国特許第号5,025,372明細書

【特許文献5】

米国特許第号5,117,355明細書

【特許文献6】

米国特許第号5,222,018明細書

【特許文献7】

米国特許第号5,287,268明細書

【特許文献8】

米国特許第号5,537,314明細書

【特許文献9】

米国特許第号5,826,241明細書

【特許文献10】

米国特許第号6,105,001明細書

【特許文献11】

米国特許第号5,581,041明細書

【非特許文献1】

P.A.Pays,"An intermediated and payment system technology" Computer Networks & ISDN Systems 28 (1996)pp.1197−1206

【非特許文献2】

T.Baron"Banks, vendors focus on security"cited in "Abstracts of Recent Articles and Literature" By Helen Collinson in form Computers & Security 14(1995)pp.409−414

【非特許文献3】

Amway USA "The Amway Opportunity in the USA−questions & answers"from http www.amway−usa.com/info/q&a.asp,(1998)

【非特許文献4】

6 sheets comprising article which disclose incentive rebates liking to the use of GM credit card. (From Dialog Search including publishing dates, title, source of the article & related paragraph,fr.(1985)

【非特許文献5】

J.Corry,"The Amway way: Seeking the profit of many" The American Spectator;Bloomington;Vol.31,Issue 10;(1998) pp.1−2

【非特許文献6】

M.Rock,"This article could make you a millinonaire"from Institute of Directors, London;Vol.48, Issue 7(1995),pp.1−4

【0004】

【発明が解決しようとする課題】

本発明によれば、コミッション支払・会計システムは、デビットカードやクレジットカードのような非現金式支払装置の保持者に属する取引データを階層データベースに組織し、デビットカードの利用や新規カード会員の加入のための動機付けプログラムの組織的構造を反映させる。購入のコミッションは電子的にカード発行者に転送され、前記コミッション支払・会計システムは、保存された電子資金取引データ、カードホールダーの間の組織内での関係、比例したコミッションレートを組織関係と関連付けてなる所定の表に基づいてカードホールダーに対するコミッション支払額を決定し分配するように構成されている。

【0005】

【発明の実施の形態】

図1を参照すると、本発明による非現金式支払・コミッションシステムの例が示されている。このシステムは、ネットワークマーケティングまたはマルチレベルマーケティング組織の会員(例えば人間またはディストリビュータ)による商品やサービス購入の管理と、階層コミッション決済・支払い方法による前記組織会員へのコミッション支払の管理とを行うようになっている。更に以下に説明されるように、各会員はデビットまたはクレジットカードを与えられ多数の販売者拠点のうちどこでも買い物ができるものであり、販売拠点10はその一例を示すものである。前記デビットまたはクレジットカードはその表面上に会員の情報をエンコードするための手段、例えば磁気ストライプに会員の口座番号が磁気的にエンコードするようなもの、を有している。前記ネットワークマーケティング組織の事前取り決めにより、各販売者拠点の経営者はそのような商品やサービスの購入価格の一定率もしくは購入毎の一定額を、前記会員による商品やサービスの購入に対するディスカウントとして提供することに同意する。さらに、前記ディスカウント及びさらなるディスカウントを考慮することとの引き換えに、前記販売者には例えばダイレクトメールといった方法により前記組織の会員に自分たちの商品やサービスを売り込む機会が提供される。

【0006】

拠点販売取引処理端末12(PPT)が拠点10に設置されている。この拠点は小売店サイトや、または電話で注文を受けるカタログ販売のオペレーターや、またはネットワークを通して商品を販売するために用いられるコンピュータサイトを有することが可能である。前記購入処理端末12は、購入に関するデータを獲得するためのキーボード12aや磁気ストライプ読取器12bのようなデータ入力手段、購入データを一時的に保存するデジタルメモリー(図示せず)、購入データを通信して購入に対するカード承認信号を受信するモデム12cのような電子通信インターフェースを有している一般的なもので良い。

【0007】

会員が拠点10で買い物をしたい場合、前記会員はデビットカードを提示し、会員の口座番号を前記磁気ストライプ読取器12b経由で前記購入処理端末12のメモリーに入力する。前記購入金額は前記キーボード12aを経由して前記拠点販売システム端末に入力される。ついで、前記端末12が作動し、電子通信インターフェース12cを起動して、デビット承認・取引処理器14との電子データ接続13を確立する。前記通信インターフェース12cがモデムを有する場合の実施例においては、前記データ接続器14は電話回線による接続であってもよい。その他の実施例においては、電子データ送信の別の一般的な方法が採用され前記データ接続13を確立する。

【0008】

前記購入処理端末12が作動して、前記会員口座番号と、購入金額と、販売者IDとを含む購入データを前記承認・取引処理器14へ送信する。前記処理器14は各販売拠点と関連付けられている遠隔位置に置かれることが望ましく、更に各販売拠点と電子データ接続を確立するように構成されている。前記処理器14は作動して購入データを受信し、各購入について、受信された購入データに対する承認信号を送るかどうか決定する。このような決定は、例えば、前記処理器14によって維持されたリスクデータに基づいて成され、各会員に関連して前記購入額の不履行のリスクが容認可能に低いかを判断する。これとは別の方法として、前記承認処理器は、会員のデビット口座の残高へのアクセスすることによってこのような決定を行っても良い。

【0009】

前記提示された購入が承認されると、前記承認処理器14は、電子承認信号を前記データ接続13を通して前記販売拠点10にある前記購入処理端末12へ送信する。前記購入処理端末12は、それに対して前記会員の購入のために前記承認信号の受取りを返す。

【0010】

前記処理器14によって購入が承認されると、次に前記処理器14は自動クリアリングハウス処理器17とのデータ接続16を確立する。この自動クリアリングハウス処理器17は前記承認処理器14に関連付けられている遠隔位置に設置されていることが好ましい。前記自動クリアリングハウス処理器17は、販売者口座20、会員口座21、組織口座22間の電子資金転送を実行するための電子資金転送ネットワーク18にさらに接続されている。購入毎に、前記承認処理器14は前記自動クリアリングハウス処理器17に対して以下の電子資金転送を実行するよう指示する:購入金額の前記会員口座へのデビット、前記購入金額の前記販売者の口座へのクレジット、前記ディスカウントまたは固定額の前記販売者の口座へのデビット、そして前記ディスカウントまたは固定額の前記組織口座へのクレジット。たとえば、10%のディスカウントレートの販売者での20ドルの購入については、20ドルのデビットが前記会員口座21にチャージされ、20ドルのクレジットが前記販売者口座20に支払われ、そして2ドルのデビットが前記販売者口座20にチャージされ、2ドルのクレジットが前記組織口座に支払われる。

【0011】

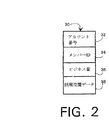

前記自動クリアリングハウス処理器17に資金移動を実行するよう指示することに加え、前記承認処理器14は、前記ネットワークマーケティング組織によって維持されるコミッション管理システム26へ購入データを送信するように構成されている。このコミッション管理システム26は、コミッション管理処理器27と、会員データや前記組織の組織構造に関する構造データを格納するための電子データベース28と、会員への支払いを実行するための自動プリント・メイル設備のような支払い処理器29とを有している。前記会員データと構造データは、図2に示される会員記録30のように、会員記録が複数から成る形で前記データベース28内に格納される。前記データベース28は、磁気ディスクやテープまたは他の公知の電子データ保存装置のような非揮発性マスデータ保存装置と互換性のある形式の電子データベースであることが望ましい。

【0012】

前記会員記録30は、複数のデータフィールド、すなわち口座番号を保存するためのアカウント番号フィールド32と、会員(会員の名前や住所など)に属する特定データを保存する会員特定フィールド34と、会員のデビットカード利用から生じる購入ディスカウントまたはその一部に関する記録を保存するパーソナルビジネス量フィールド36と、コミッション分配階層内での会員の位置を特定するデータを保存する階層位置データフィールド38を有している。このような階層位置データは、さらに以下に示されるように、例えば前記階層内で前記会員に従属している他会員の記録の、前記マスデータ保存装置内での位置を示すためのポインターを有する。

【0013】

前記承認処理器14が購入データを前記コミッション管理システム処理器27に送信する際、前記コミッション管理処理器27は受信した会員口座番号と前記データベース28’内に保存されている該当会員記録とを関連付ける。次に、前記コミッション管理システムは、前記該当するパーソナルビジネス量フィールド36の内容を取り出し、発生した前記購入金額を前記取り出されたパーソナルビジネス量に加え、そして前記データベース28内の前記会員記録30中に前記会員のパーソナルビジネス量の新しい値を保存する。

【0014】

一例のデータベース28内の会員記録間の関係を示す構造図は、図3の代表会員Aに関連付けられて図示されている。会員B〜Hの記録を含む下位構造はここで会員Aの「下位ネットワーク」とされる。前記データベース28’内の関係は以下のように確立される。会員Aが新会員をこの組織に入会させると、この新会員は前記階層内で会員Aに直接従属する位置に確立される。この新会員、例えば会員BとCは、会員Aによって勧誘された事実または上層のスポンサーによってリクルートされ配置された事実を各自の会員申込書に示す。前記階層内に確立された会員は新会員を入会させる資格が与えられ、これに続く世代の会員は会員Aの下層ネットワークを構成するよう確立される。

【0015】

新会員勧誘の動機付けと会員のデビットカード利用の動機付けを提供するために、前記組織口座22内に蓄積されたディスカウントクレジットからコミッションが払われる。前記コミッションは、毎週、毎月、年に2回、または年に1回のような定期間隔で支払われることが好ましい。特に好ましい実施例においては、コミッションは月1回の間隔で払われる。各会員のコミッションは、各自の下位ネットワーク内の会員のパーソナルビジネス量の総計に応じ、前記コミッション管理処理器27によって決定される。例えば、会員のコミッションは、前記下位ネットワークの各連続階級を階級用の選択部分に関連付けてなる表40に従って決定され、各会員の下位ネットワーク中の連続階級に位置している会員のパーソナルビジネス量の総計の所定の割合からなる。この表40は前記階層の一例に隣接して図3に示されている。前記表40に従って、会員Aは、会員BとCのパーソナルビジネス量の2%、会員DとEとFのパーソナルビジネス量の3%、会員GとHのパーソナルビジネス量の20%の割合でコミッションを受領し、合計$33.30を獲得することになる。前記割合の表40は前記コミッション管理システム26によって維持されていて、所定の間隔で各会員に返すべきコミッションを算出する際に参照される。

【0016】

会員が前記デビットカードを用いたり新会員を勧誘したりする動機を最大化するために、様々なコミッション表またはマルチレベル支払いプランが用いられていることは明らかである。さらに、このような動機付けを高めるために前記コミッション管理システム26の機能を拡張してもよい。前記デビットカードの利用を促進するための更なる動機付けとして、前記コミッションの支払いは、徐々に上がっていく資格閾値スケール(qualification threshold value)に応じて、ある会員の下位ネットワークの連続階級からコミッションを受領する資格を得るためのパーソナルビジネス量が所定レベルに到達することを条件とすることもできる。図3の例においては、会員Aは、自身の下位ネットワークの最初の3階級からコミッションをもらう資格を獲得するためには50ドル、第4から第6階級からもらうには100ドル、また第7と第8レベルも含む場合は200ドルのパーソナルビジネス量を蓄積する必要がある。別の実施例においては、会員のパーソナルビジネス量から、比率決定要素を算出する基礎を提供するようにしてもよく、その会員のコミッションを算出するために使われる比率の階級依存表40と組み合わせて使用される。

【0017】

前記コミッション管理処理器27が会員に払われるべきコミッションを決定すると、前記会員認識データとコミッション金額が支払い処理器サブシステム29に送信される。好ましい実施例においては、前記支払い処理器サブシステムは、会員に送られるべきコミッションの小切手を印刷するための自動プリンタ/郵送処理器を有する。別の実施例においては、前記支払い処理器サブシステムは、前記組織の口座22から前記会員の口座21へ前記コミッション額の電子資金移動を実行し、更に前記会員宛てに郵送される明細書を印刷する。

【0018】

会員が非現金式支払装置を利用したり新会員を勧誘するための動機付けは、さらに販売者に対しても前記組織とディスカウント契約を結ぶように勧誘するために用いてもよい。前記組織の会員は他の支払い手段よりも前記組織の支払い手段を好んで用いるよう動機付けられるため、また会員はより多いコミッション獲得の資格を得るために必要なパーソナルビジネス量を達成することを望むので、会員が参加している販売者から物を買う可能性が高い。この動機付けを作るために、販売者はマーケティングの目的で前記組織のデータベースへ限定的にアクセスを可能にしてもよい。例えば、各会員によって購入された商品のカテゴリーに関する総計的購入データは前記コミッション管理システムによって維持することが可能であり、販売者のマーケティング材料を前記組織のすでに動機付けられた会員のうちの特別に受容的な会員に向けることで販売者がより高い販促の効率性を達成できるようになる。従って、前記組織とディスカウント契約を結ぶことによって、販売者はその販売者から躊躇なく購入することにすでに動機付けられている人に販促材料を向けることによって高いマーケティング効果も獲得できる。例えば、会員がスポーツ用品を購入する相対的頻度は、販促材料を購入度の高いスポーツ用品の消費者に向けることを望んでいるスポーツ用品販売者にとって貴重な情報である。販売者に与えられるマーケティングサポートの度合いは、販売者によって提供されるディスカウントの大きさを条件とすることができる。

【0019】

上記で用いられた条件は説明上の条件であってそれに限定されるものではなく、本発明の範囲は下記請求項とそれを基にする同等のものによって定義されるべきものである。本発明は、この分野の当業者の技術の範囲内で変更が可能であることは明らかである。例えば、本発明の実施例は他の非現金支払装置に適用されてもよい。そのような変形においては、ここで用いられた「ディスカウント」という表現は、購入取引を処理するために販売者によって払われたプレミアムと、また販売者が購入価格に当てたディスカウントの意味と同様に使用される。同じように、そのような変形において、会員の「デビット口座」は、コミッションの支払いとは別、またはそれに伴った基準において会員に請求されるクレジット残高に適用される。

【図面の簡単な説明】

前記サマリーおよび後記詳述は添付図面と合わせると最も理解される。

【図1】 本発明の好ましい実施例による取引システムの機能ブロック図である。

【図2】 図1の取引システムのコミッション決算支払いデータベース中に保存された電子データベースのブロック図である。

【図3】 前記コミッション決算支払いデータベース中の電子データの組織を示す構造図である。[0001]

BACKGROUND OF THE INVENTION

The present invention relates to a non-cash base sales transaction system that manages purchase transactions and distributes purchase commissions between sellers and users of non-cash base sales transaction systems.

[0002]

[Prior art]

Non-cash payment devices such as debit cards and credit cards provide great convenience to purchasers of goods and services. However, such a payment apparatus requires an electronic transaction management / accounting system, and an operating cost is in addition to the cost of goods and services purchased with such an apparatus. Traditionally, issuers of non-cash payment devices enter into sales contracts and participating merchants pay commissions to card issuers in exchange for the convenience of using non-cash payment devices. It is like that. Recently, competition between card issuers has reduced the rate of commission paid by merchants. As a result, card issuers have attempted to increase transaction volume by providing consumers with a wide variety of motivations and actively advertising such motivations.

[0003]

Known motivational programs, such as those disclosed in McCarthy US Pat. No. 4,941,090, allow customers to be paid personal bonuses based on individual purchases made by non-cash payment devices. . Also, such motivation programs are attractive to individual customers, but must be effectively promoted to advertise and attract prospective customers. In addition, these motivational programs do not provide any benefit to participating merchants, but the merchants must still be registered under other non-cash payment systems and competitive commissions. Don't be. Therefore, it provides consumers with the motivation to use them in preference to other non-cash payment devices, encourages merchants to join, and reduces advertising costs associated with attracting and maintaining cardholders. It is desirable to develop a non-cash payment system that enables it.

Prior art document information related to the invention of this application includes the following (including documents cited in the international phase after the international filing date and documents cited when entering the country in other countries).

[Patent Document 1]

US Pat. No. 4,594,663 [Patent Document 2]

US Patent No. 4,750,119 [Patent Document 3]

US Patent No. 4,491,090 [Patent Document 4]

US Patent No. 5,025,372 [Patent Document 5]

US Pat. No. 5,117,355 [Patent Document 6]

US Patent No. 5,222,018 [Patent Document 7]

US Pat. No. 5,287,268 [Patent Document 8]

US Pat. No. 5,537,314 [Patent Document 9]

US Patent No. 5,826,241 [Patent Document 10]

US Patent No. 6,105,001 [Patent Document 11]

US Patent No. 5,581,041 [Non-patent Document 1]

P. A. Pays, "An intermediated and payment system technology" Computer Networks & ISDN Systems 28 (1996) pp. 1197-1206

[Non-Patent Document 2]

T. T. Baron "Banks, vendors focus on security" cited in "Abstracts of Recurrent Articles and Literacy" By Helen Collinson in Computers 14 (in Japanese). 409-414

[Non-Patent Document 3]

Amway USA "The Amway Opportunity in the USA-questions &answers" from http www. amway-usa. com / info / q & a. asp, (1998)

[Non-Patent Document 4]

6 sheets compiling article who dispose incentive rebates liking to the use of GM credit card. (From Dialog Search publishing dates, title, source of the articulated & related paragraph, fr. (1985)

[Non-Patent Document 5]

J. et al. Corry, “The Amway way: Seeking the profit of many” The American Spectator; Bloomington; Vol. 31,

[Non-Patent Document 6]

M.M. Rock, “This articulate doll make you a millinonair” from Institute of Directors, London; Vol. 48, Issue 7 (1995), pp. 1-4

[0004]

[Problems to be solved by the invention]

According to the present invention, the commission payment / accounting system organizes transaction data belonging to holders of non-cash payment devices such as debit cards and credit cards into a hierarchical database, and uses debit cards or joins new card members. Reflects the organizational structure of the motivational program for Commissions for purchases are electronically transferred to the card issuer, and the commission payment and accounting system associates stored electronic funds transaction data, intra-organizational relationships between card holders, and proportional commission rates with organizational relationships. The commission payment amount to the card holder is determined and distributed based on the predetermined table.

[0005]

DETAILED DESCRIPTION OF THE INVENTION

Referring to FIG. 1, an example of a non-cash payment and commission system according to the present invention is shown. This system is designed to manage purchases of goods and services by members of network marketing or multi-level marketing organizations (for example, humans or distributors), and management of commission payments to the organization members by hierarchical commission settlement / payment methods. ing. As will be described further below, each member is given a debit or credit card and can shop anywhere from a number of merchant locations, and the

[0006]

A base sales transaction processing terminal 12 (PPT) is installed at the

[0007]

When the member wants to shop at the

[0008]

The

[0009]

When the presented purchase is approved, the

[0010]

Once the purchase is approved by the

[0011]

In addition to instructing the

[0012]

The

[0013]

When the

[0014]

A structural diagram showing the relationship between the member records in the

[0015]

Commissions are paid from discount credits stored in the

[0016]

It is clear that various commission tables or multi-level payment plans are used to maximize the motivation for members to use the debit card or invite new members. Further, the function of the commission management system 26 may be expanded in order to enhance such motivation. As a further motivation to promote the use of the debit card, the commission payment is made from a continuous class of a member's sub-network according to a qualifying threshold value that gradually increases. It can also be conditioned on reaching a predetermined level of personal business volume to qualify for receipt. In the example of FIG. 3, member A receives $ 50 to qualify for commission from the first three classes of his subordinate network, $ 100 to receive commissions from the fourth to sixth classes, and seventh. And if the 8th level is included, it is necessary to accumulate a personal business volume of $ 200. In another embodiment, a basis for calculating the ratio determining factor from the member's personal business volume may be provided, in combination with the ratio class dependency table 40 used to calculate the member's commission. used.

[0017]

When the

[0018]

Motivation for members to use non-cash payment devices or solicit new members may also be used to solicit sellers to sign discounts with the organization. Because the members of the organization are motivated to prefer using the organization's payment means over other payment means, and the members wish to achieve the amount of personal business required to qualify for higher commissions Therefore, there is a high possibility that the member buys goods from the participating merchants. To create this motivation, the merchant may allow limited access to the organization's database for marketing purposes. For example, aggregate purchase data regarding the category of goods purchased by each member can be maintained by the commission management system, and the merchant's marketing material can be used specifically for the already motivated members of the organization. By turning to receptive members, sellers can achieve higher promotional efficiencies. Therefore, by signing a discount contract with the organization, the seller can also obtain a high marketing effect by directing promotional materials to those who are already motivated to purchase without hesitation from the seller. For example, the relative frequency with which members purchase sports equipment is valuable information for sports equipment sellers who want to direct promotional materials to consumers of sports equipment with a high degree of purchase. The degree of marketing support given to a seller can be conditioned on the amount of discount provided by the seller.

[0019]

The conditions used above are illustrative and not limiting, and the scope of the present invention is to be defined by the following claims and their equivalents. It will be apparent that the present invention can be modified within the skill of one of ordinary skill in the art. For example, embodiments of the present invention may be applied to other non-cash payment devices. In such variations, the term “discount” as used herein is similar to the premium paid by the seller to process the purchase transaction and the meaning of the discount that the seller has placed on the purchase price. used. Similarly, in such a variant, the member's “debit account” applies to the credit balance charged to the member on a basis separate from or associated with commission payments.

[Brief description of the drawings]

The summary and detailed description below are best understood when taken in conjunction with the accompanying drawings.

FIG. 1 is a functional block diagram of a transaction system according to a preferred embodiment of the present invention.

2 is a block diagram of an electronic database stored in a commission settlement payment database of the transaction system of FIG.

FIG. 3 is a structural diagram showing an organization of electronic data in the commission settlement payment database.

Claims (11)

前記コミッションシステムは、

販売拠点に設置されコンピュータによって実行される購入処理手段と、

各会員の預金口座、前記組織の預金口座及び前記販売拠点における販売者の口座間の電子資金転送をコンピュータによって実行するための電子資金転送ネットワークに接続され、当該電子送金処理を実行する支払処理手段と、

前記購入処理手段及び前記支払処理手段と通信回線を介して接続され、各会員に与えるべきコミッション金額の基準となるビジネス量値及び各会員の前記組織内における相対的な階層関係を示す位置データが各会員のIDに関連づけてられて会員記録として格納されたデータベースと、

このデータベースをコンピュータによって管理する管理手段と、

を有し、

このコミッション分配方法は、

コンピュータが、前記購入処理手段に、前記会員のカード使用による商品購入を受付けた場合に購入データを前記管理手段に送信させ、この管理手段に、前記購入データに基づき前記カードを保持する前記会員のIDを特定させて当該会員の購入データとして前記会員記録に記録させる工程と、

コンピュータが、前記管理手段に、前記購入データに基づいて前記特定された会員のビジネス量値を算出させ、この算出されたビジネス量値を前記特定された会員の会員記録にさらに記録させる工程と、

コンピュータが、前記購入データに基づいて前記支払処理手段に前記会員の預金口座から前記販売者の預金口座へ前記カード使用による購入価格と等しい金銭額を移動させると共に、前記販売者の預金口座から前記組織の預金口座へ所定の金銭額を移動させる工程と、

コンピュータが、前記管理手段に、予め設定された所定のタイミングで、前記データベースから一の会員のビジネス量値と、この一の会員とは異なる他の会員のビジネス量値と、前記位置データとを読み出させ、これらに基づき、前記一の会員に対するコミッション金額を算出させる工程と、

コンピュータが、前記支払処理手段に、前記組織の預金口座から前記一の会員の預金口座へ前記コミッション金額の電子資金移動を実行させる工程と

を有する方法。A commission distribution method for promoting the use of card payments, executed by a computer system and executed by a commission system for managing commission payments to a plurality of members who have joined a predetermined organization ,

The commission system is

Purchase processing means installed at the sales base and executed by a computer;

Payment processing means connected to an electronic funds transfer network for executing electronic funds transfer between a deposit account of each member, a deposit account of the organization and a seller's account at the sales base by a computer, and executing the electronic money transfer processing When,

A business amount value that is connected to the purchase processing means and the payment processing means via a communication line and serves as a reference for a commission amount to be given to each member, and position data that indicates a relative hierarchical relationship within each organization of each member. A database associated with each member's ID and stored as a member record;

Management means for managing this database by a computer;

Have

This commission distribution method is

Computer, the purchase processing unit, the purchase data in the case of receiving a product purchase by the member of the card used is transmitted to the management unit, in the management means, of the member for holding the card on the basis of the purchase data Allowing the ID to be specified and recorded in the member record as purchase data of the member ;

A step of causing the management means to calculate a business amount value of the identified member based on the purchase data, and further recording the calculated business amount value in the member record of the identified member;

The computer moves the payment processing means based on the purchase data from the member's savings account to the seller's savings account for a monetary amount equal to the purchase price by using the card, and from the seller's savings account to Transferring a predetermined amount of money to the organization's deposit account;

Computer, said management means, at a predetermined timing set in advance, and business volume value of one member from the database, and business volume values of different other member this one member, and the position data And calculating a commission amount for the one member based on these , and

A computer causing said payment processing means to perform electronic money transfer of said commission amount from said organization deposit account to said one member deposit account .

前記位置データには、前記階層内で前記一会員に従属して連なる前記他の会員が従属会員として含まれており、

前記コミッション金額を算出する工程は、

コンピュータが、前記管理手段によって予め設定された所定のタイミングで、前記データベースから前記一の会員のビジネス量値と、各従属会員のビジネス量値と、前記位置データとを読み出し、これらに基づいて前記一の会員に対する前記コミッション金額を算出する工程を有する。The method of claim 1, comprising:

In the position data, the other members that are subordinate to the one member in the hierarchy are included as subordinate members,

The step of calculating the commission amount includes

Computer, a predetermined timing set in advance by the management unit, a business volume value of the one member from the database, and business quantity value of each dependent member, reads said position data, on the basis of these Calculating the commission amount for one member .

前記コミッション金額を算出する工程は、

コンピュータが、前記データベースに格納され比率的コミッションレートを前記階層の各連続従属階級と関連付けてなる比率表に基づき、前記コミッション金額を算出する工程を更に含むものである。The method of claim 2, comprising:

The step of calculating the commission amount includes

Computer, based on a proportionally commission rate stored in the database to the ratio table comprising in association with each successive subordinate classes of the hierarchy, is intended to include the additional step of calculating the commission amount.

前記コミッション金額を算出する工程は、

コンピュータが、前記データベースに格納され各会員が優遇措置を得るための前記ビジネス量値に関するテーブルに基づいて前記コミッション金額を算出する工程を更に含むものである。The method of claim 3, comprising:

The step of calculating the commission amount includes

Computer, in which each member is stored in the database further comprises the step of calculating the commission amount based on the table about the business volume value to obtain preferential treatment.

前記コミッション金額を算出する工程は、

コンピュータが、前記優遇措置を得るための前記ビジネス量値に関するテーブルを前記データベースから取り出して処理し、以下のものを決定する:

(i)前記一会員に対するコミッション支払いのためのビジネス量閾値、

(ii)前記従属会員の会員記録に含まれる前記コミッション金額を決定するために引き出される従属会員階層に対応した階級値。The method of claim 4, comprising:

The step of calculating the commission amount includes

Computer, a table relating to the business volume value to obtain the preferential treatment processes removed from the database, to determine the following:

(I) a business volume threshold for commission payment to the one member;

Class value corresponding to the subordinate member hierarchy drawn to determine the commission amount contained in the membership records of (ii) the dependent members.

前記カードは、少なくともデビットカードを含み、

前記コミッションシステムは、

コンピュータが、前記デビットカードから会員の情報を読取り会員の正当性を承認する承認処理器をさらに有し、

この方法は、さらに、

コンピュータが、前記デビット承認処理器によって前記購入処理手段から前記購入データを受け取り、前記購入データを前記管理処理手段へ転送する工程と、

コンピュータが、前記デビット承認処理器から前記購入処理手段へ電子承認信号を発する工程と、

コンピュータが、前記デビット承認処理器から前記支払処理手段へ資金転送を実行させるための電子の指令を送信し、前記支払処理手段によって前記一会員の預金口座から購入が行われた販売者の預金口座へ購入価格と等しい金銭額を移動する工程と、

コンピュータが、前記購入処理手段によって前記購入が行われた販売者の預金口座から前記組織の預金口座へ所定の金銭額を移動する工程とを有する。The method of claim 1 , comprising:

Before Symbol card, it includes at least a debit card,

The commission system is

The computer further comprises an approval processor that reads the member information from the debit card and approves the validity of the member,

This method further

Computer, the steps of said receiving the purchase data from the purchase processing unit by debit authorization processor, transferring the purchase data Previous Symbol management processing unit,

A computer issuing an electronic approval signal from the debit approval processor to the purchase processing means;

Computer, the debit approval from the processor to the payment processing means to send an e-command to execute the funds transfer, the payment processing means by the one member deposit accounts from the bank account purchase is made the seller of Transferring a monetary amount equal to the purchase price to

Computer, and a step of moving a predetermined monetary amount to deposit account of the tissue from the bank account of the purchases that were made merchant by said purchase processing means.

前記コミッションシステムは、さらに、

会員に送られるべきコミッション金額を小切手に印刷する印刷手段を有し、

この方法は、さらに、

コンピュータが、前記印刷手段に、前記一会員宛の小切手に前記算出されたコミッション金額を印刷させる工程

を有する方法。 The method of claim 1, comprising:

The commission system further comprises:

Has a printing means to print the commission amount to be sent to the member on a check,

This method further

Process computer, in the printing unit, to print the commission amount to the calculated the check destined the one member

Having a method.

前記カードはクレジットカードおよびデビットカードのうちの1つであって、

前記カードは前記一会員を特定するための磁気的にエンコードされた記号をその上に有しており、

この方法は、

前記磁気的にエンコードされた記号を前記デビット承認処理器へ送信するための前記購入データに変換する工程をさらに有する。The method of claim 1, wherein

The card is a one of a credit card and debit card,

The card has a symbol that is magnetically encoded for identifying the one member thereon,

This method

The method further comprises converting the magnetically encoded symbol into the purchase data for transmission to the debit authorization processor.

Applications Claiming Priority (1)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| PCT/US2000/020196 WO2002008992A2 (en) | 1997-08-15 | 2000-07-25 | Non-cash transaction incentive and commission distribution system |

Publications (3)

| Publication Number | Publication Date |

|---|---|

| JP2004505352A JP2004505352A (en) | 2004-02-19 |

| JP2004505352A5 JP2004505352A5 (en) | 2008-07-31 |

| JP4583708B2 true JP4583708B2 (en) | 2010-11-17 |

Family

ID=21741613

Family Applications (1)

| Application Number | Title | Priority Date | Filing Date |

|---|---|---|---|

| JP2002514622A Expired - Lifetime JP4583708B2 (en) | 2000-07-25 | 2000-07-25 | Motivation and commission distribution system for non-cash transactions |

Country Status (5)

| Country | Link |

|---|---|

| JP (1) | JP4583708B2 (en) |

| KR (1) | KR20030040375A (en) |

| AU (2) | AU2000263722B2 (en) |

| CA (1) | CA2417219A1 (en) |

| MX (1) | MXPA03000733A (en) |

Family Cites Families (5)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| US5025372A (en) * | 1987-09-17 | 1991-06-18 | Meridian Enterprises, Inc. | System and method for administration of incentive award program through use of credit |

| US4941090A (en) * | 1989-01-27 | 1990-07-10 | Mccarthy Patrick D | Centralized consumer cash value accumulation system for multiple merchants |

| US5537314A (en) * | 1994-04-18 | 1996-07-16 | First Marketrust Intl. | Referral recognition system for an incentive award program |

| US5826241A (en) * | 1994-09-16 | 1998-10-20 | First Virtual Holdings Incorporated | Computerized system for making payments and authenticating transactions over the internet |

| JPH11272754A (en) * | 1998-03-25 | 1999-10-08 | Gs Joho System Kk | Customer service system, record medium card for member used in this system, and record medium with customer service system program recorded |

-

2000

- 2000-07-25 AU AU2000263722A patent/AU2000263722B2/en not_active Ceased

- 2000-07-25 JP JP2002514622A patent/JP4583708B2/en not_active Expired - Lifetime

- 2000-07-25 KR KR10-2003-7001081A patent/KR20030040375A/en not_active Application Discontinuation

- 2000-07-25 AU AU6372200A patent/AU6372200A/en active Pending

- 2000-07-25 CA CA002417219A patent/CA2417219A1/en not_active Abandoned

- 2000-07-25 MX MXPA03000733A patent/MXPA03000733A/en unknown

Also Published As

| Publication number | Publication date |

|---|---|

| KR20030040375A (en) | 2003-05-22 |

| JP2004505352A (en) | 2004-02-19 |

| CA2417219A1 (en) | 2002-01-31 |

| AU2000263722B2 (en) | 2008-03-20 |

| MXPA03000733A (en) | 2004-11-01 |

| AU6372200A (en) | 2002-02-05 |

Similar Documents

| Publication | Publication Date | Title |

|---|---|---|

| US6105001A (en) | Non-cash transaction incentive and commission distribution system | |

| US8930270B2 (en) | Smart payment instrument selection | |

| US8001048B2 (en) | Non-cash transaction incentive and commission distribution system | |

| US5025372A (en) | System and method for administration of incentive award program through use of credit | |

| US8412629B2 (en) | Non-cash transaction incentive and commission distribution system | |

| RU2598590C2 (en) | Pos system using network of prepaid/gift cards | |

| US20050131792A1 (en) | Financial transaction system with integrated, automatic reward detection | |

| US20080201230A1 (en) | Internet-based method of and system for equity ownership optimization within a financial and retail marketplace | |

| US20070051797A1 (en) | Methods and systems for packaging and distributing financial instruments | |

| US20040049423A1 (en) | Point return method and apparatus | |

| US7472073B1 (en) | Non-cash transaction incentive and commission distribution system | |

| US20040249752A1 (en) | Charity funding method using an open-ended stored-value card | |

| US20040049421A1 (en) | Point sales server and point sales method | |

| WO2005029284A2 (en) | Club membership for discounted buying | |

| US20040225605A1 (en) | Account-based electronic music access system and method | |

| CA2398520A1 (en) | Internet related discount coupon rebate business method | |

| JP2000113327A (en) | Point card system | |

| US20130231986A1 (en) | Non-cash transaction incentive and commission distribution system | |

| US20030220839A1 (en) | Coupon rebate business method using portable presonal communication devices | |

| US20030036957A1 (en) | Internet related discount coupon rebate business method | |

| JP2002032681A (en) | Business method and business operation managing device | |

| JP2001306952A (en) | Purchasing and settling system | |

| JP4583708B2 (en) | Motivation and commission distribution system for non-cash transactions | |

| US20080288340A1 (en) | System and method for providing a pre-paid rebate card | |

| JP2002099966A (en) | Point bank system and point-issuing terminal |

Legal Events

| Date | Code | Title | Description |

|---|---|---|---|

| A621 | Written request for application examination |

Free format text: JAPANESE INTERMEDIATE CODE: A621 Effective date: 20070725 |

|

| A521 | Written amendment |

Free format text: JAPANESE INTERMEDIATE CODE: A523 Effective date: 20080610 |

|

| A131 | Notification of reasons for refusal |

Free format text: JAPANESE INTERMEDIATE CODE: A131 Effective date: 20100223 |

|

| A601 | Written request for extension of time |

Free format text: JAPANESE INTERMEDIATE CODE: A601 Effective date: 20100515 |

|

| A602 | Written permission of extension of time |

Free format text: JAPANESE INTERMEDIATE CODE: A602 Effective date: 20100524 |

|

| A601 | Written request for extension of time |

Free format text: JAPANESE INTERMEDIATE CODE: A601 Effective date: 20100623 |

|

| A602 | Written permission of extension of time |

Free format text: JAPANESE INTERMEDIATE CODE: A602 Effective date: 20100630 |

|

| A521 | Written amendment |

Free format text: JAPANESE INTERMEDIATE CODE: A523 Effective date: 20100716 |

|

| TRDD | Decision of grant or rejection written | ||

| A01 | Written decision to grant a patent or to grant a registration (utility model) |

Free format text: JAPANESE INTERMEDIATE CODE: A01 Effective date: 20100810 |

|

| A01 | Written decision to grant a patent or to grant a registration (utility model) |

Free format text: JAPANESE INTERMEDIATE CODE: A01 |

|

| A61 | First payment of annual fees (during grant procedure) |

Free format text: JAPANESE INTERMEDIATE CODE: A61 Effective date: 20100901 |

|

| R150 | Certificate of patent or registration of utility model |

Free format text: JAPANESE INTERMEDIATE CODE: R150 Ref document number: 4583708 Country of ref document: JP Free format text: JAPANESE INTERMEDIATE CODE: R150 |

|

| FPAY | Renewal fee payment (event date is renewal date of database) |

Free format text: PAYMENT UNTIL: 20130910 Year of fee payment: 3 |

|

| R250 | Receipt of annual fees |

Free format text: JAPANESE INTERMEDIATE CODE: R250 |

|

| R250 | Receipt of annual fees |

Free format text: JAPANESE INTERMEDIATE CODE: R250 |

|

| R250 | Receipt of annual fees |

Free format text: JAPANESE INTERMEDIATE CODE: R250 |

|

| R250 | Receipt of annual fees |

Free format text: JAPANESE INTERMEDIATE CODE: R250 |

|

| R250 | Receipt of annual fees |

Free format text: JAPANESE INTERMEDIATE CODE: R250 |

|

| R250 | Receipt of annual fees |

Free format text: JAPANESE INTERMEDIATE CODE: R250 |

|

| R250 | Receipt of annual fees |

Free format text: JAPANESE INTERMEDIATE CODE: R250 |

|

| EXPY | Cancellation because of completion of term |