CN116113967A - System and method for controlling digital knowledge dependent rights - Google Patents

System and method for controlling digital knowledge dependent rights Download PDFInfo

- Publication number

- CN116113967A CN116113967A CN202180063278.1A CN202180063278A CN116113967A CN 116113967 A CN116113967 A CN 116113967A CN 202180063278 A CN202180063278 A CN 202180063278A CN 116113967 A CN116113967 A CN 116113967A

- Authority

- CN

- China

- Prior art keywords

- knowledge

- smart contract

- digital

- distribution system

- distributed ledger

- Prior art date

- Legal status (The legal status is an assumption and is not a legal conclusion. Google has not performed a legal analysis and makes no representation as to the accuracy of the status listed.)

- Pending

Links

- 238000000034 method Methods 0.000 title claims abstract description 753

- 230000001419 dependent effect Effects 0.000 title description 13

- 230000008569 process Effects 0.000 claims abstract description 492

- 230000009471 action Effects 0.000 claims abstract description 288

- 238000009826 distribution Methods 0.000 claims description 321

- 238000007726 management method Methods 0.000 claims description 302

- 238000004519 manufacturing process Methods 0.000 claims description 215

- 230000004044 response Effects 0.000 claims description 193

- 238000012545 processing Methods 0.000 claims description 179

- 238000012544 monitoring process Methods 0.000 claims description 152

- 238000004458 analytical method Methods 0.000 claims description 114

- 238000004891 communication Methods 0.000 claims description 106

- 230000006854 communication Effects 0.000 claims description 106

- 238000004422 calculation algorithm Methods 0.000 claims description 86

- 230000002776 aggregation Effects 0.000 claims description 66

- 238000004220 aggregation Methods 0.000 claims description 66

- 238000012795 verification Methods 0.000 claims description 61

- 238000012546 transfer Methods 0.000 claims description 54

- 238000012358 sourcing Methods 0.000 claims description 22

- 235000013305 food Nutrition 0.000 claims description 16

- 239000013078 crystal Substances 0.000 claims description 9

- 229920000642 polymer Polymers 0.000 claims description 9

- 238000002360 preparation method Methods 0.000 claims description 9

- 239000004065 semiconductor Substances 0.000 claims description 8

- 238000000576 coating method Methods 0.000 claims description 7

- 238000003786 synthesis reaction Methods 0.000 claims description 7

- 238000013473 artificial intelligence Methods 0.000 description 312

- 230000008901 benefit Effects 0.000 description 290

- 230000000694 effects Effects 0.000 description 255

- 238000010801 machine learning Methods 0.000 description 237

- 238000013528 artificial neural network Methods 0.000 description 232

- 238000004088 simulation Methods 0.000 description 172

- 230000006399 behavior Effects 0.000 description 162

- 238000012549 training Methods 0.000 description 129

- 238000013480 data collection Methods 0.000 description 128

- 230000003993 interaction Effects 0.000 description 123

- 238000003860 storage Methods 0.000 description 123

- 238000004801 process automation Methods 0.000 description 111

- 239000000047 product Substances 0.000 description 110

- 238000005259 measurement Methods 0.000 description 106

- 230000000875 corresponding effect Effects 0.000 description 102

- 230000006870 function Effects 0.000 description 95

- 238000012800 visualization Methods 0.000 description 94

- 230000013016 learning Effects 0.000 description 92

- 230000033001 locomotion Effects 0.000 description 88

- 230000008859 change Effects 0.000 description 84

- 239000003795 chemical substances by application Substances 0.000 description 81

- 230000001105 regulatory effect Effects 0.000 description 66

- 230000007613 environmental effect Effects 0.000 description 62

- 230000003044 adaptive effect Effects 0.000 description 61

- 230000015654 memory Effects 0.000 description 61

- 230000008520 organization Effects 0.000 description 56

- 238000012423 maintenance Methods 0.000 description 55

- 238000013500 data storage Methods 0.000 description 53

- 230000000670 limiting effect Effects 0.000 description 52

- 239000000463 material Substances 0.000 description 51

- 238000001514 detection method Methods 0.000 description 46

- 230000001149 cognitive effect Effects 0.000 description 44

- 238000013461 design Methods 0.000 description 43

- 230000000007 visual effect Effects 0.000 description 41

- 238000007689 inspection Methods 0.000 description 39

- 239000013598 vector Substances 0.000 description 39

- 238000005516 engineering process Methods 0.000 description 37

- 238000001228 spectrum Methods 0.000 description 35

- 238000005065 mining Methods 0.000 description 34

- 230000019771 cognition Effects 0.000 description 33

- 230000007774 longterm Effects 0.000 description 32

- 230000001976 improved effect Effects 0.000 description 31

- 230000010354 integration Effects 0.000 description 31

- 230000006872 improvement Effects 0.000 description 30

- 230000033228 biological regulation Effects 0.000 description 29

- 210000004556 brain Anatomy 0.000 description 28

- 238000010586 diagram Methods 0.000 description 28

- 238000013145 classification model Methods 0.000 description 27

- 208000018910 keratinopathic ichthyosis Diseases 0.000 description 27

- 230000002265 prevention Effects 0.000 description 27

- 230000004308 accommodation Effects 0.000 description 26

- 210000002569 neuron Anatomy 0.000 description 26

- 238000005457 optimization Methods 0.000 description 26

- 230000003190 augmentative effect Effects 0.000 description 25

- 230000001276 controlling effect Effects 0.000 description 25

- 230000006855 networking Effects 0.000 description 25

- 230000001960 triggered effect Effects 0.000 description 25

- 230000002349 favourable effect Effects 0.000 description 22

- 239000012530 fluid Substances 0.000 description 21

- 238000004364 calculation method Methods 0.000 description 20

- 230000036541 health Effects 0.000 description 20

- 239000007788 liquid Substances 0.000 description 20

- 241000282412 Homo Species 0.000 description 19

- 230000003542 behavioural effect Effects 0.000 description 19

- 230000007246 mechanism Effects 0.000 description 19

- 230000000306 recurrent effect Effects 0.000 description 19

- 230000004931 aggregating effect Effects 0.000 description 18

- 230000006378 damage Effects 0.000 description 18

- 230000001965 increasing effect Effects 0.000 description 18

- 230000009183 running Effects 0.000 description 18

- 230000001133 acceleration Effects 0.000 description 17

- 238000013527 convolutional neural network Methods 0.000 description 17

- 238000011156 evaluation Methods 0.000 description 17

- 238000012552 review Methods 0.000 description 17

- 238000012384 transportation and delivery Methods 0.000 description 17

- 230000009286 beneficial effect Effects 0.000 description 16

- 230000005540 biological transmission Effects 0.000 description 16

- 238000001914 filtration Methods 0.000 description 15

- 238000012360 testing method Methods 0.000 description 15

- XLYOFNOQVPJJNP-UHFFFAOYSA-N water Substances O XLYOFNOQVPJJNP-UHFFFAOYSA-N 0.000 description 14

- 238000012550 audit Methods 0.000 description 13

- 239000007787 solid Substances 0.000 description 13

- 238000010146 3D printing Methods 0.000 description 12

- 238000013135 deep learning Methods 0.000 description 12

- 230000007547 defect Effects 0.000 description 12

- 239000007789 gas Substances 0.000 description 12

- 239000000126 substance Substances 0.000 description 12

- 238000003066 decision tree Methods 0.000 description 11

- 230000002068 genetic effect Effects 0.000 description 11

- 230000004048 modification Effects 0.000 description 11

- 238000012986 modification Methods 0.000 description 11

- 238000003909 pattern recognition Methods 0.000 description 11

- 230000002123 temporal effect Effects 0.000 description 11

- 238000001816 cooling Methods 0.000 description 10

- 230000001788 irregular Effects 0.000 description 10

- 238000003012 network analysis Methods 0.000 description 10

- 238000013439 planning Methods 0.000 description 10

- 230000004913 activation Effects 0.000 description 9

- 238000001994 activation Methods 0.000 description 9

- 238000011960 computer-aided design Methods 0.000 description 9

- 238000007596 consolidation process Methods 0.000 description 9

- 238000010276 construction Methods 0.000 description 9

- 238000006073 displacement reaction Methods 0.000 description 9

- 230000008676 import Effects 0.000 description 9

- -1 jewelry Substances 0.000 description 9

- 230000000116 mitigating effect Effects 0.000 description 9

- 230000036961 partial effect Effects 0.000 description 9

- 239000010970 precious metal Substances 0.000 description 9

- 238000012706 support-vector machine Methods 0.000 description 9

- 230000001413 cellular effect Effects 0.000 description 8

- 238000006243 chemical reaction Methods 0.000 description 8

- 230000003247 decreasing effect Effects 0.000 description 8

- 238000004146 energy storage Methods 0.000 description 8

- 230000001939 inductive effect Effects 0.000 description 8

- 230000000977 initiatory effect Effects 0.000 description 8

- 238000013507 mapping Methods 0.000 description 8

- 230000003287 optical effect Effects 0.000 description 8

- 230000005855 radiation Effects 0.000 description 8

- 238000005067 remediation Methods 0.000 description 8

- 238000010845 search algorithm Methods 0.000 description 8

- 230000035882 stress Effects 0.000 description 8

- 230000008093 supporting effect Effects 0.000 description 8

- 235000013361 beverage Nutrition 0.000 description 7

- 238000004140 cleaning Methods 0.000 description 7

- 238000011161 development Methods 0.000 description 7

- 230000018109 developmental process Effects 0.000 description 7

- 238000005553 drilling Methods 0.000 description 7

- 239000010437 gem Substances 0.000 description 7

- 238000013178 mathematical model Methods 0.000 description 7

- 238000003058 natural language processing Methods 0.000 description 7

- 230000003334 potential effect Effects 0.000 description 7

- 238000007639 printing Methods 0.000 description 7

- 230000035945 sensitivity Effects 0.000 description 7

- 230000003068 static effect Effects 0.000 description 7

- CURLTUGMZLYLDI-UHFFFAOYSA-N Carbon dioxide Chemical compound O=C=O CURLTUGMZLYLDI-UHFFFAOYSA-N 0.000 description 6

- RWSOTUBLDIXVET-UHFFFAOYSA-N Dihydrogen sulfide Chemical compound S RWSOTUBLDIXVET-UHFFFAOYSA-N 0.000 description 6

- 230000003466 anti-cipated effect Effects 0.000 description 6

- 230000007177 brain activity Effects 0.000 description 6

- 239000003086 colorant Substances 0.000 description 6

- 238000004590 computer program Methods 0.000 description 6

- 230000005670 electromagnetic radiation Effects 0.000 description 6

- 238000000605 extraction Methods 0.000 description 6

- 238000010438 heat treatment Methods 0.000 description 6

- 210000000478 neocortex Anatomy 0.000 description 6

- 239000003921 oil Substances 0.000 description 6

- 230000000704 physical effect Effects 0.000 description 6

- 230000008439 repair process Effects 0.000 description 6

- 238000005070 sampling Methods 0.000 description 6

- 231100000430 skin reaction Toxicity 0.000 description 6

- 239000013589 supplement Substances 0.000 description 6

- 238000010200 validation analysis Methods 0.000 description 6

- RTZKZFJDLAIYFH-UHFFFAOYSA-N Diethyl ether Chemical compound CCOCC RTZKZFJDLAIYFH-UHFFFAOYSA-N 0.000 description 5

- 229910000831 Steel Inorganic materials 0.000 description 5

- 230000006978 adaptation Effects 0.000 description 5

- 239000000446 fuel Substances 0.000 description 5

- 208000014674 injury Diseases 0.000 description 5

- 229910052500 inorganic mineral Inorganic materials 0.000 description 5

- 238000005304 joining Methods 0.000 description 5

- 238000011068 loading method Methods 0.000 description 5

- 239000011707 mineral Substances 0.000 description 5

- 238000010606 normalization Methods 0.000 description 5

- 238000004806 packaging method and process Methods 0.000 description 5

- 230000000737 periodic effect Effects 0.000 description 5

- 230000010399 physical interaction Effects 0.000 description 5

- 238000010248 power generation Methods 0.000 description 5

- 238000000611 regression analysis Methods 0.000 description 5

- 230000002787 reinforcement Effects 0.000 description 5

- 230000002441 reversible effect Effects 0.000 description 5

- 239000010959 steel Substances 0.000 description 5

- 241000700605 Viruses Species 0.000 description 4

- 208000027418 Wounds and injury Diseases 0.000 description 4

- 230000032683 aging Effects 0.000 description 4

- 238000012790 confirmation Methods 0.000 description 4

- 238000013523 data management Methods 0.000 description 4

- 230000003111 delayed effect Effects 0.000 description 4

- 230000008451 emotion Effects 0.000 description 4

- 238000005265 energy consumption Methods 0.000 description 4

- 230000007717 exclusion Effects 0.000 description 4

- 230000004438 eyesight Effects 0.000 description 4

- 230000004927 fusion Effects 0.000 description 4

- 238000010191 image analysis Methods 0.000 description 4

- 238000003384 imaging method Methods 0.000 description 4

- 230000004807 localization Effects 0.000 description 4

- 238000005461 lubrication Methods 0.000 description 4

- 230000014759 maintenance of location Effects 0.000 description 4

- 239000000203 mixture Substances 0.000 description 4

- 210000003205 muscle Anatomy 0.000 description 4

- 230000001537 neural effect Effects 0.000 description 4

- 230000001737 promoting effect Effects 0.000 description 4

- 239000002994 raw material Substances 0.000 description 4

- 230000002829 reductive effect Effects 0.000 description 4

- 238000007670 refining Methods 0.000 description 4

- 238000009877 rendering Methods 0.000 description 4

- 230000008521 reorganization Effects 0.000 description 4

- 238000011144 upstream manufacturing Methods 0.000 description 4

- 239000000654 additive Substances 0.000 description 3

- 230000000996 additive effect Effects 0.000 description 3

- 238000003491 array Methods 0.000 description 3

- 230000000712 assembly Effects 0.000 description 3

- 238000000429 assembly Methods 0.000 description 3

- 229910002092 carbon dioxide Inorganic materials 0.000 description 3

- 239000001569 carbon dioxide Substances 0.000 description 3

- 230000006835 compression Effects 0.000 description 3

- 238000007906 compression Methods 0.000 description 3

- 238000007405 data analysis Methods 0.000 description 3

- 230000010365 information processing Effects 0.000 description 3

- 230000002452 interceptive effect Effects 0.000 description 3

- 238000003064 k means clustering Methods 0.000 description 3

- 239000011159 matrix material Substances 0.000 description 3

- 238000007781 pre-processing Methods 0.000 description 3

- 230000002360 prefrontal effect Effects 0.000 description 3

- 230000001681 protective effect Effects 0.000 description 3

- 238000012797 qualification Methods 0.000 description 3

- 238000007637 random forest analysis Methods 0.000 description 3

- 230000009467 reduction Effects 0.000 description 3

- 230000006403 short-term memory Effects 0.000 description 3

- 238000000638 solvent extraction Methods 0.000 description 3

- 238000013179 statistical model Methods 0.000 description 3

- 230000007704 transition Effects 0.000 description 3

- 241000239290 Araneae Species 0.000 description 2

- 230000005483 Hooke's law Effects 0.000 description 2

- XUIMIQQOPSSXEZ-UHFFFAOYSA-N Silicon Chemical compound [Si] XUIMIQQOPSSXEZ-UHFFFAOYSA-N 0.000 description 2

- BQCADISMDOOEFD-UHFFFAOYSA-N Silver Chemical group [Ag] BQCADISMDOOEFD-UHFFFAOYSA-N 0.000 description 2

- 230000002159 abnormal effect Effects 0.000 description 2

- 125000002015 acyclic group Chemical group 0.000 description 2

- 230000002411 adverse Effects 0.000 description 2

- 238000004378 air conditioning Methods 0.000 description 2

- 238000013475 authorization Methods 0.000 description 2

- 230000004888 barrier function Effects 0.000 description 2

- 238000009412 basement excavation Methods 0.000 description 2

- 230000002457 bidirectional effect Effects 0.000 description 2

- 230000008049 biological aging Effects 0.000 description 2

- 230000003592 biomimetic effect Effects 0.000 description 2

- 238000009530 blood pressure measurement Methods 0.000 description 2

- 230000036760 body temperature Effects 0.000 description 2

- 230000001364 causal effect Effects 0.000 description 2

- 210000004027 cell Anatomy 0.000 description 2

- 239000007795 chemical reaction product Substances 0.000 description 2

- 238000007621 cluster analysis Methods 0.000 description 2

- 230000002860 competitive effect Effects 0.000 description 2

- 150000001875 compounds Chemical class 0.000 description 2

- 238000012937 correction Methods 0.000 description 2

- 230000008878 coupling Effects 0.000 description 2

- 238000010168 coupling process Methods 0.000 description 2

- 238000005859 coupling reaction Methods 0.000 description 2

- 238000005336 cracking Methods 0.000 description 2

- 230000001186 cumulative effect Effects 0.000 description 2

- 238000013075 data extraction Methods 0.000 description 2

- 230000006837 decompression Effects 0.000 description 2

- 238000011143 downstream manufacturing Methods 0.000 description 2

- 239000000428 dust Substances 0.000 description 2

- 230000005520 electrodynamics Effects 0.000 description 2

- 230000005672 electromagnetic field Effects 0.000 description 2

- 230000002708 enhancing effect Effects 0.000 description 2

- 238000005530 etching Methods 0.000 description 2

- 230000000763 evoking effect Effects 0.000 description 2

- 239000004744 fabric Substances 0.000 description 2

- 238000011049 filling Methods 0.000 description 2

- 230000010006 flight Effects 0.000 description 2

- 230000008014 freezing Effects 0.000 description 2

- 238000007710 freezing Methods 0.000 description 2

- 210000005153 frontal cortex Anatomy 0.000 description 2

- 230000014509 gene expression Effects 0.000 description 2

- 239000011521 glass Substances 0.000 description 2

- 230000003862 health status Effects 0.000 description 2

- 235000003642 hunger Nutrition 0.000 description 2

- 210000002364 input neuron Anatomy 0.000 description 2

- 238000002372 labelling Methods 0.000 description 2

- 238000012417 linear regression Methods 0.000 description 2

- 244000144972 livestock Species 0.000 description 2

- 230000001050 lubricating effect Effects 0.000 description 2

- 238000002844 melting Methods 0.000 description 2

- 230000008018 melting Effects 0.000 description 2

- 229910052751 metal Inorganic materials 0.000 description 2

- 239000002184 metal Substances 0.000 description 2

- 230000005012 migration Effects 0.000 description 2

- 238000013508 migration Methods 0.000 description 2

- 230000001936 parietal effect Effects 0.000 description 2

- 239000002245 particle Substances 0.000 description 2

- 230000008447 perception Effects 0.000 description 2

- 230000002085 persistent effect Effects 0.000 description 2

- 239000003208 petroleum Substances 0.000 description 2

- 230000037081 physical activity Effects 0.000 description 2

- 238000001556 precipitation Methods 0.000 description 2

- 238000013139 quantization Methods 0.000 description 2

- 238000012394 real-time manufacturing Methods 0.000 description 2

- 238000005215 recombination Methods 0.000 description 2

- 230000006798 recombination Effects 0.000 description 2

- 230000000246 remedial effect Effects 0.000 description 2

- 238000011160 research Methods 0.000 description 2

- 238000013468 resource allocation Methods 0.000 description 2

- 230000029058 respiratory gaseous exchange Effects 0.000 description 2

- 238000000926 separation method Methods 0.000 description 2

- 229910052710 silicon Inorganic materials 0.000 description 2

- 239000010703 silicon Substances 0.000 description 2

- 239000004984 smart glass Substances 0.000 description 2

- 239000000779 smoke Substances 0.000 description 2

- 230000005236 sound signal Effects 0.000 description 2

- 238000007619 statistical method Methods 0.000 description 2

- 230000001502 supplementing effect Effects 0.000 description 2

- 230000002459 sustained effect Effects 0.000 description 2

- 230000009466 transformation Effects 0.000 description 2

- 230000001052 transient effect Effects 0.000 description 2

- 230000007306 turnover Effects 0.000 description 2

- 238000002211 ultraviolet spectrum Methods 0.000 description 2

- 230000016776 visual perception Effects 0.000 description 2

- 239000002699 waste material Substances 0.000 description 2

- 206010000372 Accident at work Diseases 0.000 description 1

- 208000012260 Accidental injury Diseases 0.000 description 1

- 206010048909 Boredom Diseases 0.000 description 1

- UGFAIRIUMAVXCW-UHFFFAOYSA-N Carbon monoxide Chemical compound [O+]#[C-] UGFAIRIUMAVXCW-UHFFFAOYSA-N 0.000 description 1

- 101150054987 ChAT gene Proteins 0.000 description 1

- 235000008733 Citrus aurantifolia Nutrition 0.000 description 1

- 206010073306 Exposure to radiation Diseases 0.000 description 1

- 238000006424 Flood reaction Methods 0.000 description 1

- 208000001613 Gambling Diseases 0.000 description 1

- WQZGKKKJIJFFOK-GASJEMHNSA-N Glucose Natural products OC[C@H]1OC(O)[C@H](O)[C@@H](O)[C@@H]1O WQZGKKKJIJFFOK-GASJEMHNSA-N 0.000 description 1

- 230000005355 Hall effect Effects 0.000 description 1

- 238000012614 Monte-Carlo sampling Methods 0.000 description 1

- 101100203187 Mus musculus Sh2d3c gene Proteins 0.000 description 1

- CBENFWSGALASAD-UHFFFAOYSA-N Ozone Chemical compound [O-][O+]=O CBENFWSGALASAD-UHFFFAOYSA-N 0.000 description 1

- 241001122315 Polites Species 0.000 description 1

- 208000001431 Psychomotor Agitation Diseases 0.000 description 1

- 206010038743 Restlessness Diseases 0.000 description 1

- 238000012896 Statistical algorithm Methods 0.000 description 1

- 235000011941 Tilia x europaea Nutrition 0.000 description 1

- 238000009825 accumulation Methods 0.000 description 1

- 238000012152 algorithmic method Methods 0.000 description 1

- 230000008485 antagonism Effects 0.000 description 1

- 230000002528 anti-freeze Effects 0.000 description 1

- QVGXLLKOCUKJST-UHFFFAOYSA-N atomic oxygen Chemical compound [O] QVGXLLKOCUKJST-UHFFFAOYSA-N 0.000 description 1

- 210000003926 auditory cortex Anatomy 0.000 description 1

- 238000013398 bayesian method Methods 0.000 description 1

- 238000005452 bending Methods 0.000 description 1

- 239000003181 biological factor Substances 0.000 description 1

- 230000008827 biological function Effects 0.000 description 1

- 230000015572 biosynthetic process Effects 0.000 description 1

- 229910021418 black silicon Inorganic materials 0.000 description 1

- 235000021152 breakfast Nutrition 0.000 description 1

- 229910002091 carbon monoxide Inorganic materials 0.000 description 1

- 230000015556 catabolic process Effects 0.000 description 1

- 230000010267 cellular communication Effects 0.000 description 1

- 238000005229 chemical vapour deposition Methods 0.000 description 1

- 238000010835 comparative analysis Methods 0.000 description 1

- 230000001010 compromised effect Effects 0.000 description 1

- 230000002596 correlated effect Effects 0.000 description 1

- 238000007418 data mining Methods 0.000 description 1

- 238000013079 data visualisation Methods 0.000 description 1

- 230000009849 deactivation Effects 0.000 description 1

- 230000034994 death Effects 0.000 description 1

- 230000002950 deficient Effects 0.000 description 1

- 238000006731 degradation reaction Methods 0.000 description 1

- 230000001934 delay Effects 0.000 description 1

- 238000000151 deposition Methods 0.000 description 1

- 230000006866 deterioration Effects 0.000 description 1

- 238000002405 diagnostic procedure Methods 0.000 description 1

- 238000005315 distribution function Methods 0.000 description 1

- 238000012553 document review Methods 0.000 description 1

- 238000003920 environmental process Methods 0.000 description 1

- 238000013213 extrapolation Methods 0.000 description 1

- 230000004424 eye movement Effects 0.000 description 1

- 230000005057 finger movement Effects 0.000 description 1

- 230000037406 food intake Effects 0.000 description 1

- 238000002599 functional magnetic resonance imaging Methods 0.000 description 1

- ZZUFCTLCJUWOSV-UHFFFAOYSA-N furosemide Chemical compound C1=C(Cl)C(S(=O)(=O)N)=CC(C(O)=O)=C1NCC1=CC=CO1 ZZUFCTLCJUWOSV-UHFFFAOYSA-N 0.000 description 1

- 239000008103 glucose Substances 0.000 description 1

- 230000012010 growth Effects 0.000 description 1

- 210000000987 immune system Anatomy 0.000 description 1

- 238000011835 investigation Methods 0.000 description 1

- JEIPFZHSYJVQDO-UHFFFAOYSA-N iron(III) oxide Inorganic materials O=[Fe]O[Fe]=O JEIPFZHSYJVQDO-UHFFFAOYSA-N 0.000 description 1

- 239000004571 lime Substances 0.000 description 1

- 238000012886 linear function Methods 0.000 description 1

- 230000006742 locomotor activity Effects 0.000 description 1

- 238000007477 logistic regression Methods 0.000 description 1

- 230000007787 long-term memory Effects 0.000 description 1

- 239000000314 lubricant Substances 0.000 description 1

- 238000002595 magnetic resonance imaging Methods 0.000 description 1

- 230000007257 malfunction Effects 0.000 description 1

- 239000003550 marker Substances 0.000 description 1

- 230000035800 maturation Effects 0.000 description 1

- 230000005055 memory storage Effects 0.000 description 1

- 230000003924 mental process Effects 0.000 description 1

- 238000002156 mixing Methods 0.000 description 1

- 238000012806 monitoring device Methods 0.000 description 1

- 230000036651 mood Effects 0.000 description 1

- 230000004973 motor coordination Effects 0.000 description 1

- 230000001423 neocortical effect Effects 0.000 description 1

- 210000005036 nerve Anatomy 0.000 description 1

- 230000007935 neutral effect Effects 0.000 description 1

- SNICXCGAKADSCV-UHFFFAOYSA-N nicotine Chemical compound CN1CCCC1C1=CC=CN=C1 SNICXCGAKADSCV-UHFFFAOYSA-N 0.000 description 1

- 210000001331 nose Anatomy 0.000 description 1

- 210000004205 output neuron Anatomy 0.000 description 1

- 238000012946 outsourcing Methods 0.000 description 1

- 229910052760 oxygen Inorganic materials 0.000 description 1

- 239000001301 oxygen Substances 0.000 description 1

- 239000005022 packaging material Substances 0.000 description 1

- 239000013618 particulate matter Substances 0.000 description 1

- 244000052769 pathogen Species 0.000 description 1

- 229940068196 placebo Drugs 0.000 description 1

- 239000000902 placebo Substances 0.000 description 1

- 238000009428 plumbing Methods 0.000 description 1

- 238000011176 pooling Methods 0.000 description 1

- 210000000977 primary visual cortex Anatomy 0.000 description 1

- 238000000513 principal component analysis Methods 0.000 description 1

- 230000000750 progressive effect Effects 0.000 description 1

- 230000035755 proliferation Effects 0.000 description 1

- 230000007363 regulatory process Effects 0.000 description 1

- 230000004043 responsiveness Effects 0.000 description 1

- 230000002207 retinal effect Effects 0.000 description 1

- 150000003839 salts Chemical class 0.000 description 1

- 239000004576 sand Substances 0.000 description 1

- 230000001953 sensory effect Effects 0.000 description 1

- 230000009919 sequestration Effects 0.000 description 1

- 239000000344 soap Substances 0.000 description 1

- 230000011273 social behavior Effects 0.000 description 1

- 230000003997 social interaction Effects 0.000 description 1

- 230000003595 spectral effect Effects 0.000 description 1

- 238000012421 spiking Methods 0.000 description 1

- 238000006467 substitution reaction Methods 0.000 description 1

- 238000013068 supply chain management Methods 0.000 description 1

- 230000003319 supportive effect Effects 0.000 description 1

- 230000009182 swimming Effects 0.000 description 1

- 210000000225 synapse Anatomy 0.000 description 1

- 230000001360 synchronised effect Effects 0.000 description 1

- 230000026676 system process Effects 0.000 description 1

- 230000008685 targeting Effects 0.000 description 1

- 238000005494 tarnishing Methods 0.000 description 1

- 238000012731 temporal analysis Methods 0.000 description 1

- 238000001931 thermography Methods 0.000 description 1

- 230000036962 time dependent Effects 0.000 description 1

- 239000003053 toxin Substances 0.000 description 1

- 231100000765 toxin Toxicity 0.000 description 1

- 108700012359 toxins Proteins 0.000 description 1

- 238000000844 transformation Methods 0.000 description 1

- 238000013519 translation Methods 0.000 description 1

- 238000001429 visible spectrum Methods 0.000 description 1

- 210000000857 visual cortex Anatomy 0.000 description 1

- 238000011179 visual inspection Methods 0.000 description 1

Images

Classifications

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q50/00—Systems or methods specially adapted for specific business sectors, e.g. utilities or tourism

- G06Q50/10—Services

- G06Q50/18—Legal services; Handling legal documents

- G06Q50/184—Intellectual property management

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06F—ELECTRIC DIGITAL DATA PROCESSING

- G06F16/00—Information retrieval; Database structures therefor; File system structures therefor

- G06F16/20—Information retrieval; Database structures therefor; File system structures therefor of structured data, e.g. relational data

- G06F16/27—Replication, distribution or synchronisation of data between databases or within a distributed database system; Distributed database system architectures therefor

- G06F16/275—Synchronous replication

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06F—ELECTRIC DIGITAL DATA PROCESSING

- G06F21/00—Security arrangements for protecting computers, components thereof, programs or data against unauthorised activity

- G06F21/10—Protecting distributed programs or content, e.g. vending or licensing of copyrighted material ; Digital rights management [DRM]

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06F—ELECTRIC DIGITAL DATA PROCESSING

- G06F21/00—Security arrangements for protecting computers, components thereof, programs or data against unauthorised activity

- G06F21/10—Protecting distributed programs or content, e.g. vending or licensing of copyrighted material ; Digital rights management [DRM]

- G06F21/12—Protecting executable software

- G06F21/121—Restricting unauthorised execution of programs

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06F—ELECTRIC DIGITAL DATA PROCESSING

- G06F21/00—Security arrangements for protecting computers, components thereof, programs or data against unauthorised activity

- G06F21/60—Protecting data

- G06F21/602—Providing cryptographic facilities or services

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06F—ELECTRIC DIGITAL DATA PROCESSING

- G06F21/00—Security arrangements for protecting computers, components thereof, programs or data against unauthorised activity

- G06F21/60—Protecting data

- G06F21/64—Protecting data integrity, e.g. using checksums, certificates or signatures

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N20/00—Machine learning

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N20/00—Machine learning

- G06N20/10—Machine learning using kernel methods, e.g. support vector machines [SVM]

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

- G06N3/043—Architecture, e.g. interconnection topology based on fuzzy logic, fuzzy membership or fuzzy inference, e.g. adaptive neuro-fuzzy inference systems [ANFIS]

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

- G06N3/044—Recurrent networks, e.g. Hopfield networks

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

- G06N3/045—Combinations of networks

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

- G06N3/047—Probabilistic or stochastic networks

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

- G06N3/048—Activation functions

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

- G06N3/049—Temporal neural networks, e.g. delay elements, oscillating neurons or pulsed inputs

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/06—Physical realisation, i.e. hardware implementation of neural networks, neurons or parts of neurons

- G06N3/063—Physical realisation, i.e. hardware implementation of neural networks, neurons or parts of neurons using electronic means

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/08—Learning methods

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/08—Learning methods

- G06N3/084—Backpropagation, e.g. using gradient descent

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/08—Learning methods

- G06N3/086—Learning methods using evolutionary algorithms, e.g. genetic algorithms or genetic programming

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/08—Learning methods

- G06N3/088—Non-supervised learning, e.g. competitive learning

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/12—Computing arrangements based on biological models using genetic models

- G06N3/126—Evolutionary algorithms, e.g. genetic algorithms or genetic programming

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N7/00—Computing arrangements based on specific mathematical models

- G06N7/01—Probabilistic graphical models, e.g. probabilistic networks

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/02—Payment architectures, schemes or protocols involving a neutral party, e.g. certification authority, notary or trusted third party [TTP]

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/04—Payment circuits

- G06Q20/06—Private payment circuits, e.g. involving electronic currency used among participants of a common payment scheme

- G06Q20/065—Private payment circuits, e.g. involving electronic currency used among participants of a common payment scheme using e-cash

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/22—Payment schemes or models

- G06Q20/223—Payment schemes or models based on the use of peer-to-peer networks

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/30—Payment architectures, schemes or protocols characterised by the use of specific devices or networks

- G06Q20/36—Payment architectures, schemes or protocols characterised by the use of specific devices or networks using electronic wallets or electronic money safes

- G06Q20/367—Payment architectures, schemes or protocols characterised by the use of specific devices or networks using electronic wallets or electronic money safes involving electronic purses or money safes

- G06Q20/3678—Payment architectures, schemes or protocols characterised by the use of specific devices or networks using electronic wallets or electronic money safes involving electronic purses or money safes e-cash details, e.g. blinded, divisible or detecting double spending

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/382—Payment protocols; Details thereof insuring higher security of transaction

- G06Q20/3827—Use of message hashing

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/382—Payment protocols; Details thereof insuring higher security of transaction

- G06Q20/3829—Payment protocols; Details thereof insuring higher security of transaction involving key management

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/389—Keeping log of transactions for guaranteeing non-repudiation of a transaction

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/40—Authorisation, e.g. identification of payer or payee, verification of customer or shop credentials; Review and approval of payers, e.g. check credit lines or negative lists

- G06Q20/401—Transaction verification

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

- G06Q20/38—Payment protocols; Details thereof

- G06Q20/40—Authorisation, e.g. identification of payer or payee, verification of customer or shop credentials; Review and approval of payers, e.g. check credit lines or negative lists

- G06Q20/401—Transaction verification

- G06Q20/4016—Transaction verification involving fraud or risk level assessment in transaction processing

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N20/00—Machine learning

- G06N20/20—Ensemble learning

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

- G06N3/042—Knowledge-based neural networks; Logical representations of neural networks

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N3/00—Computing arrangements based on biological models

- G06N3/02—Neural networks

- G06N3/04—Architecture, e.g. interconnection topology

- G06N3/0463—Neocognitrons

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N5/00—Computing arrangements using knowledge-based models

- G06N5/01—Dynamic search techniques; Heuristics; Dynamic trees; Branch-and-bound

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N5/00—Computing arrangements using knowledge-based models

- G06N5/02—Knowledge representation; Symbolic representation

- G06N5/022—Knowledge engineering; Knowledge acquisition

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N5/00—Computing arrangements using knowledge-based models

- G06N5/02—Knowledge representation; Symbolic representation

- G06N5/022—Knowledge engineering; Knowledge acquisition

- G06N5/025—Extracting rules from data

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N5/00—Computing arrangements using knowledge-based models

- G06N5/04—Inference or reasoning models

- G06N5/045—Explanation of inference; Explainable artificial intelligence [XAI]; Interpretable artificial intelligence

-

- G—PHYSICS

- G06—COMPUTING; CALCULATING OR COUNTING

- G06N—COMPUTING ARRANGEMENTS BASED ON SPECIFIC COMPUTATIONAL MODELS

- G06N7/00—Computing arrangements based on specific mathematical models

- G06N7/02—Computing arrangements based on specific mathematical models using fuzzy logic

-

- H—ELECTRICITY

- H04—ELECTRIC COMMUNICATION TECHNIQUE

- H04L—TRANSMISSION OF DIGITAL INFORMATION, e.g. TELEGRAPHIC COMMUNICATION

- H04L2209/00—Additional information or applications relating to cryptographic mechanisms or cryptographic arrangements for secret or secure communication H04L9/00

- H04L2209/60—Digital content management, e.g. content distribution

-

- H—ELECTRICITY

- H04—ELECTRIC COMMUNICATION TECHNIQUE

- H04L—TRANSMISSION OF DIGITAL INFORMATION, e.g. TELEGRAPHIC COMMUNICATION

- H04L9/00—Cryptographic mechanisms or cryptographic arrangements for secret or secure communications; Network security protocols

- H04L9/50—Cryptographic mechanisms or cryptographic arrangements for secret or secure communications; Network security protocols using hash chains, e.g. blockchains or hash trees

-

- Y—GENERAL TAGGING OF NEW TECHNOLOGICAL DEVELOPMENTS; GENERAL TAGGING OF CROSS-SECTIONAL TECHNOLOGIES SPANNING OVER SEVERAL SECTIONS OF THE IPC; TECHNICAL SUBJECTS COVERED BY FORMER USPC CROSS-REFERENCE ART COLLECTIONS [XRACs] AND DIGESTS

- Y02—TECHNOLOGIES OR APPLICATIONS FOR MITIGATION OR ADAPTATION AGAINST CLIMATE CHANGE

- Y02P—CLIMATE CHANGE MITIGATION TECHNOLOGIES IN THE PRODUCTION OR PROCESSING OF GOODS

- Y02P90/00—Enabling technologies with a potential contribution to greenhouse gas [GHG] emissions mitigation

- Y02P90/30—Computing systems specially adapted for manufacturing

Abstract

Systems and methods for controlling digital knowledge related rights are disclosed. The sample system may comprise: an input system for receiving digital knowledge from a user; a tagging system for tagging the digital knowledge; ledger management systems for creating, managing and storing things on distributed ledgers and providing provable access to the digital knowledge. The smart contract system may create a smart contract that includes a trigger action and respond with a defined smart contract action when the trigger event occurs. The smart contract system may also process commitments to the smart contract.

Description

Cross reference

This application claims the benefit of priority from the following U.S. provisional patent application: U.S. provisional patent application No. 63/052,475 (attorney docket No. SFTX-0018-P01), filed on 7/16 in 2020, entitled "system and method for controlling digital knowledge related rights"; U.S. provisional patent application No. 63/054,603 (attorney docket No. SFTX-0017-P02) filed on day 21 of 7 in 2020 entitled "digital twin systems and methods for financial systems"; U.S. provisional patent application No. 63/127,980 (attorney docket SFTX-0016-P01), entitled "market orchestration system for facilitating electronic market transactions", filed on 12 months 18 in 2020.

The above applications are each incorporated by reference in their entirety.

Background

A large amount of information is periodically exchanged digitally and the amount of information is increasing. Such information may include valuable and sensitive information such as trade secrets, proprietary technology, proprietary materials, and author works. Some information is limited in access and control, such as limitations on who can view, edit, alter, use, transmit, sell, purchase, rent, review, license, and acquire digital information (e.g., with respect to patent permissions, trademark permissions, contractual agreements, copyright permissions, etc.). Setting and enforcing access and control restrictions is difficult because any computer-based system used to perform this transaction presents potential drawbacks, such as the risk of improper or unreliable system owners or maintainers, or the risk of other parties gaining unauthorized access and illegal access, copying, editing, or otherwise tampering with the digital knowledge.

The lending transaction provides financing for housing and education to various needs such as corporate and government projects, while enabling the borrower to obtain financial benefits. However, lending transactions suffer from a number of problems including opacity and asymmetry of the information, moral risk due to the transfer of risk or consequences of improper behavior, complexity of the application and negotiation process, heavy regulatory and policy regimes, difficulty in determining the value of the property being used as a mortgage or debt guarantee, difficulty in determining the reliability or financial health of the entity, and so forth.

Machines and automated agents are increasingly being used for marketing activities, including data collection, forecasting, planning, transactional execution, and other activities. This includes increasingly higher performance systems, such as those used for high speed transactions. There is a need for methods and systems that can improve machines capable of markets, including improving efficiency, speed, reliability, etc. for participants in such markets.

Many markets are becoming more and more decentralized, rather than more and more focused, distributed ledgers (e.g., blockchains), point-to-point interaction models, and microtransactions replace or supplement traditional models involving centralized or intermediaries. There is a need for an improved machine that enables large numbers of participants (including human participants and automated agents) to conduct decentralized transactions on a large scale.

Operations on blockchains (e.g., operations using cryptocurrency) increasingly require energy intensive computing operations, such as computing very large hash functions on ever-growing blockchains. Systems using work certificates, equity certificates, etc., have resulted in "mining" operations by which computer processing power is applied on a large scale to perform calculations that support collective trust for transactions recorded in blockchains.

Many applications of artificial intelligence also require energy intensive computing operations, such as very large neural networks with very many interconnections to perform operations on a large number of inputs to produce one or more outputs, such as prediction, classification, optimization, control outputs, and so forth.

The growth of internet of things and cloud computing platforms has also led to a proliferation of devices, applications, and connections between them, such that data centers, house servers, and other IT components consume a significant portion of the energy consumption in the united states and other developed countries.

As a result of these trends and other trends, energy consumption has become a major factor in computing resource utilization, such that energy resources and computing resources (or simply "energy and computing") have begun to merge from various perspectives, such as applications, purchases, supplies, configurations, and management of inputs, activities, outputs, and the like. For example, projects have been developed to host large computing resource facilities (e.g., bitlock TM Or other cryptocurrency mining operations) are placed near large hydroelectric resources such as the niagara waterfall.

The main challenges faced by the owners and operators of the facilities are the uncertainties involved in optimizing the facilities, such as due to fluctuations in the cost and availability of inputs (especially in the case of less stable renewable resources), fluctuations in the cost and availability of computing and network resources (e.g. in the case of network performance variations) and fluctuations and uncertainties of the various end markets in which energy and computing resources can be applied (e.g. fluctuations in cryptocurrency, fluctuations in energy markets, fluctuations in various other market pricing and uncertainties in the utility of artificial intelligence in a wide range of applications), among other factors.

Disclosure of Invention

The exemplary embodiments herein disclose systems, processes, and aspects for providing an encrypted secure blockchain for a knowledge system capable of storing digital knowledge to provide convenient, secure control of the knowledge system. The example methods and systems herein provide improvements in determining property valuations, reliability of physical financial health, transparency, information symmetry, and application and negotiation processes in a lending environment. The example methods and systems herein provide improvements to machines that enable markets that provide greater efficiency, speed, and/or reliability to participants in such markets. The example methods and systems herein provide improvements to automated configuration of data collection, storage and processing, input, resources, and output, and methods for facility optimization of energy and computing facilities.

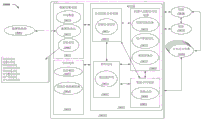

In one or more exemplary embodiments, a knowledge distribution system for controlling digital knowledge-related rights is disclosed. The knowledge distribution system may be a blockchain for a knowledge system that allows for storing digital knowledge, purchasing or selling digital knowledge, tagging digital knowledge, and/or auditing/auditing the digital knowledge by cryptographically secure distributed ledgers. The intelligent contract may be implemented by the distributed ledger to control rights to digital knowledge, transfer digital knowledge, and to enable parties to adhere to agreements related to the digital knowledge. The knowledge system blockchain may also facilitate third parties to review, audit, or verify information related to digital knowledge.

There may be many practical barriers to knowledge sharing, such as lack of trust between parties that may benefit from knowledge sharing. There are platforms for digital knowledge distribution systems that facilitate orchestration of the sharing of knowledge by providing a high degree of control over the extent to which a transacting adversary has access to the shared knowledge. Even with knowledge security and good control, certain types of knowledge are so sensitive that owners may be reluctant to share the entire knowledge set with a single adversary. In an embodiment, a platform for a digital knowledge distribution system is disclosed that facilitates processing and controlling knowledge subsets, including automatically processing knowledge aggregation or related output due to knowledge subset partitioning.

The knowledge distribution system may include a ledger management system for creating and managing distributed ledgers, which may be distributed over nodes of a network and may include blocks linked by encryption. An intelligent contract system may be in communication with the distributed ledger and may be used to implement and manage intelligent contracts with the distributed ledger. The smart contract may be stored in the distributed ledger and may include a trigger event. The smart contract may be configured to perform a smart contract action with respect to the digital knowledge in response to the occurrence of the trigger event. The knowledge distribution system may be configured to receive an instance of the digital knowledge from a user. The digital knowledge may be tagged such that the instance of the digital knowledge operates as a tag on the distributed ledger. The tagged digital knowledge may be stored by the distributed ledger. The commitments of the parties to the smart contract may be processed. The knowledge distribution system may be configured to: managing control and access rights to the marked digital knowledge according to the intelligent contract; and managing the smart contract actions in response to the trigger event.

One or more of the following exemplary features may be included. The digital intellectual property may include intellectual property, where the smart contract embeds intellectual property licensing terms for the intellectual property embedded in the distributed ledger, and performing operations on the distributed ledger may provide access to the intellectual property, and may also handle commitments of parties to the smart contract to the intellectual property licensing terms. An intelligent contract wrapper on the distributed ledger may allow operations to be performed on the ledger to add intellectual property to an intellectual property aggregation stack; an operation may be allowed to be performed on the ledger to add intellectual property rights to agree to apportion licensing fees among the parties in the ledger; operations may be allowed to be performed on the ledger to add intellectual property to an intellectual property aggregation stack; and/or may allow operations to be performed on the ledger to handle commitments of the principal to the terms of the agreement. The digital knowledge of the tag may include an instruction set. The distributed ledger may be used to provide provable access to the instruction set and execute the instruction set on a system to record transactions in the distributed ledger. The digital knowledge of the tag may include executable algorithm logic, a three-dimensional (3D) printer instruction set, an instruction set for a coating process, an instruction set for a semiconductor manufacturing process, a firmware program, an instruction set for a field programmable gate array, server-less code logic, an instruction set for a crystal manufacturing system, an instruction set for a food preparation process, an instruction set for a polymer production process, an instruction set for a chemical synthesis process, an instruction set for a bio-production process, a data set for digital twinning, and/or a business secret with an expert wrapper. The system may be used to aggregate views of trade secrets into a chain that proves which knowledge recipients of the principal have viewed the trade secrets. The knowledge distribution system may include a reporting system for reporting analysis results based on operations performed on the distributed ledgers or the digital knowledge. The distributed ledger may be used to aggregate instruction sets, wherein performing operations on the distributed ledger may add at least one instruction to a pre-existing instruction set to provide a modified instruction set. The smart contract may be used to manage allocation of a subset of instructions to the distributed ledger and access to the subset of instructions. The distributed ledger may be used to record principals contributing to the instance of digital knowledge by storing data related to the principals in at least one of the blocks. The knowledge distribution system may be configured to record a source of the instance of digital knowledge by storing data related to the source in at least one of the blocks. The distributed ledger may be configured to enable a private network of authorized participants to establish encryption-based consensus requirements to verify new ones of the blocks to be added. The ledger administration system may be used to facilitate crowdsourcing of information added to one of the blocks of the distributed ledger. The distributed ledger may be used to store a crowd-sourced review of instances of the digital knowledge in one of the blocks. The distributed ledger may be used to store a signature of an instance of the digital knowledge by a crowdsourcer in one of the blocks. The distributed ledger may be used to store a verification of an instance of the digital knowledge by a crowdsourcer in one of the blocks. The ledger administration system may be used to establish cryptocurrency tokens that may be transacted between users of the distributed ledger. The knowledge distribution system may include an account management system in communication with the distributed ledger, which may be used to facilitate creation and management of user accounts related to users of the knowledge distribution system. The knowledge distribution system may include a user interface system in communication with the distributed ledger, which may be used to present a user interface to a user of the knowledge distribution system, wherein the user interface allows the user to view data related to an instance of the digital knowledge. The knowledge distribution system may include a marketplace system in communication with the distributed ledger, the marketplace system may be operable to establish and maintain a digital marketplace that may be operable to visually present data related to instances of the digital knowledge to users of the knowledge distribution system. The knowledge distribution system may include a knowledge data store in communication with the distributed ledger, which may be used to store data related to the digital knowledge. The knowledge distribution system may include a client data store in communication with the distributed ledger, which may be used to store data related to users of the knowledge distribution system. The knowledge distribution system may include a smart contract data store in communication with the distributed ledger, which may be used to store data related to the smart contract. The knowledge distribution system may include a reporting system in communication with the distributed ledger, the reporting system operable to analyze the tagged digital knowledge and report analysis results based on the analysis of the tagged digital knowledge. The smart contracts may be generated using parameterizable smart contract templates. The smart contract may include parameters based on the type of digital knowledge to be tagged. The parameters may include financial parameters, license fee parameters, usage parameters, yield parameters, price allocation parameters, identity parameters, and/or access condition parameters.

In other exemplary embodiments, the knowledge distribution system may use distributed ledgers and intelligent contracts to facilitate the management and exchange of access, permissions, and ownership of digital knowledge.

In other exemplary embodiments, a computer-implemented method for controlling digital knowledge-related rights is disclosed. The method may include: a distributed ledger is created and managed, which is distributed over nodes of the network and comprises blocks linked by encryption. A smart contract may be implemented and managed by the distributed ledger, wherein the smart contract may be stored in the distributed ledger and may include a trigger event. An intelligent contract action may be performed with respect to the digital knowledge in response to the occurrence of the trigger event. An instance of the digital knowledge may be received. The digital knowledge may be tagged such that the instance of the digital knowledge operates as a tag on the distributed ledger. The tagged digital knowledge may be stored by the distributed ledger. The commitments of the parties to the smart contract may be processed. The method may include: managing control and access rights to the marked digital knowledge according to the intelligent contract; and managing the smart contract actions in response to the trigger event.

One or more of the following exemplary features may be included. Knowledge exchange for exchanging digital knowledge of the tags based on the smart contracts may be orchestrated. The knowledge exchange of the tagged digital knowledge may be integrated with another exchange, wherein the knowledge exchange facilitates an exchange of valuable and/or sensitive knowledge related to the subject matter of the other exchange.

In other exemplary embodiments, a knowledge distribution system for controlling digital knowledge-related rights is disclosed. The knowledge distribution system may include a ledger management system for creating and managing distributed ledgers. The distributed ledger may be distributed over nodes of a network and may include blocks linked by encryption. An intelligent contract system may be in communication with the distributed ledger and may be used to implement and manage intelligent contracts with the distributed ledger. The smart contract may be stored in the distributed ledger and may include a trigger event. The smart contract may be configured to perform a smart contract action with respect to the digital knowledge in response to the occurrence of the trigger event. The knowledge distribution system may be configured to receive an instance of the digital knowledge from a knowledge provider device, the instance of the digital knowledge including a 3D printer instruction set for a three-dimensional (3D) print object. The digital knowledge may be tagged such that the instance of the digital knowledge operates as a tag on the distributed ledger. The tagged digital knowledge may be stored by the distributed ledger. The commitments of the knowledge provider and knowledge receiver of the 3D printer instruction set to the smart contract may be processed. The knowledge distribution system may be configured to: managing control and access rights to the marked digital knowledge according to the intelligent contract; and managing the smart contract actions based on the conditions and the trigger event.

One or more of the following exemplary features may be included. The 3D printer instruction set may include a 3D print schematic. The object may be at least one of a custom part, a custom product, a manufactured part, a replacement part, a toy, a medical device, and a tool. The knowledge receiver may download and use the 3D printer instruction set using a knowledge receiver device. The knowledge receiver device may be at least one of a computing device, a server, a 3D printer, and a manufacturing device. The knowledge receiver may purchase digital knowledge of the tag corresponding to the 3D printer instruction set using a knowledge receiver device. The knowledge distribution system may include an event listener for listening to an Application Programming Interface (API) that may provide a connection between the knowledge distribution system and a knowledge receiver device of the knowledge receiver. The smart contract may be to: when the 3D printer instruction set can transfer or use the control rights and the access rights based on the digital knowledge of the tag, a condition for payment by the knowledge recipient is triggered. The controlling of the digital knowledge of the tag and the accessing may include allowing a user to 3D print using multiple instances of the 3D printer instruction set. The control rights and the access rights to the marked digital knowledge may comprise at least one of: the 3D printer requires, the period of time that the object can be 3D printed, whether the marked digital knowledge is transferred to a downstream knowledge receiver, assurance, disclaimer, reimbursement, and authentication with respect to the object. When the 3D printer instruction set is subjected to at least one of purchasing, downloading, and using, information related to the 3D printer instruction set of the marked digital knowledge may be modified on the distributed ledger. In an example, the information related to the 3D printer instruction set may include at least one of: sources, creation dates, names of one or more contributing individuals, groups, and/or companies, pricing, market trends for related schematics, serial numbers, and component identifiers. The smart contract action may be one of: assigning a serial number to the 3D printed object; monitoring the trigger event; verifying performance of the obligation based on the condition; verifying payment and/or transfer of the marked digital knowledge; transferring the digital knowledge of the tag; recording one or more transactions in the distributed ledger; performing one or more operations on the distributed ledger; and creating one or more new blocks in the distributed ledger. The smart contract action may include verifying that the condition defined in the smart contract is satisfied, wherein the condition may be one of: printer requirements, money for payment or transfer received from the knowledge receiver device of the knowledge receiver and transferring the marked digital knowledge to the knowledge receiver device. When the marked digital knowledge can be transferred to a knowledge receiver device of a knowledge receiver, a 3D printer can be used to print the object according to the 3D printer instruction set. The knowledge distribution system may include an intelligent contract generator that may be used to parameterize an intelligent contract template based on at least one of the knowledge provider provided information, the conditions, and the triggering event.

In other exemplary embodiments, a computer-implemented method for controlling digital knowledge-related rights is disclosed. The method may include: a distributed ledger is created and managed, which is distributed over nodes of the network and comprises blocks linked by encryption. A smart contract may be implemented and managed by the distributed ledger, wherein the smart contract may be stored in the distributed ledger and may include a trigger event. An intelligent contract action may be performed with respect to the digital knowledge in response to the occurrence of the trigger event. The method may include: an instance of the digital knowledge is received from a knowledge provider device, the instance of the digital knowledge including a 3D printer instruction set for a three-dimensional (3D) print object. The digital knowledge may be tagged such that the instance of the digital knowledge operates as a tag on the distributed ledger. The tagged digital knowledge may be stored by the distributed ledger. The commitments of the knowledge provider and knowledge receiver of the 3D printer instruction set to the smart contract may be processed. The method may include: managing control and access rights to the marked digital knowledge according to the intelligent contract; and managing the smart contract actions based on the conditions and the trigger event.

One or more of the following exemplary features may be included. Elements of the instance of the digital knowledge may be crowd-sourced through the smart contract. The elements of the instance of the digital knowledge may be managed by a smart contract system according to the smart contract.

A lending transaction support platform is provided having a set of data-integrated micro services including data collection and monitoring services, blockchain services, and smart contract services for processing lending entities and transactions. The platform enables a wide range of proprietary solutions that can share data collection and storage infrastructure and can share or exchange inputs, events, activities, and outputs to enhance learning, enable automation, and enable adaptive intelligence among various solutions.

Aspects of the present invention relate to a method for electronically facilitating one or more personality rights of a licensing party. The method may include receiving an access request from a licensee to obtain approval of a licensing personality right from a set of available licensees. The method may include selectively granting access to the licensee based on the access request. The method may include receiving a deposit confirmation of the funds amount from the licensee. The method may include issuing an encrypted monetary amount corresponding to the amount of funds deposited by the licensee to an account of the licensee. The method may include receiving a smart contract request to create a smart contract that manages permissions of the licensee for the one or more personals of the licensee. The smart contract request may indicate one or more terms including a crypto-currency value amount to be paid to the licensor in exchange for one or more obligations of the licensor. The method may include generating the smart contract based on the smart contract request. The method may include hosting the cryptocurrency value amount from the account of the licensee. The method may include deploying the smart contract to a distributed ledger. The method may include verifying, by the smart contract, that the licensor has fulfilled the one or more obligations. The method may include releasing at least a portion of the cryptocurrency amount into a licensor account of the licensor in response to receiving verification that the licensor has fulfilled the one or more obligations. The method may include outputting a record to the distributed ledger, the record indicating that a license transaction defined by the smart contract has been completed.