USRE44738E1 - Seller automated engine architecture and methodology for optimized pricing strategies in automated real-time iterative reverse auctions over the internet and the like for the purchase and sale of goods and services - Google Patents

Seller automated engine architecture and methodology for optimized pricing strategies in automated real-time iterative reverse auctions over the internet and the like for the purchase and sale of goods and services Download PDFInfo

- Publication number

- USRE44738E1 USRE44738E1 US13/762,485 US201313762485A USRE44738E US RE44738 E1 USRE44738 E1 US RE44738E1 US 201313762485 A US201313762485 A US 201313762485A US RE44738 E USRE44738 E US RE44738E

- Authority

- US

- United States

- Prior art keywords

- price

- seller

- implementation

- market

- target

- Prior art date

- Legal status (The legal status is an assumption and is not a legal conclusion. Google has not performed a legal analysis and makes no representation as to the accuracy of the status listed.)

- Active, expires

Links

Images

Classifications

-

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q30/00—Commerce

- G06Q30/06—Buying, selling or leasing transactions

-

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q30/00—Commerce

- G06Q30/02—Marketing; Price estimation or determination; Fundraising

- G06Q30/0201—Market modelling; Market analysis; Collecting market data

- G06Q30/0206—Price or cost determination based on market factors

-

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q30/00—Commerce

- G06Q30/02—Marketing; Price estimation or determination; Fundraising

- G06Q30/0283—Price estimation or determination

-

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q30/00—Commerce

- G06Q30/06—Buying, selling or leasing transactions

- G06Q30/08—Auctions

-

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q40/00—Finance; Insurance; Tax strategies; Processing of corporate or income taxes

- G06Q40/03—Credit; Loans; Processing thereof

-

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q40/00—Finance; Insurance; Tax strategies; Processing of corporate or income taxes

- G06Q40/04—Trading; Exchange, e.g. stocks, commodities, derivatives or currency exchange

Definitions

- the present invention relates broadly to the field of on-line shopping for products and services over the Internet, the term “Internet” being used herein to embrace generically all types of public and/or private communication networks using wireless and/or wired transmission media, and combinations of the above, and also, specifically the satellite world wide web. More particularly, the invention is concerned with electronic transactions with price-comparison features, being more directly concerned with buyer-seller real-time iterative bidding and offering, in close simulation of the mechanisms of real marketplace auctions and further enhancements for the benefit of both buyer and seller interests.

- the more particular, though not exclusive, field herein embraced involves improvements in the approach described and claimed in our earlier co-pending U.S. patent application, Ser. No. 11/367,907, filed Mar.

- This [ARTIST] approach involves an automated real-time iterative reverse auction system and mechanism consisting basically of a buyer system component (BS), a reverse auctioneer controller component (RAC), and a seller automated engine component (SAEJ)—the present invention being particularly concerned with improvements in the implementation of the SAEJ, and with the said co-pending application describing in detail, the overall architecture of each component, including that of the SAEJ, generally.

- the present invention in its thrust toward improved seller automated engines, offers a number of novel implementations of such seller automated engine architectures that can achieve and optimize the seller pricing and goals of the before-mentioned [ARTIST] system of said co-pending application.

- the challenges and questions include generally how to access a larger addressable market without spending large sums in advertising, man power and capital expenditure.

- Important further questions, among others, include how to price, what to price and when to update the price; how automatically to compute an optimal price in real-time in automatic reverse auctions; and how iteratively to bid so as to sell the product at the optimal price.

- a seller works with a number of interacting variables typically including: revenue target, profit target, market share target and others over specified intervals; inventory status in case of retail; volume discount rates from its own suppliers, promotion events timing and magnitude; inherently inaccurate pricing forecasts derived from historic market data; competitive forces impacting the current market; management of conflicting targets as a function of time; volume discount strategy; and others.

- These interactive variables largely interdependent, and at times in conflict, are either assigned by the seller, such as targets, or they assume a wide range of values driven by the dynamics of market conditions. The result is massive variation in the choices to be made as the seller attempts to find an optimum pricing strategy specific to its constraints to meet its assigned targets.

- Risk tolerance of the decision maker at the seller plays an important role in establishing the targets and other value assignments to the variables and is typically subject to his/her own financials, perceived reputation, age, and views on both short and long term economic outlook. Risk tolerance is also a function of the benefits a decision maker may derive from the type of equity structure, ranging from private, or preparing to go public, or public, or in the process of going from public to private. In aggregate, these and other human factors considerably influence seller pricing strategies, ranging from very defensive to highly aggressive and in between.

- a retailer will typically work with the above-mentioned type of variables, There are also corresponding variables in service institutions such as banking and the like, which may include, for example, multiple deposit targets, corresponding CD durations, times in which these deposit targets must respectively be met, the maximum payable interest rate, the desired blended interest rate, the desired spread with respect to a benchmark or lending rate, the historic and current interest rates, the types of benchmarks, and so on.

- service institutions such as banking and the like, which may include, for example, multiple deposit targets, corresponding CD durations, times in which these deposit targets must respectively be met, the maximum payable interest rate, the desired blended interest rate, the desired spread with respect to a benchmark or lending rate, the historic and current interest rates, the types of benchmarks, and so on.

- each seller defines its unique targets for revenue, profit, growth, and market share, etc. Some sellers track sales and other variables on a daily basis; some weekly; others, monthly or quarterly and some combination of the above. If a target is missed, some move the difference to the immediate next time slot; others distribute it equally over multiple times slots; and yet, some distribute it unequally across multiple time slots to match the customer buying patterns. Some choose to do nothing at all, and some do not have the luxury to go to the next time slot—for example, in the last quarter of the year. The seller thus has to make very many hopefully correct choices as a function of time for each product or service in its portfolio to derive an optimum price as it races to meet its targets.

- Tight inventory management is one of the most critical functions for a large number of retailers, whereas some sellers inventories are largely time insensitive variation; for example, a diamond seller.

- these rapidly changing conditions force a seller to shift relative degrees of emphasis among targets—for example, from profit to revenue, to inventory, to market share and then back to revenue and profit, and then perhaps back to market share, or any combinations thereof—all in the same quarter, and all highly subjective to estimation errors. This often results in highly sub-optimal seller pricing decisions at large variance with the market, and in the inability simultaneously to meet the targets.

- Sellers who have met their revenue target earlier in the quarter than anticipated may choose to slow down to keep the quarterly revenue smooth and predictable; whereas others may choose to be more aggressive for the rest of the quarter and may even accelerate to substantially enhance the profit while the overheads remain largely the same.

- Yet another important variable distorting the historic data is the advent of asynchronous and potentially non-repetitive promotions from competitors at that time. Some sellers are less impacted by seasonal effects and depend more on supply and demand, such as seller of a “hot” new video game or a much anticipated toy, that may distort the historic data of the past. There is, thus, highly questionable repeatability of historic data, particularly as further distorted by current market conditions, which will significantly increase the standard deviation of pricing forecast models. Generally, however, relative qualitative demand data tends to be more reliable, such as retail sales from Monday to Thursday being less than Friday, Saturday, and Sunday, thus providing an insight into relative arrival rate.

- Another challenge faced by sellers is the decision of when to run a promotion independent of, and at times in anticipation of, competitive promotions. These events are typically planned months in advance. Frequently, a seller is unaware of either timing or intention (e.g. a competitor wanting to drastically reduce inventory), or the intensity of a competitor's promotion, and the seller will therefore find it difficult to respond in a timely manner. Manual tracking of promotions run by hundreds or thousands of sellers, especially on-line, moreover, is a difficult if not impossible task. A seller, furthermore, sometimes may not want to respond to every promotion and may typically respond only to sellers of its own class and geographical proximity; for example, a large department store will generally only respond to another similar store, but not to a small player.

- a reverse auction controller receives buyer requests and solicits iterative bids from sellers equipped with seller automated engines (SAEJ) that respond to each iterative bid request (as part of an auction) in real-time with the optimal price available from the seller at that instant.

- SAEJ seller automated engine

- the seller automated engine not only provides the buyer with its best price, but also optimizes the price based on the seller's objectives.

- SAEJ A generic automated seller engine that enables the addressing of many of these challenges and without manual intervention, is described in said co-pending [ARTIST] application and is also summarized herein; disclosing how automatically to track competitive pricing; how to be agile in responding to changing market conditions; how to set sales targets (using revenue, profit margin, sales volume and other similar metrics); how to manage inventory efficiently; and how optimally to manage product pricing to maximize the likelihood of reaching the sales targets; how to maintain and increase market share in a highly competitive environment; how to create promotions and inject promotions instantaneously, based on currently occurring, real-time, market and internal conditions, to a large and targeted set of customers, based on demographics or other criteria; how to trigger higher sales to achieve a volume-based incentive from suppliers, manufacturers of the product or a part of the product; how dynamically to adjust sales from multiple channels by using current market conditions on each sales channel to trigger pricing changes and promotion events that are specific to channels/markets; how dynamically to adjust pricing of well-performing products to compensate for another unrelated under-performing product, thus

- the invention addresses how to achieve all of the above goals simultaneously without manual intervention each time the price has to be adjusted to achieve the goals in the presence of dynamically changing market conditions; also how to achieve all of the above goals simultaneously without waiting for offline tools to gather market data and adjust pricing subject to high estimation errors over the period of a week or month or more; and how to achieve the above goals simultaneously without being required to predict future market conditions—indeed, achieving the above goals simultaneously by changing pricing in real-time.

- the [ARTIST] concept provides an effective method of communications-network shopping by buyers of products and services for purchasing such from sellers, wherein buyers request the automatic reverse auctioneer or auction controller (RAC) to initiate a reverse auction in real time amongst willing sellers and to solicit from their automated seller engines (SAEJ) their automatic real-time iterative bidding price quotations for such products and services, to be returned automatically over the network back to the controller under the iterative processing guidance of the controller to assure a best bid price quotation for the buyer; and automatically effecting buyer notification or purchase at such best price, all even while the buyer may remain on-line, and without any manual intervention.

- RAC automatic reverse auctioneer or auction controller

- SAEJ automated seller engines

- the present invention now further provides such [ARTIST] systems, among others, with automatic seller optimization techniques and with a choice of options for improved automated seller engine architecture implementations depending upon the particular application involved.

- the architecture has multiple possible implementations that include a parallel processing architecture, or a pipeline architecture, or a hub and spoke model, or also a hybrid combination of the above, as later explained in detail.

- the core idea is to implement a price management unit that is responsible for receiving requests from the controller (RAC) for one or more items that the buyer expresses interest in buying.

- the price management unit optimizes the price for the business objectives of the seller.

- the present invention provides several specific implementations of how automatically to optimize the price, (1) for specific target-directed implementations, (2) for market-share directed implementations, (3) for a hereinafter described utility derivative-following implementation, and (4) for a model optimizer implementation.

- the invention provides for novel mathematical optimization-oriented implementation more generally.

- the price management unit furthermore, can also use a more conventional rules-based implementation, as also later described.

- a primary object of the invention accordingly, is to provide for the introduction and implementation of a novel price management and seller price optimizing system in the [ARTIST] type method and system of said co-pending application, and similar systems, enabling automatic real-time iterative commercial transactions over the Internet in a multiple-buyer, multiple-seller marketplace, while automatically optimizing both buyer and seller needs based upon the dynamics of market conditions and the seller's inputted business objectives, and constraints, as the price management unit receives requests from an auction controller for pricing bids on items that the buyer may request.

- a further object is to provide price-optimizing novel seller automated engine architectural implementations for use in such and related systems.

- An additional object is to provide a more general automated novel method and engine for price management by select and novel mathematical and physical implementations for optimizing seller price bids under changing market conditions in real time.

- Another object is to provide automatic pricing and optimizing features across a wide range of verticals in widely varying businesses ranging from retail products to banking and insurance services, among others.

- the invention provides a method of communications-network shopping by buyers of products and services for purchasing such from sellers, wherein buyers request an automatic reverse auctioneer or auction controller (RAC) to initiate a reverse auction in real time amongst willing sellers and to solicit from automated seller engines (SAEJ) of the sellers their automatic real-time iterative bidding price quotations for such products and services, to be returned automatically over the network back to the controller without any manual intervention and under the iterative processing guidance of the controller to assure a best bid price quotation for the buyer;

- RAC automatic reverse auctioneer or auction controller

- SAEJ automated seller engines

- the methodology underlying the invention can be implemented in a system for conducting real-time commercial transactions between buyers and sellers of products and services through an intermediate reverse auctioneer controller communicating on-line with both buyer and seller over the Internet, and providing on-line buyer requests for seller price quotations, and for thereupon communicating the same over the Internet to sellers;

- each seller being equipped with a seller automatic engine storing that seller's specific predetermined business objectives and market condition information and responsive to the buyer requests in order automatically to create and to respond to the controller with a price quotation based upon the buyer request and within the respective guidelines of seller-specific predetermined information stored in that seller's automatic seller engine;

- a processor for processing the price quotations received back over the Internet from the seller automatic engines to initiate an iterative real-time automatic seller engine competitive bettering of the price quotations within said respective guidelines, until a best price quotation is received, for thereupon enabling the automatic notifying of, or purchasing by, the buyer at such best price quotation;

- the seller automatic engines being adapted to use a choice of architectural price optimizing implementation selected from the group consisting of a parallel processing architecture, a pipeline architecture, a hub and spoke architecture, and a hybrid combination thereof.

- the price optimizing techniques of the invention and the mathematical basis therefor are also useable in other than reverse auction applications, and they find particular usefulness in the automatic pricing of services and products and bundling of the same in the banking, insurance and similar service institutions, as later more fully addressed.

- FIG. 1 is an overall high level block system diagram of a generic seller-automated engine implementation architecture referred to by the previously mentioned acronym “SAEJ”; for use preferably and particularly, though not exclusively, in the [ARTIST] type system of said co-pending application;

- SAEJ seller-automated engine implementation architecture

- FIG. 2 is a similar flow diagram generically illustrating various types of price optimizers for SAEJ price management units (PMU) of the invention

- FIG. 3 is a more detailed block diagram of a Price Management Unit (PMU) of the SAEJ, using a parallel architecture implementation;

- PMU Price Management Unit

- FIGS. 4 and 5 are similar diagrams illustrating pipelined and hub and spoke architecture PMU implementations, respectively;

- FIG. 6 illustrates a hybrid type PMU architecture

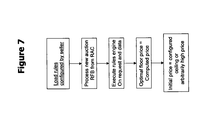

- FIG. 7 is a flow chart diagram of a illustrative rules-based implementation

- FIGS. 8 , 9 (a), 9 (b), 10 (a) and 10 (b) are graphs of illustrative utility curves—linear, piecewise linear, and exponential, respectively,—useful with the invention

- FIG. 11(a) presents a piecewise exponential utility curve

- FIG. 11(b) a sample hybrid utility function

- FIG. 12 is an exemplary logit historic-response curve

- FIG. 13 presents an illustrative qualitative demand curve as a function of days of the week

- FIGS. 14 and 15 are block schematic and target-directed implementation diagrams of a configuration for use in the improved SAEJ structures of the invention, illustrating optimal price computation in accordance with the invention

- FIGS. 16 and 18 are diagrams similar to FIG. 14 illustrating, respectively, a market share-directed SAEJ implementation and a utility derivative-following implementation, respectively;

- FIG. 17 is a schematic pricing cycle representation of persistent price during promotion and avoidance of such persistent price auction

- FIGS. 19 and 20 show suitable model optimizer configurations with exploration implementations, respectively configured and computational.

- FIGS. 21 through 23 are block diagrams of adaptation of the optimizing engine technique of the invention to illustrative banking credit card and loan industry offerings.

- the [ARTIST] type system may incorporate a “Buyer System” (BS) implementation ( FIG. 1 ) that may involve, for example, a buyer laptop computer, desktop, PDA or cell phone computers, in on-line connection over the conventional world-wide Internet (so labeled schematically) with a reverse auctioneer controller (RAC).

- BS Busyer System

- RAC reverse auctioneer controller

- illustrative custom hardware such as server farms, computer work-stations or mainframes may be implemented with the ‘Seller System’ seller automated engine implementations ‘SAEJ’, and are generally connected over the conventional world-wide Internet to the RAC.

- SAEJ seller automated engine implementations

- the key features of the sellers participation reside in fully automated bids in real-time, iteratively and automatically modified in accordance with the customer (buyer) specific profile and the current market conditions and also the sellers inputted specific business objectives and constraints as fully described in said co-pending application.

- Respective requests for quotes RFQ and for reverse auction (RFRA), for a price watch and/or for automatic notification, or for a price watch and automated purchase, and for bid result acceptance, are all associated with the Buyer System state machine operation, instructing transmission over the Internet to the RAC as in said co-pending application.

- the buyer input for a price watch as good quotes or reverse auction results are obtained may include such items as target price, time frame, notification, e-mail or device type format, telephone or SMS number, etc., all as detailed in said co-pending application.

- the RAC processing provides for matching sellers, generating initialized unique buyer profile packets, and where there are process responses from seller automated engines SAEJ, for further processing and updating the same.

- the architecture of the [ARTIST] invention of said co-pending application enables fully automated, instantaneous, accurate and competitive quotes from sellers on a twenty four hour, seven days a week basis in response to an on-demand ‘Request for Quote’ (RFQ) from a ‘Buyer System’ (BS). It also allows such systems to request at any time on a twenty four hour, seven days a week basis, a true instantaneous reverse auction (RFRA or a request for bid, RFB) amongst sellers, where fully automated seller engines SAEJ iteratively bid amongst themselves in real-time to provide the best bid—i.e. the lowest price for a product or service supplier, or the highest banking interest rate CD, for example.

- RFRA a true instantaneous reverse auction

- RFB request for bid

- Each seller engine automatically responds with instantaneous iterative bids specific to: the unique buyer profile, to prevailing and historic market trends, and to competitive dynamics, to the last round lowest bid, dollar and unit volume of the request, and to its own marketing/promotion strategy or business objectives.

- the bids are dynamically generated to stay within the seller's unique business model-driven constraints; these constraints themselves being further automatically modified within pre-defined hard limits on a product-by-product basis based on historic market data and trend lines.

- This seller automated engine SAEJ dramatically cuts down the prior-art need and associated substantial expense for manually tracking and comparing thousands of items across hundreds of competitors.

- the seller moreover, also has the option to decline participating in bids other than those of its interest, such as within its own class of sellers in order to preserve and protect its own business model.

- the buyers not only get instantaneous on-demand response to their requests, but, as before stated, also enormous benefit by this forced real-time iterative competition amongst sellers. Instead of getting a generic price, a buyer does better based on its own unique profile which includes purchasing history, dollar and unit/units volume of its shopping portfolio and its willingness to accept promotions and advertisements. The buyer can also request that only certain class/classes of sellers participate in this iterative competitive bidding for the buyers business based on its own comfort factor. The buyer also can set a price limit for its desired shopping portfolio, put it on price watch, and if and when matched, receiving notification or automatically effecting purchase, if so chosen. If the price drops even more within a certain time frame, furthermore, the buyer is automatically notified, as for credit.

- Such automated on-demand instantaneous buyer-centric reverse auction will allow the buyer to get the best possible price from multiple sellers, while enabling the same seller iteratively and automatically to compete in real-time for the buyer's business (‘price’ and ‘value’ are herein used interchangeably).

- Price and ‘value’ are herein used interchangeably.

- a buyer looking to buy a camera for example, the desire is to get the lowest price; on the other hand, a buyer wanting to deposit money at a bank for a year-long CD is looking to get the best rate of interest.

- the goal is to get best prices for the buyers and yet also to optimize the revenue/profit and other business objectives of the sellers by enabling them to evaluate the buyer demands in real-time, and with the corresponding ability automatically to respond to various situations instantaneously without any manual intervention, based on pre-defined variables and constraints.

- FIG. 1 illustrates a high level block diagram for the SAEJ implementation described in the present application.

- the SAEJ is shown consisting of the following functional units:

- the PMU implementations 4 described herein consist of two types of pricing functional units: Price Optimizers (PO) and Price Integrators (PI).

- the role of the price optimizer is to compute the optimal price based on input data such as a buyer request, real-time market data, historic data, etc, and seller configurations; i.e. the parameters programmed by the seller based on its or his unique objectives.

- the PMU 4 can compute the optimal price based on multiple diverse objectives.

- a group of price optimizers work together to generate optimal price through one or more price integrators, in real-time.

- the price integrator further enhances the optimizer outputs by integrating additional variables and constraints as provided by the seller. Examples of these variables and constraints may include (but are not limited to):

- FIG. 2 schematically illustrates such optimizers (PO) as seperate blocks, with each optimizer specific to certain goals or certain business objectives of the seller (shown generally in FIG. 2 and specifically under “INPUTS” in FIGS. 3-5 , as for the illustrative, optimizing of global prices 8 , events 9 , promotions 10 , supplier's break points 11 , and other optimizers 12 , etc.)

- the price optimizers PO receive the input requests and data at 1 1 , including the specific inputs of FIGS. 3-5 , shown as real-time market data 16 , historical data 19 , sellers targets 15 , etc.

- the optimizers output their individual optimized prices into the price integrator (PI) that processes the prices along with all the other inputs and sends a price quote at 7 .

- PI price integrator

- FIG. 2 The optimizers in FIG. 2 are schematically deliberately shown as free-standing blocks not connected to one another.

- FIGS. 3-6 illustrate specific examples of how they may be connected into the system and with flexible architectures so as to permit implementation of these optimizers in different ways, based on different objectives, as later discussed.

- a price optimizer The role of a price optimizer is thus to compute the optimal price based on input data and configuration data—parameters programmed into the SAEJ by the seller, based on the seller's unique business objectives.

- a group of price optimizers may work together to output optimal prices through one or more price integrators.

- the price integrator further enhances the optimizer outputs by integrating additional variables and business rules as provided by the seller. Examples of such variables and business rules are upper and lower bounds on price; regions of price and/or gross margins in which certain optimizers are given preference over the others; and further group discounts applied to the optimizer outputs.

- the PMU of the invention thus consists of a set of one or more price optimizer functional units (PO), illustrated at 8 - 12 in FIGS. 3-5 , that can be applied to various market inputs illustrated at 13 - 19 .

- the price optimizers may work independently or dependently to determine the optimal price for their specific target criteria.

- the output of the price optimizer is sent to a price integrator functional unit (PI) later described in more detail, that determines the best price at that instant; and a request is then sent back to the reverse auction controller.

- FIG. 2 illustrates such optimizers with their outputs sent to the price integrator (PI) before being sent back to the auction controller RAC through the SMU 3 .

- the PMU architecture of the invention is highly modular, allowing the price optimizers to be architected in several ways to accomplish the different goals.

- FIGS. 3 , 4 , 5 and 6 hereinafter more fully discussed in detail, illustrate a few different ways of architecting the PMU with various types of price optimizers and integrators.

- FIG. 3 illustrates a parallel processing architecture implementation in which each of the before-described optimizers 8 , 9 , 10 , 11 and 12 runs independently of the others, with all optimizers running concurrently.

- the output results of each optimizer are fed into the price integrator (PI) that processes the price computations received and computes a single optimal price for the request.

- the price integrator also ensures that the final price is consistent with the constraints specified by the seller.

- the resulting price quote 7 is sent back to the session management unit 3 of FIG. 1 and then in turn is sent to the RAC.

- the optimizers may be implemented in their own operating system threads, or processed for execution by one or more general purpose CPUs in parallel.

- special purpose processors such as a micro-programmable processor or a custom hardware processor may also be implemented for each optimizer, and they may then be run in parallel.

- FIG. 4 an example of a pipelined architecture for the price optimizers is presented.

- the result of each optimizer (PO) is serially fed ( 8 - 12 ) into the next optimizer and a request goes through the optimizers sequentially in pipeline fashion.

- each optimizer may have an integrator function built in that uses the previous result to compute the next result, all in real-time.

- the price quote result 7 of the final optimizer is sent back to the SMU 3 of FIG. 1 to be returned to RAC.

- request pipelining is used to ensure that each optimizer is always processing a request.

- queues may, indeed, be inserted between optimizers to buffer requests until the next optimizer in the pipeline is ready to process it.

- PMU may have more than one such pipeline configuration if so desired; for example, to improve the performance, or to process similar or dissimilar variables, resulting in further optimization across product lines.

- FIG. 5 Another variant of the architecture useful with the present invention is shown in FIG. 5 —a hub-and-spoke architecture for the optimizer.

- the price integrator (PI) 1 acts as a hub and the individual price optimizers 8 - 12 are the spokes that communicate with the hub.

- the integrator decides when to send the request to each optimizer and how to combine the results.

- the integrator may choose to send the requests in series, or in parallel, or a combination thereof, and process the results in real-time based on the seller's objectives.

- FIG. 6 illustrates a hybrid approach to the PMU architecture where again the price integrator (PI) 1 forms a central hub, with the spokes being further sub-configurations of the optimizers, including both independent and dependent variations.

- one spoke may be a parallel optimizer configuration, (Optimizers I ⁇ N at the right), while another may be a pipelined configuration (Optimizers N+L through M at the left), and yet others may be individual optimizers as at P, or any combination of the above. It is easy to see that this implementation covers any arbitrary way of architecting multiple price optimizers with a price integrator, all as determined by the objectives of the seller.

- the price optimizer architectures of the invention can enable several types of price optimization, including:

- optimizer is determined by the seller's objectives; whereas the implementation used by the optimizer, enables achievement of these objectives.

- Each optimizer such as the illustrative price optimizers 8 - 12 before described in connection with FIGS. 3-5 , regardless of type, can be configured to use any of the above pre-specified implementations, and can, indeed, change its preferred implementation dynamically, based on the seller configuration.

- TABLE 1 is an illustrative matrix of such price optimizers and the suitable respective implementations presented in this application.

- Sales target optimizers are best suited to use the target-driven implementation (A2), of TABLE 1, but could also use any implementation (A1, A3, A4, A5) based on a seller's objectives, as well as permitting switching between implementations dynamically, as per configuration.

- Market share optimizers generate the optimal price for achieving and maintaining a seller-specified market share.

- market share is often used as a growth indicator and the seller may have specific growth targets to be achieved over a specified time period.

- reducing or maintaining current market share could also be a goal. This may be relevant when the market price is falling and the seller must quickly decide to compromise on the sales targets and just maintain a market share compared to its competitors. It may also be pertinent in a rising market where the seller may be exceeding sales targets, yet may be falling behind on market share. In this case, the seller may want to use the market share as a tracker to stay abreast of the competition.

- Market share optimizers are best suited for the market share-directed implementation (B1) or the rules engine implementation (B5) of TABLE 1.

- Event optimizers of the third row of TABLE 1 generate the optimal price for both planned and unplanned events. These events can be considered as temporary promotions that are put in place to achieve certain specific objectives. Some examples of planned and unplanned events are:

- the event optimizers may also use any of the implementations (C1, C2, C3, C4, C5) as listed in TABLE 1, as well as switch between implementations dynamically.

- (D) Supply-break optimizers generate the optimal price for achieving the supply break.

- the seller may want to run a short-term promotion, aggressively to sell more units and achieve the supply break, assuming the short-term reduction in profitability is more than offset by the reduced cost gained from the supply break. This is in contrast to existing technologies where there is no way to react quickly to a supply-break opportunity.

- the supply-break event may be considered a special promotion event during which the seller is trying to achieve the supply break targets. In this case, the seller will typically provide the following information for a supplier's break:

- This optimizer can then make use of the target-directed implementation (D2) of TABLE 1.

- the target is to sell N more units prior to the expiration of the specified duration.

- the parameters of the implementation can be different from the global price optimizer. That optimizer may also use any other implementations, such as (D1, D3, D4, D5) of TABLE 1.

- Price watch list optimizers use the buyer's price watch lists (transmitted to the SAEJ by RAC) as a collective demand or an aggregated order. Based on the pre-specified constraints, a partial list of requests may be fulfilled.

- the advantage for the price watch lists is that it allows the seller to maintain and track buyer desire to purchase products at certain price points determined by the buyers. Such an optimizer may well use any of the implementations (E1, E2, E3, E4, E5) of TABLE 1.

- Other optimizers may also be created as desired by the seller.

- the architecture provides the ability to define new optimizers based on the seller unique objectives and the ability for the optimizers to use any suitable implementation (F1, F2, F3, F4, F5) of TABLE 1 and change implementation via seller configuration or otherwise, dynamically.

- the PMU architecture of the invention enables multiple price optimizers to function in a variety of parallel, pipelined, dependent and/or independent ways and/or any combination of these.

- Each optimizer may flexibly be of any type above, and may use any implementation, as described.

- the optimizers, in conjunction, will optimize for all the objectives as configured by the seller.

- the price integrator is effectively a super-optimizer, optimizing across the output of each feeder optimizer, coupled with additional other inputs, in a manner such as to produce a final optimized result across the board.

- the price integrator then makes price decisions by applying computation, logic and/or pricing rules (or any combination thereof) on outputs from the price optimizers and other external inputs (price request, targets, real-time sales data and price watch lists etc.).

- Computation-centric-only implementations may be quite different from pure rule-based implementations.

- a simple price integrator PI may use the best price from the parallel optimizers.

- the integrator may use any (or a combination) of the above optimizer implementations to further optimize the price computed by the optimizers.

- the price integrator acts as a hub responsible for sequentially, and/or in parallel, invoking groups of dependent and independent optimizers. The integrator processes the results of the optimizers as it invokes them, uses the results as additional inputs into the next set of dependent optimizers, and invokes them.

- the invocation is determined by complex logic, computation, rules engines, prevailing market conditions, or any combination of these.

- the set and sequence of optimizers invoked may change dynamically based on previous optimizer results as well as prevailing market conditions.

- the integrator is then ultimately responsible for producing a final price at 7 for the request.

- the price optimizers of the invention together with the price integrator, thus allow the seller to achieve his or its objectives simultaneously while dynamically changing the priority of each objective based on current market conditions, current fill status, and function of time, and a variety of other factors.

- the set of novel price optimizer implementations of the invention enables the seller to optimally achieve pre-set objectives optimally without accurate advance knowledge of demand, buyer characteristics and competitor behaviors. It is now in order to examine such implementation in greater detail.

- such implementations can be broadly categorized either as quantitative implementations or rules-based implementations.

- the rules-based approach while simple, does not scale as well as the quantitative solution.

- a rules-based solution typically requires the designer to consider all possible cases including complex inter-variable relationships, and then write rules for each one of them. As the requirements evolve, there is need to continually update them, correspondingly. This tends to get very complex and quickly non-scalable. It is difficult to maintain and upgrade, unlike a quantitative solution, which, though difficult to conceive, is highly scalable, solved, and is easy to maintain and upgrade.

- Such price optimizer implementations embrace both the before-mentioned rules-based implementations and the quantitative implementations, including those previously discussed; namely:

- a rules engine may be a software or hardware subsystem that manages complex rules and matches them against inputs and seller configuration. Rules engines typically use pattern-matching algorithms such as the “Rete” algorithm. In the implementation of the present invention, also, any rules engine may be used, but with a highly novel ability to apply rules to a real-time iterative reverse auction in a dynamic fashion, while using other optimizers in conjunction to determine optimal price—this being one of the novel aspects of the invention with rules engine implementation involving either or both of price optimizers and/or price integrators.

- a pricing rule consists of conditions and actions, with the action part of the rule producing the optimal price quote.

- Pricing rules are seller-created rules that may be used to make pricing decisions.

- a simple rule for a price integrator could be to compute the lowest (or highest or average etc) price from all the price optimizers, while further checking the limits of price as configured by the seller.

- An example of a rule used by a price optimizer may be a rule to specify certain discounts and/or promotional pricing such as zip-code-based promotion or a consumer index-based promotion or group-membership-based promotion or other such promotion.

- Rules could also be used to raise the price based upon the happening of certain criteria such as an increase in demand over a threshold.

- Rules may also be used as a trigger for price watch lists when sufficient buyer demand has accumulated at a certain pre-configured set of prices.

- Rules may thus be represented as decision tables or other formats as required by the specific rules engine—even presentable in a more intuitive fashion using a graphical user interface or a web-based interface to the seller.

- the price optimizer and price integrator could, indeed, become one functional element.

- FIG. 7 A typical implementation using such rules is illustrated in exemplary FIG. 7 .

- the rules engine optimizer is invoked at the start of every new auction, and the price resulting from the optimizer computation, can be used as a temporary computed optimized floor for the next bidding rounds in the same auction. This is an optimized sub-constraint clearly residing within the overall constraints configured by the seller. In this case, the PMU 4 starts with an initial price and iteratively drops the price to the temporary computed optimized floor, or until the auction ends (whichever comes first). For such RFQ, there are several options available such as:

- This implementation makes no assumptions. Its inputs are only the seller's rules and the request data, the market data and the seller's configuration data used by the rules.

- the rules engine indeed, is typically far easier to conceive than quantitative solutions and may be a preferred choice for simple problems. It enables a simple implementation for price optimizers and/or price integrators and may be used to cover boundary conditions.

- the rules moreover, can be directly or indirectly mapped to the seller's objectives and may be intuitive for certain sellers.

- FIGS. 14 and 15 ( FIGS. 14 and 15 )

- the sales target-directed implementation introduces the ability to pursue any quantitative targets specified by the seller.

- Some examples of such targets are periodic sales targets (such as quarterly revenue, profit, sales volume etc), or specific promotion-driven sales targets (such as sell $100 k worth of the product over a weekend), supplier break targets (sell 1000 units in the next 2 hours) etc.

- This implementation also provides the ability to the seller to specify the pace with which to approach the corresponding targets, subject to the seller's risk averseness, market perception and other factors as outlined previously.

- a seller may want to sell more aggressively, for example, when the current revenue is remote from the target revenue (or vice versa), or sell at the same pace regardless of how far away the revenue is from the target.

- the implementation also provides the ability for the seller to subdivide the target equally or unequally and in any proportion into sub-targets over smaller time intervals—divide a weekly target into daily, or even day/night targets based on day of the week, as desired. This enables the seller to track and measure progress in smaller intervals, as well as sets the appropriate pace based on known qualitative buying patterns.

- the target-directed implementation furthermore, also enables the seller dynamically to increase or decrease the relative priorities of each of the targets in real-time. Sometimes profit may be more important than revenue, while at other times sales volume may be the most important, and so on. This ability to shift the relative degree of emphasis among targets based on prevailing market conditions, or based on the respective distance yet to cover for each target, or the time left in a pre-specified time interval, results in an optimal approach to achieve the targets simultaneously.

- the target-directed implementation uses the notion of “utility”, later more fully discussed, to represent the measure of a seller's perceived value of winning an auction with respect to the targets.

- the total utility for N incoming requests may be represented as:

- the optimal price offered by the seller can be computed by maximizing the expected utility. It is indeed possible to find the optimal price policy (p 1 , p 2 , . . . , p N ) to maximize the expected utility if the request arrival process and competitive price characteristics are assumed to be accurately predictable in advance. Clearly, this unviable assumption of being able to accurately predict the future in real-time in a competitive and dynamic market renders previously known techniques at best marginally useful, and that, indeed, only for off-line batch processing.

- the above-mentioned seller's total “utility” is defined as a weighted combination of several utilities such as revenue, profit and sales volume utilities. Any number of target utilities can be used to compose the total utility, thus giving the seller the ability to set numerous types of additional targets with appropriate weights.

- weights are typically configured by the seller. Some sellers may want to assign equal weights to targets such as revenue, profit, sales volume etc. Others may value one more than others; yet others may change the weights over time and as market conditions evolve. For example, for a retailer with seasonal apparel, sales volume target may be much more important than revenue or profit at the end of the season. If a product is selling below expectations, the seller can increase the sales volume weight substantially over the weights of other targets. If not configured by the seller, equal values for the weights may be used.

- the configurable weights provide the ability for sellers to assign emphasis (or de-emphasis) to each of their targets.

- the utilities are functions of respective “distances” to targets, the “distance” being the quantitative measure of how far away the seller is from the specified target. For example, if the target revenue for Q1 is $10 m, and on February 1, the current revenue is $3 m, then the “distance” for the revenue is a function of ($3 m/$10 m).

- utility function provides the ability for the seller to specify the pace/aggressiveness with which to approach the target.

- the linear utility function is computed as the achieved revenue, profit and sales volume etc so far, normalized by respective targets in the specified time interval.

- the revenue utility is (at time “t”),

- the linear utility can also be represented as a function of the “distance” to the respective targets.

- the distance of revenue from the revenue target and a simple corresponding linear utility can be defined as

- the piecewise linear utility function allows the seller to change his or its utility gain at arbitrarily chosen discrete distances to the target. This enables further optimization for the more sophisticated seller.

- a sample piecewise linear utility curve is shown in FIG. 9(a) .

- “a” is a factor to measure aggressiveness after the target has been reached. If “a” is chosen to be ⁇ 1, it is less aggressive; and if a>1, it is more aggressive.

- the total utility is a weighted combination of several (two, in the above example) piecewise linear utilities.

- FIG. 9(b) illustrates a piecewise linear utility function with three pieces, each with a different slope.

- a sample exponential utility curve corresponding to the above equation is shown in FIG. 10(a) .

- This exponential utility has the several properties that may represent desired seller behavior. For example:

- the above-defined exponential utility function has the unique property that the smaller a, the more aggressive it is when pursuing the target before reaching the same target. When a gets bigger and bigger, it gets closer and closer to the linear utility function, and it becomes less and less aggressive below the target. It is this ability to go from highly exponential to linear that makes this approach very attractive.

- A, B and a are exponential utility function parameters

- d R , d M and d S are normalized distances to targets. They are defined as

- the optimal price is computed by maximizing the weighted utility function.

- the maximization of the weighted exponential utility function is equivalent to the minimization of the weighted exponential distance to targets.

- FIG. 10(b) Another embodiment of the exponential utility type function is illustrated in FIG. 10(b) .

- u ⁇ A+Be ad .

- This function has the unique property that it approaches the target less aggressively when the distance to the target is large, and gets more aggressive as the distance to the target decreases. Such properties may represent a desired seller behavior; for example:

- a piecewise exponential utility function may also be used as shown in FIG. 11 (a), which enables the seller to adjust aggressiveness as desired.

- the novel implementation of the invention allows any utility function or a combination of heterogeneous utility functions to be used (such as a piecewise exponential, a combination of piecewise linear or polynomial, and exponential, etc.) to represent each seller's unique objectives as the distance from the target varies.

- the selection of the utility functions can also be changed by the seller via configuration.

- the hybrid utility function provides a powerful ability to vary the aggressiveness of the optimizer based on the distance to the target.

- the hybrid function consists of multiple pieces of linear and exponential utility functions as desired by the seller. As the distance to the target varies, different function forms can be used based on the seller's objectives and risk averseness.

- a sample hybrid utility function is illustrated in FIG. 11 (b).

- the target-directed implementation of FIGS. 14 and 15 also provides the seller with the ability to be time and demand sensitive in pursuing the target.

- the seller In case of a retailer, at the start of a quarter, the seller is likely far away from the quarterly targets. This is expected and the seller need not be overly aggressive in pricing products.

- time progresses e.g., the end of the quarter nears, if the seller is still very far from the target, then it may be prudent to pursue the target more aggressively; i.e., the additional gain in winning the subsequent auction would be considered high.

- time dependent There are numerous other factors that are time dependent that affect the desired seller's utility.

- the seller may have explicit sub-goals for the holiday season; the seller may be aware of changing buying patterns over weekends vs weekdays; there may be an upcoming event such as a super-bowl or a snowstorm; an advertising campaign that may lead to increased/decrease demand and thus require specific targets; in a 24 ⁇ 7 environment, the demand may be different during day vs night, and even during various hours of the day.

- a qualitative demand curve configuration can provide the seller with the ability to capture the varying relative demand over time and further enhances the effectiveness of the utility function.

- the seller is asked optionally to configure a qualitative demand curve for the target period.

- the seller's configuration could be based on a graphical display input; such as the sample qualitative demand curve for a weekly target illustrated in FIG. 12 .

- the demand curve provides a mechanism to measure and track the intermediate progress of the seller, as opposed to traditional techniques based on demand forecasting.

- the demand gradually increases over the week and through day 6, while decreasing back down on day 7.

- the weekly target is then subdivided into daily targets based on the relative demand curve. This process may be further used to derive night/day or even hourly targets during which the demand is relatively uniform. Effectively, one can compute the area under the curve as a relative number and then appropriately map it to the quantitative sales targets for that specific duration.

- the target-directed implementation finds the optimal price by maximizing the utility gain with respect to the distance to the target for the current sub-period.

- the sales targets may be readjusted based on performance and seller configuration. If the seller does not achieve the weekly revenue targets for the first week of the month, for example, the remaining unmet target from the week may be rolled over in several ways, if so desired, such as to the next week, uniformly or non-uniformly distributed across the remaining week of the month, year etc. This is completely dependent on the seller configuration. If the seller chooses to distribute the unmet targets to the remaining sub-periods, the distance to the new (higher) target effectively increases thus making the optimizer more aggressive.

- the unmet targets from before may be left to fulfill in the last month, if desired, resulting in potentially aggressively moving towards the target.

- the ability to use the demand curve to sub-divide targets provides intermediate check points, effectively minimizing of the seller's risk. If, however, the seller does not want to do this, all the unmet targets can be pushed to the end.

- the seller may also change the utility functions based on time to map against the demand curve. For example, they may choose to pursue the sub-targets less aggressively early in the quarter, while becoming more aggressive later in the quarter.

- the target-directed approach can satisfy a wide variety of seller objectives.

- the parameters of the historic bid-response function can be computed statistically by fitting a curve to the available auction historical data, based on minimizing the squared errors or using maximum-likelihood estimates as later described. Further enhancement can be made by more heavily weighing more recent historical data during the estimation.

- the historic bid-response function parameters may be computed either at the SAEJ or at the RAC.

- RAC may provide a service to all the SAEJs by periodically transmitting the parameters of well-known and/or common historic bid-response functions.

- Individual SAEJs may use the given bid-response parameters or may use other bid-response curves by based on seller configuration and/or historical data gathered by the individual SAEJs.

- the historic bid-response function is used as a nominal proxy for the recent market behavior. It allows the implementation quickly to compute an optimal price close to the market price. In case the computed bid-response parameters are not available, or if the market price has deviated from the last computation of bid-response parameters, the distance to the target enables the implementation to converge to the true market price.

- the historic bid-response parameters are estimated by minimizing the squares of the error terms from the bid-response curve to the actual wins and losses of each auction opportunity within the historic window configured.

- the indicator variable W i is assigned the value of 1 if the auction is won, and W i is assigned the value of 0 if the auction is lost.

- Each auction i also has a weight W i which expresses the confidence in the accuracy or relevance of the point.

- the bid-response should be as close to W i as possible. This can be achieved by solving the unconstrained optimization problem

- This implementation for computing the bid-response parameter values involves choosing parameter values that closely mimic the pattern of wins and losses resembling the actual historic outcomes.

- the parameters therefore, can be chosen in such a way that they maximize the probability of realizing the actual outcome over all observations. This can be achieved by solving the equation

- the ideal bid-response function indeed, is the Logit function due to its unique characteristics.

- the general form of the Logit function is:

- ⁇ ⁇ ( p ) 1 1 + e a + bp + cQ + dp c , ( 15 ) where p Unit price quoted by the seller. ⁇ (p) Historic bid-response function at price p Q Order size (number of units) p c Recent historic average unit price in the market, and where a, b, c, d are scaling parameters for the Logit function. These parameters are used to measure the effects of various factors:

- FIGS. 14 and 15 A typical flowchart implementation for the illustrative sales target-directed implementation of FIGS. 14 and 15 follows:

- this implementation does not impose any restrictions on the price that is returned to the RAC.

- the price is returned via the integrator which may be configured in several ways such as, the following.

- the optimizer is invoked at the start of every new auction, and the price resulting from the optimizer computation, can be used as a temporary computed optimized floor (in case of the retail vertical) for the next bidding rounds in the same auction.

- This is an optimized sub-constraint clearly residing within the overall constraints configured by the seller.

- the integrator starts with a configured (or computed) ceiling price and iteratively drops the price to the temporary computed optimized floor or until the auction ends (whichever comes first).

- the options are simpler such as return the list price configured by the seller or return the optimal price at 45 as computed by the optimizer.

- the target directed implementation is well suited for the sales target optimizer where the seller is trying to achieve annual, quarterly, monthly etc, targets.

- the target intervals can also overlap with two optimizers operating over the desired time periods and with appropriate targets, respectively.

- the target-directed implementation can also be used for events price optimization.

- the seller may want to boost sales during a week/weekend or any arbitrary time interval.

- the seller configures the optimizer with the appropriate targets, duration, weights etc, and the optimizer computes an optimal price from the targets.

- the integrator decides which price (or a new price resulting from integrating the several optimal prices) to use.

- Another example of effective use of this implementation is for supply break optimizations.

- the seller can specify the supply break information, and these form the targets entered into the supplier break optimizer 11 .

- the supply break optimizer is triggered and processes requests until the supply break is met or the supply break time expires (whichever comes first).

- the price integrator PI uses the results of the individual optimizers, along with appropriate constraints on pricing, and other input from the seller, and then generates the bid price at 7 to be returned to the RAC.

- the target-directed implementation has several key advantages that enables its use for a variety of optimization purposes, with the ability to adapt to a wide range of evolving market conditions and seller objectives. Some of these advantages are.

- the market share-directed implementation of the invention previously described computes price by considering the percentage of the auctions won (market share) in the previous pre-defined number of requests. As an example, consider that 10 auctions were won out of 100 requests received. This could be computed as a unique number per so many requests received for example in a slot of 100 auctions, or could be a rolling number such as number of auctions won in last 100 auctions. If the market share is below the desired target, the price will be appropriately corrected automatically and in real-time until the desired objective is matched. If the number of auctions won is higher than the desired market share, the machine will automatically make appropriate corrections using this feedback loop to cut the winning percentage down, if so desired by the seller (or vice versa). The key idea is to make the winning independent of the time of the day, or day of the week, or if it was a snow day, etc, and ensure that the winning percentage number effectively adjusts itself as per the market demand without requiring any quantitative forecast.

- This market-share-directed implementation makes no assumptions about the demand, buyer and competitor characteristics.

- the key input is the target market share.

- the product cost and the appropriate constraints on the unit price are also required inputs.

- One additional feature provided by the RAC is the ability to provide a constraint in terms of not to exceed a configured market share, thus enabling liquidity.

- the RAC market share will override the seller-configured market share in case the latter exceeds the former.

- the RAC could constrain any one entity to no more than 25% market share.

- the utility derivative-following implementation is based on improving the seller's utility over time.

- the utility in the preferred embodiment, can be formulated as a function of distance to the target as previously described in the target-directed implementation. In alternative embodiments, any other utility function may be used as desired by the seller.

- the utility derivative-following implementation compares the utility gained (or lost) from change in price over two previous intervals. It then adjusts its price by looking at the amount of utility earned on the previous interval as a result of the previous interval price change. If the price change produced a higher utility, then the strategy makes a similar change in price for the next period. If the previous change produced lower utility, then the strategy makes an opposing price change for the next period. If the utility is target based, this approach will try to follow the market and pursue the targets simultaneously.

- FIG. 18 A typical implementation is shown below and illustrated in FIG. 18 .

- This implementation has some similar properties to the target-directed implementation before described. It uses the concept of maximizing utility to compute an optimal price for initial use. This is called the “baseline optimal price”. It further improves this baseline optimal price by using random (within constraints) deviations from the baseline optimal price to periodically explore the price space. Once a more optimal price is found, the implementation uses that as the baseline optimal price until an even more optimal price is found. This process continues as the system continues to hunt for the optimal price in an ever changing marketplace. The deviations from the baseline optimal could in fact be related to the distance to the target, or any other number as desired by the seller. The ability to explore the price space by using deviations from the baseline optimal price allows the seller to lead the market where a more optimal price is found.

- FIGS. 19 and 20 A typical implementation is described in the flowchart below and is illustrated in FIGS. 19 and 20 .

- FIGS. 19 and 20 make assumptions similar to the before-described target-directed implementation, as follows:

- This implementation being utility based and the utility being related to the targets, it is also thus target-directed, permitting the seller to have the ability to lead the market by setting the product price by using random deviations up or down from the baseline price.

- the implementation can be further enhanced, moreover, by using machine learning techniques that provide intelligent ways of picking when to experiment; how much to raise/lower the price, and for how long.

- the SAEJ of the invention can satisfy the various and ever-changing objectives of sellers in a wide range of verticals

- the SAEJ architecture provides the additional ability to the seller of enabling quantitative optimization of prices based on more complex dependent and independent objectives, in turn involving one or more verticals.

- prior art or existing non-SAEJ based technology relying on manual or off-line processing, it is not possible to optimize in real-time and iteratively, thus limiting the scope of applications to silos of a small set of individual products, or verticals using manual or batch processing.

- Banks rely on consumer deposits (in the form of CDs, High Yield Savings, Checking etc) as a source of funds for their loan commitments. They offer CD products with various maturities—as 3 months, 6 months, 9 months, 1 year, etc. In the case of CDs, they generate profit from the difference (spread) between interest payments on CDs (calculated as the annual percentage yield or APY) and the interest earned on loans.

- CDs High Yield Savings, Checking etc

- the before-described target-directed implementation may be used; but in alternate embodiments, the market-share implementation, the rules-based implementation, the utility derivative-following implementation, the model optimizer with exploration implementation, or a combination of these implementations may also be used.

- a bank could have a need to raise $10M in deposits in the next 24 hours, under terms of a one year duration, a lending rate of 8.5% with a minimum spread of 3%.

- Other such targets also called “buckets” might be a desire to raise $3M in the next 3 days, with a 6 month duration, for a lending rate of 8% and with a minimum spread of 2.75%. Both these and other such requests can be set-up simultaneously.

- Each of these targets furthermore, can also be prioritized or a relative weight assigned thereto, if so desired, enabling each new request to be responded to with corresponding aggressiveness subject to the current status of the target.

- the PMU 4 consists of a front-end optimizer PO at 80 , as well as several SAEJ credit-optimizers (SAEJ 1 through SAEJ 5 ), one for each target specified by the seller.

- SAEJ 1 through SAEJ 5 SAEJ credit-optimizers

- the front-end optimizer 80 examines its credit score in real-time to ensure that it is within the acceptable range (above 400 in this case). Assuming the request is within the range, the optimizer uses the following computation to determine the incremental blended average, if this auction is to be won.

- the blended credit score is calculated as

- C is the blended credit score

- Ci is the average credit score for target i

- Fi is the amount of credit issued so far for target i

- N is the total number of targets.

- the front-end optimizer If the computed blended credit score is expected to remain within the constraints outlined by the bank, the front-end optimizer signals the corresponding credit-optimizer to participate in the bid process. Alternatively, if the blended average constraints are going to be violated, the front-end optimizer will not signal any credit-optimizer to participate in the bid process.

- this optimization across various targets, in real-time and on a dynamic basis guarantees the bank all the time a consistent blended credit score (CS) quality of its entire credit card portfolio at any time.

- the bank furthermore, also has provided for the blended interest rate per line of credit target and across the portfolio—all available at the same time. This is illustrated in FIG. 22 where again as in FIG. 21 , multiple SAEJ optimizers ( 1 through 5 ) are employed to achieve the blended credit score (CS).

- each SAEJ engine may also optimize its blended interest rate to the bank-specified level, using any of the techniques discussed herein.

- the bank will have the guarantee of a portfolio optimized for not only specific blended credit scores; but also further optimized to a desired interest rate level for each total credit-line target.

- a blended credit-score target can be achieved across these auto loan optimizer-engines 1 11 , 2 11 and 3 11 , and the same for blended interest rates.

- a price integrator PI of the invention may readily be used, as in FIG. 23 .

- the integrator connects the above-described deposit engines 1 1 through 4 1 to the front-end optimizer, so-labeled.

- the over all system may have the following illustrative constraints, with the loans being made only from the deposits collected.

- the aggregate percentage contribution from each deposit engine towards loans may be different—auto loans, for example, tend to be for longer terms.

- the bank could, as an example, specify that deposits are to be disbursed such that 94% of the deposits collected by the 2-year plus engine 4 1 , are to be used towards such auto loans; 50% for the 1-year deposits 3 1 ; 10%, for the 6-months 2 1 ; and 5% for 3 months 1 1 , and so on.

- Deposits may be collected by bidding in real-time for prospective depositors according to configured constraints. These deposits may then be funneled, appropriately proportioned, via the integrator to the front-end optimizer of the loan engines.

- the front-end optimizer examines its credit score in real-time to ensure that it is within the acceptable range. Assuming the request is within such range, the optimizer uses the following equation to determine the incremental blended credit score average across the portfolio, if this auction is won. The blended credit score is calculated as

- Ci the blended credit score for engine i

- Fi the amount of loan issued so far for engine i

- N the total number of loan engines.

- the front-end optimizer signals the matching loan engine to participate in the auction, assuming funds are available. Alternatively, if the blended credit score constraint is going to be violated, this optimizer will not signal any loan engine to participate in the bid process.

- the selected loan engine then participates in the auction with its unique constraints and targets as configured by the bank. Thus, not only are each engine targets optimized, but blended targets across various engines are also optimized and in real-time and on a dynamic basis. This guarantees the bank a consistent blended credit score quality across its entire auto loan portfolio at any time, all the time. Furthermore, the resulting blended interest rate across such loan engines can also be computed, providing additional insight into the loan quality. Additionally, the front end optimizer also optimizes for the blended portfolio interest rate by computing in real-time the allowable lower limit interest rate constraint as each loan auction request arrives. This dynamically computed allowable constraint is then automatically provided to the selected engine.

- this implementation provides a powerful mechanism for banks to collect deposits in real-time and subsequently to make auto loans in real-time while maintaining the appropriate constraints on both deposits and on loans, such that not only is the deposit base substantially expanded, but the corresponding loan business is appropriately matched—all the while maintaining an optimized loan quality both at in individual engine level and also across the entire loan portfolio.

- This architectural configuration using implementations described earlier can provide banks with an unprecedented opportunity to grow in a very short time.

- many variations of this concept adjusted for vertical specific parameters, can be used in various verticals.

Landscapes

- Business, Economics & Management (AREA)

- Accounting & Taxation (AREA)

- Finance (AREA)

- Engineering & Computer Science (AREA)

- Development Economics (AREA)

- Strategic Management (AREA)

- Theoretical Computer Science (AREA)

- Marketing (AREA)

- Physics & Mathematics (AREA)

- General Business, Economics & Management (AREA)

- General Physics & Mathematics (AREA)

- Economics (AREA)

- Entrepreneurship & Innovation (AREA)

- Technology Law (AREA)

- Game Theory and Decision Science (AREA)

- Data Mining & Analysis (AREA)

- Management, Administration, Business Operations System, And Electronic Commerce (AREA)

Abstract

An improved seller automated engine architecture methodology particularly (though not exclusively) for use in automated real-time iterative reverse auctions over the Internet and the like for the purchase and sale of goods and services, providing a choice of architectural implementations while enabling price optimization on market share-directed considerations, specific sales target-directed implementations, seller utility derivative-following implementations, model optimizer implementations and explorations, mathematical optimization-oriented and rules-based implementations.

Description

This reissue application has been filed for the reissue of U.S. patent application Ser. No. 11/880,980 now U.S. Pat. No. 7,895,116 titled “SELLER AUTOMATED ENGINE ARCHITECTURE AND METHODOLOGY FOR OPTIMIZED PRICING STRATEGIES IN AUTOMATED REAL-TIME ITERATIVE REVERSE AUCTIONS OVER THE INTERNET AND THE LIKE FOR THE PURCHASE AND SALE OF GOODS AND SERVICES” naming Mukesh Chatter, Rohit Goyal, and Shiao-bin Soong as inventors.